Leadership transitions are not just personnel changes and can reset investor expectations, reshape strategy, and, in some cases, redefine a company’s long-term trajectory. That’s exactly the moment Best Buy Co. (BBY) now finds itself in.

The company announced on April 22 that CEO Corie Barry will step down at the end of October, closing a tenure that began in 2019 and spanned both the pandemic-era boom and the more recent slowdown in consumer demand and supply‑chain pressures. Her successor, longtime executive Jason Bonfig, will take the reins at a time when the business is grappling with declining sales, intensifying competition, and a stock that has struggled to keep pace with broader markets.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The timing is critical. Best Buy’s fundamentals have softened in recent quarters, with pressured comparable sales and cautious forward guidance reflecting a tougher demand environment. Meanwhile, the stock has significantly underperformed since its pandemic peak, and it remains to be seen whether this leadership change can be a catalyst for a turnaround.

Best Buy has been working to reignite growth by expanding online sales, services, and its advertising business amid rising competition and Jason Bonfig has been leading these efforts, including overseeing the Canadian division, launching the U.S. online marketplace and expansion of its advertising business.

About Best Buy Stock

Best Buy is a leading consumer electronics retailer specializing in devices, appliances, and related services, operating more than 1,000 stores across the U.S. and Canada. Headquartered in Richfield, Minnesota, the company has been expanding beyond traditional retail into e-commerce, services, and advertising through initiatives such as its online marketplace and retail media platform. Best Buy has a market cap of $13.3 billion.

Best Buy’s stock performance has been notably weak relative to the broader market, reflecting both cyclical headwinds and company-specific challenges. Over the past year, the stock has delivered only marginal returns, while significantly lagging the S&P 500 Index ($SPX), which has gained 31.74% over the same period.

This year, momentum has turned negative. The stock is down 8.52% year-to-date (YTD), pressured by soft consumer demand, declining comparable sales, and a challenging macro backdrop marked by inflation and higher borrowing costs. Investor sentiment has also been impacted by structural concerns, including rising competition and supply constraints in key electronics categories.

