Advanced Micro Devices (AMD) has been one of the stronger names in chips lately. AMD stock has climbed about 40% since March 31, helped by fresh optimism around artificial intelligence (AI), server demand, and improving sentiment across the semiconductor sector.

AMD’s long-term story still looks interesting. The company has been making progress in data-center CPUs, AI accelerators, and client chips, while its latest results showed solid revenue growth and stronger cash flow. That gives the stock real support beyond just momentum.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For investors looking at the next leg of the AI trade, AMD may still have more room to run, but the rally also means the stock deserves a closer look before chasing it higher.

The AI Story Is Getting Attention

Advanced Micro Devices remains one of the most important names in chips. It makes processors for data centers, PCs, and gaming. AMD is also growing rapidly in the AI space. For years, AMD has tried to catch Nvidia (NVDA). Now, investors are starting to notice progress.

The company's data-center business is driving much of the optimism. EPYC server chips are gaining ground while Instinct AI accelerators grow in importance. Ryzen chips also keep AMD strong in PCs.

AMD’s moat is its full system approach. Data centers use complete setups, not single chips. Once installed, switching is hard.

The market rewards AI positioning. Nvidia still leads. But AMD is now seen as a strong second choice as companies diversify suppliers.

Why Is AMD Stock Rising?

AMD stock has gained more than 214% over the past year and nearly 30% year-to-date (YTD). The recent surge is not just about AMD’s own numbers. It is also about the broader chip tape. Several events in late March and early April gave semiconductor stocks a lift, including upbeat AI sentiment, improving geopolitical tone, and strong results from Taiwan Semiconductor (TSM), which reinforced confidence in global chip demand.

There were also reports that AMD may raise CPU prices, which added to the idea that pricing power is improving across the industry. More importantly, bullish commentary from analysts has helped change the tone around AMD stock.

Earlier in the year, AMD did lag some peers, but recent upgrades and positive notes have made investors more confident that the company is not losing relevance in AI.

www.barchart.com

www.barchart.com Q4 Earnings Show Strength

AMD’s fourth-quarter fiscal 2025 results were strong across the board. Revenue reached a record $10.27 billion, up 34% year-over-year (YOY), while GAAP EPS came in at $0.92, up 217% from the prior-year period, showing growth and better operating leverage.

The data-center business was the standout. Data-center revenue rose about 39% YOY to roughly $5.4 billion, driven by EPYC server chips and Instinct GPU demand. The quarter was not just about one segment carrying the load — it showed a broader recovery in demand.

Cash generation was also impressive. Operating cash flow came in around $2.3 billion, while free cash flow reached roughly $2.08 billion, both of which were much stronger than a year earlier. Gross margin improved as well, with gross margin hitting 57%, aided in part by product mix and a one-time inventory release tied to MI308 GPUs.

Management described the results as evidence of “broad-based demand,” and the numbers largely back that up. AMD is not just growing because of one product cycle. It is benefiting from a combination of server strength, PC resilience, and rising AI interest.

For Q1 2026, AMD guided revenue to about $9.8 billion, plus or minus $300 million. That would represent growth of roughly 32% YOY, a solid number even if it implies a normal seasonal pullback from the fourth quarter.

Valuation Is the Biggest Debate

The challenge is valuation. AMD now trades at roughly 44 times forward earnings, which is rich even in a market willing to pay up for AI exposure. That multiple is above Nvidia’s forward price-to-earnings (P/E) ratio, which is closer to 25 times, and far above Qualcomm’s (QCOM) multiple of 16 times. It is also well above AMD’s own historical norms. On a trailing basis, AMD stock looks even more expensive because of uneven profitability over the past year.

Supporters argue that the premium is fair because AMD’s earnings are still expected to compound rapidly. Analysts see revenue growth remaining strong in 2026, and if margins keep improving, the stock could still have room to run.

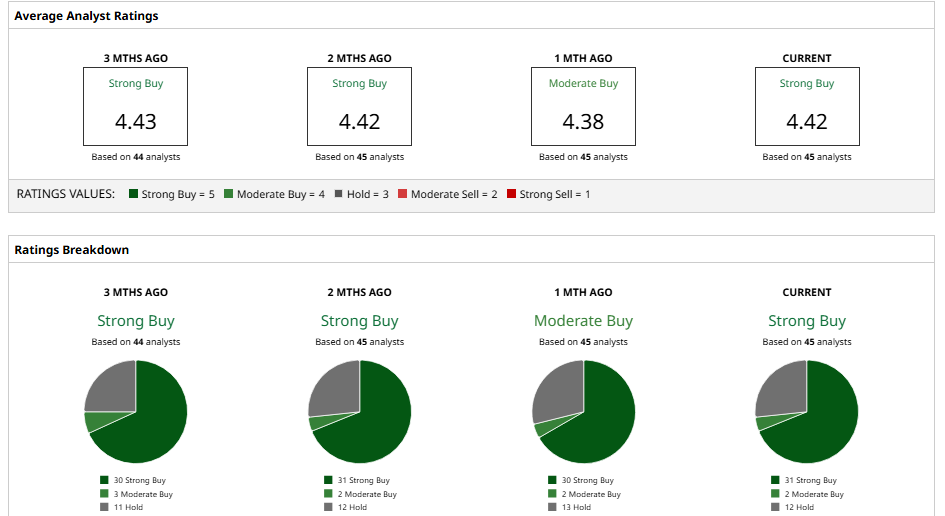

What Does Wall Street Think of AMD Stock?

Analysts remain broadly positive on AMD stock. The consensus view is a “Strong Buy" rating, with most firms expecting more upside over the next 12 months. The average price target of $287.39 implies potential upside of about 4% from current levels, while the high target of $380 implies a possible gain of 38%.

Several firms have reiterated bullish views on the stock recently, citing AMD’s growing role in AI infrastructure, its improving data-center mix, and the strength of its core CPU business. The wide spread in targets, though, shows that conviction is not uniform. Some analysts clearly believe AMD stock deserves a higher multiple, while others think the market has already priced in a lot of good news.

www.barchart.com

www.barchart.com The Bottom Line

I believe AMD stock’s rally is built on real progress, not just speculation. The company delivered record revenue, strong earnings growth, and solid cash flow, while its AI and server businesses continue to gain traction. That makes the long-term story more compelling than it was a year ago.

For now, AMD looks like a high-quality growth story with strong momentum, but also a stock that leaves little room for error.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Down 55% From Its YTD High, Is Super Micro Computer Stock a Buy, Sell, or Hold? Up 40% in the Past 12 Days, Should You Chase the Rally in AMD Stock? Is Allbirds Stock a Buy, Sell, or Hold Amid Major Pivot to NewBird AI? Unusual Options Activity Hints That a Big Fish Is Rolling Covered Calls on Shopify Stock