Embraer S.A. EMBJ is an aerospace company that designs and manufactures aircraft for commercial, executive and defense markets. With rising air travel demand and a strong order pipeline, the company is well-positioned for long-term growth.

However, this Zacks Rank #3 (Hold) stock faces risks related to supply-chain disruptions and labor shortages that may weigh on its near-term performance.

EMBJ’s Tailwinds

Embraer is benefiting from the steady recovery in global air travel. According to the International Air Transport Association, air traffic is expected to grow 4.9% in 2026, supporting demand for new aircraft. This trend is driving orders for Embraer’s E-Jets, particularly the E2 series, and strengthening its backlog, which improves revenue visibility.

The company’s executive aviation business is also performing well, supported by higher jet deliveries and rising demand for private travel. At the same time, Embraer is expanding its global Maintenance, Repair and Overhaul (MRO) network, which should support steady service revenues in the long run.

Moreover, its defense segment is gaining from increasing global military spending and new international partnerships, which are expected to drive future growth.

EMBJ’s Headwinds

Labor shortages remain a key challenge for Embraer S.A. and the broader aerospace industry. A significant portion of the workforce is nearing retirement, while younger employees are increasingly moving to other industries. This talent gap may reduce production efficiency, slow operations and lead to delays in aircraft deliveries.

Ongoing supply-chain issues continue to affect aircraft production, particularly for E2 jets. Shortages of critical components and delays from suppliers are disrupting manufacturing schedules. If these challenges persist, they could limit delivery volumes and weigh on near-term operating performance.

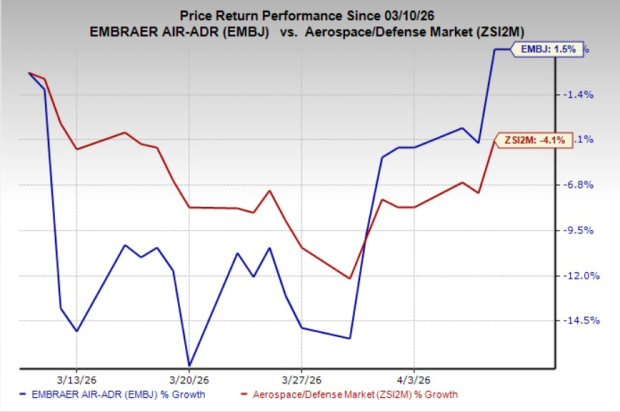

EMBJ Stock’s Price Performance

Shares of EMBJ have gained 1.5% in the past month against the industry’s 4.1% decline.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks from the same industry are Lockheed Martin LMT, StandardAero, Inc. SARO and Virgin Galactic SPCE. Each of these stocks currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

LMT delivered an average earnings surprise of 14.01% in the last four quarters. The Zacks Consensus Estimate for LMT’s 2026 earnings is pinned at $29.93 per share, which indicates year-over-year growth of 29.5%.

SARO delivered an average earnings surprise of 0.75% in the last four quarters. The consensus estimate for SARO’s 2026 earnings is pegged at $1.41 per share, which implies year-over-year growth of 18.5%.

SPCE delivered an average earnings surprise of 16.95% in the last four quarters. The consensus estimate for SPCE’s 2026 loss stands at $3.60 per share, which suggests year-over-year growth.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lockheed Martin Corporation (LMT): Free Stock Analysis Report

Virgin Galactic Holdings, Inc. (SPCE): Free Stock Analysis Report

StandardAero, Inc. (SARO): Free Stock Analysis Report

Embraer-Empresa Brasileira de Aeronautica (EMBJ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).