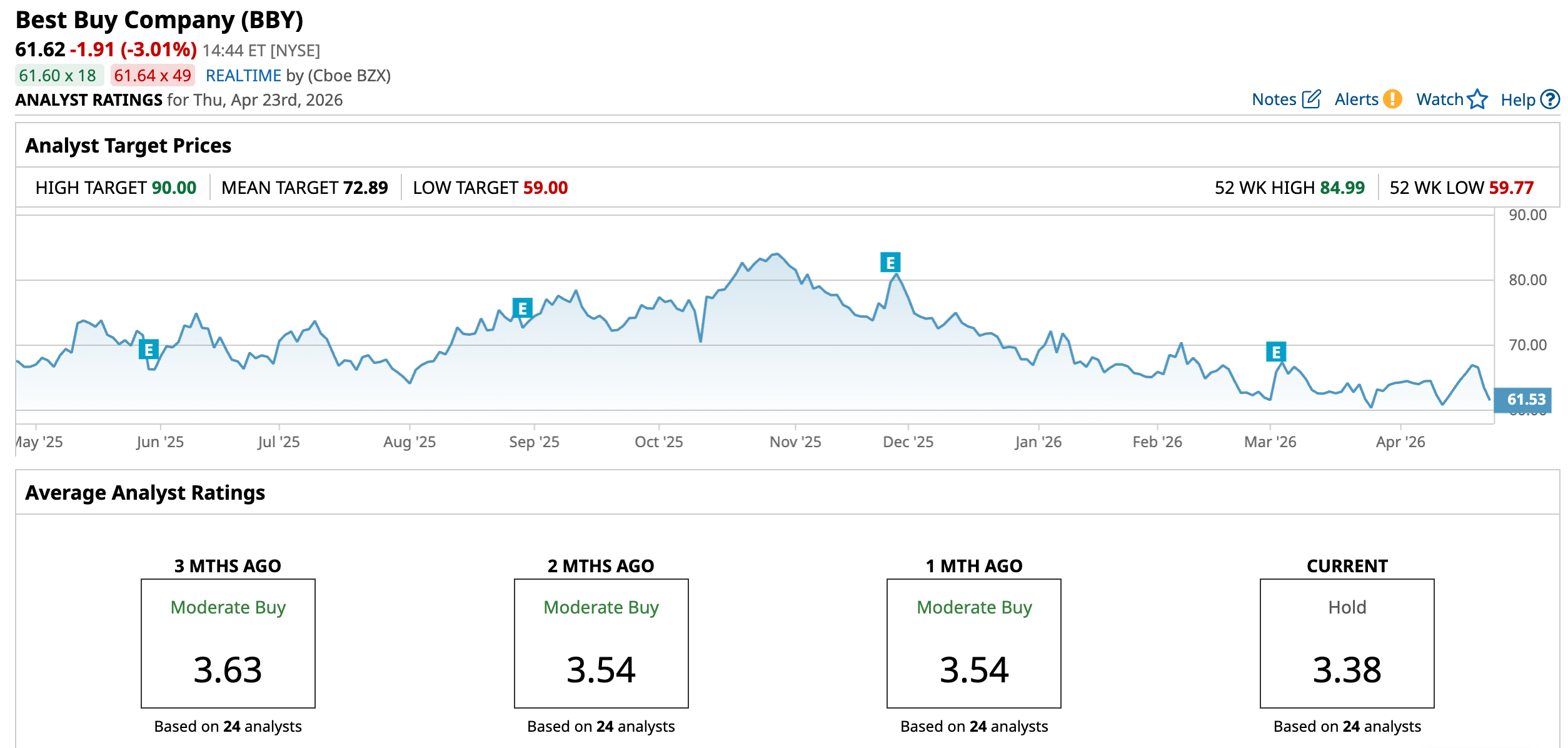

The latest bump came on April 22, when shares fell 4.6% intraday as investors reacted to the announcement of CEO Corie Barry’s departure and the appointment of Jason Bonfig as successor. The decline highlights investors skepticism around near-term growth visibility.

www.barchart.com

www.barchart.com The stock is currently trading at a discount compared to industry peers and its own historical average at 10.24 times forward earnings.

Mixed Financial Performance

Best Buy reported its fourth-quarter and full-year fiscal 2026 results on March 3, with the numbers reflecting top line pressure. In the fourth quarter, revenue came in at $13.8 billion, down about 1% year-over-year (YOY), while enterprise comparable sales declined 0.8% compared to a 0.5% increase in the prior-year period, underscoring continued softness in demand for consumer electronics.

Despite this, adjusted EPS rose slightly to $2.61 from $2.58 a year earlier, and operating margins improved to 5% from 4.9%.

For the full year, Best Buy generated revenue of $41.7 billion, broadly flat compared with $41.5 billion in fiscal 2025, while adjusted EPS increased slightly to $6.43 from $6.37. Importantly, the company returned to positive comparable sales growth of 0.5% for the year, a notable improvement from a 2.3% decline in the prior year, signaling early signs of stabilization after a prolonged period of contraction. Operating margin also improved to 4.3% from 4.2%.

Furthermore, the company issued cautious guidance for fiscal 2027, projecting revenue in the range of $41.2 billion to $42.1 billion, comparable sales change between -1% and +1%, and adjusted EPS of $6.30 to $6.60.

Analysts predict EPS to be $6.50 for fiscal 2027, up 1.1% YOY, and 7.9% annually to $7.01 in fiscal 2028.

What Do Analysts Expect for Best Buy Stock?

Earlier this month, Goldman Sachs downgraded Best Buy to “Sell” with a $59 price target. The firm flagged margin pressure from consumers trading down and weaker volumes, along with continued struggles in key categories like appliances and electronics.

Also, last month, Piper Sandler maintained a “Neutral” rating on Best Buy with a $68 price target.

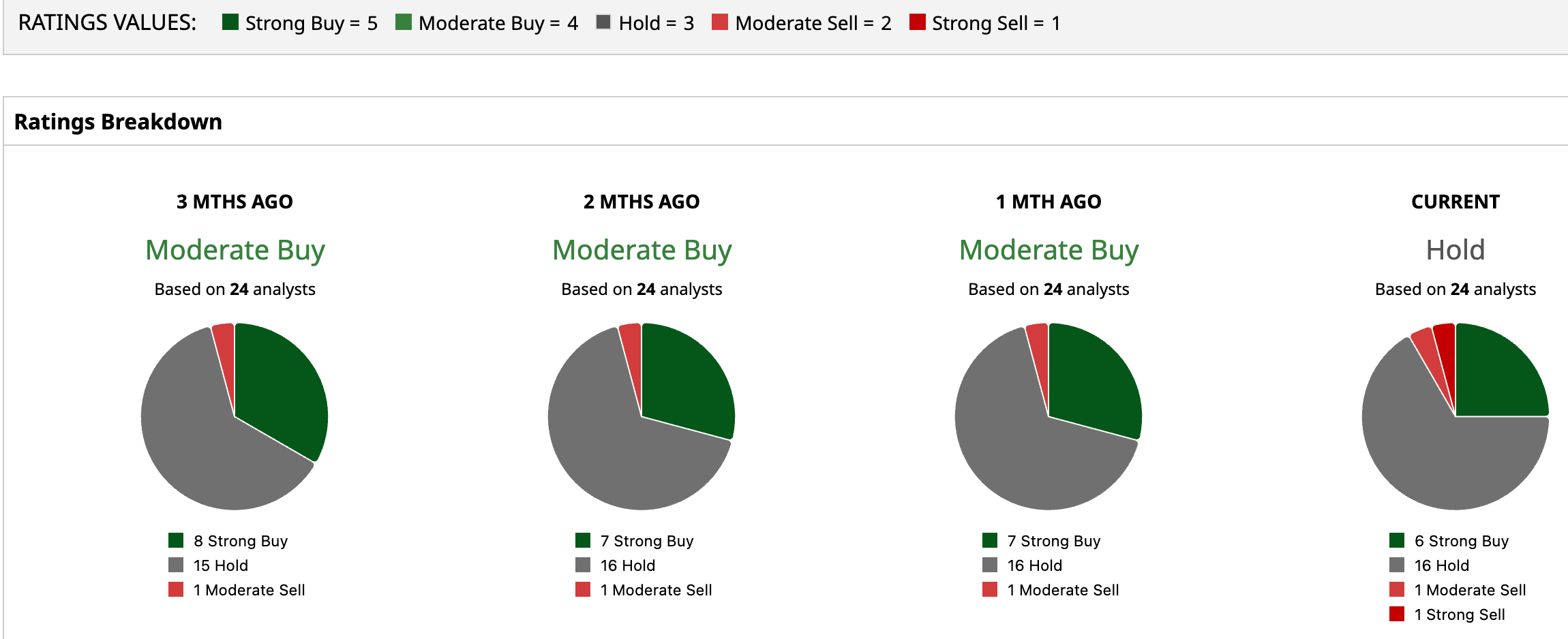

Wall Street is cautious about Best Buy. Overall, BBY has a consensus “Hold” rating. Of the 24 analysts covering the stock, six advise a “Strong Buy,” 16 analysts recommend it a “Hold” rating, one suggests a “Moderate Sell,” and one proposes a “Strong Sell.”

The average analyst price target for BBY is $72.89, indicating a potential upside of 18.3%. The Street-high target price of $90 suggests that the stock could rally as much as 46.1%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Tesla Beats in Q1—But TSLA Stock’s Bull Case Still Needs Fuel KeyBanc Sees AI Saving the Day for CrowdStrike Stock Despite Broad Wall Street Panic. Who’s Right? Amazon Aims to Take Over the GLP-1 Market Next. Will That Move the Needle for AMZN Stock? Should You Buy the Dip in ServiceNow Stock Today?