Even as the wider markets flirt with record-high levels, an earnings miss will almost inevitably lead to a brutal whiplash for any stock. That is undoubtedly what happened with the shares of the discount broker, Robinhood (HOOD). Investors, not able to find comfort, or rather opting to ignore any semblance of positivity, dumped HOOD stock unceremoniously, leading to its shares nosediving by more than 13% in yesterday's trading session.

About Robinhood

Founded in 2013, Robinhood brought about a revolution in the world of stockbroking by eliminating commissions and making investing accessible via mobile. In subsequent years, it expanded into crypto, margin lending, and retirement account management. Among them, crypto trading has become a vital source of revenue for the company.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.

Currently valued at a market cap of $73.9 billion, HOOD stock is down 35% on a year-to-date (YTD) basis.

So, after its latest quarterly results failed to live up to the Street's expectations, should HOOD be added to investors' hoods? Let's find out.

www.barchart.com

www.barchart.com Robinhood's Q1 Reality

A 47% year-over-year (YoY) drop in crypto revenues, a slight earnings miss, and a moderate sequential drop in the average revenue per user (ARPU) were the main triggers for the selloff yesterday. Yet, look under the “hood,” and one will find a stark mismatch between the results and the share price action.

Total net revenues increased 15% from the previous year to $1.07 billion. Within this, all the key revenue segments witnessed growth from the prior year. While the largest segment of transaction-based revenue grew by 7% YoY to $623 million, net interest revenue and other revenue climbed by 24% and 57% to $359 million and $85 million, respectively.

Granted, the growth rates for the EPS at 3% in the same period were not noteworthy, but it was growth nonetheless. Coming in at $0.38 per share, it missed the consensus estimate of $0.39 per share by a whisker. Moreover, this was just the second instance of an earnings miss from the company in the past nine quarters.

Further, all the key operating metrics displayed growth, albeit with varying degrees. While total platform assets and average revenue per user went up by impressive rates of 39% and 36% to $307 billion and $157, the assets under custody almost doubled in the same period to a record $27.4 billion.

Moreover, the quarter also saw a shot in the arm for Robinhood's international aspirations after it received approval from the Monetary Authority of Singapore to offer its brokerage services in the affluent Asian nation.

Meanwhile, net cash from operations jumped to $2 billion from $642 million in the year-ago period, as Robinhood ended the first quarter with a cash balance of about $5 billion. The company had no short-term debt on its books.

However, HOOD stock trades at punchy valuations. Its forward P/E, P/S, and P/CF of 33.74, 14.26, and 63.13 are all much above the sector medians of 10.64, 2.94, and 11.53, respectively.

Several Growth Drivers

Beyond its financials, which have established that it is in no danger, Robinhood's multiple revenue streams and a robust ecosystem keep it in good standing for the future.

Notably, a defining feature of Robinhood's recent evolution is how several high-margin revenue streams have converged into what now resembles a unified financial superapp. The business is no longer tethered to the ups and downs of transaction volume in the way it once was. In its place, the company has assembled a broader set of offerings that includes margin lending, a subscription tier under the Gold brand, retirement accounts, managed portfolios, and prediction market infrastructure. Each of these additions has deepened the relationship Robinhood holds with its users while lifting the revenue it extracts from each one over time. The numbers bear this out, with the margin book expanding 113% on a YoY basis and Gold subscribers growing 58% over the same period, a monetization shift that is now flowing visibly through to the bottom line.

However, perhaps the most underestimated dimension of the Robinhood story at this stage is what the company is building within prediction markets. Rather than simply offering event contracts to its users, Robinhood is constructing the underlying exchange and clearing infrastructure through its acquisition of MIAXdx and the development of its Rothera platform. The significance of this shift should not be understated. It moves the company from the position of a participant within the ecosystem to something closer to the operator. The addressable market expands as a result, and the revenue model that emerges carries the kind of network effects that tend to become more durable over time.

Then there is the Robinhood Ventures Fund I (RVI). RVI adds yet another dimension to the company's ambitions. Positioned around access to private companies operating at the frontier of their respective industries, the fund holds stakes in notable names including Databricks, the cloud-based data and AI platform; fintech operator Revolut; and Mercor, an AI-driven hiring marketplace.

What sets this vehicle apart from conventional private equity is both how it charges and who it admits. The management fee runs at about 2%, dropping to 1% during the first six months, and the fund carries no performance fee and imposes no accreditation requirements on participants. That stands in direct opposition to the traditional private equity model, where high entry thresholds and carried interest structures routinely diminish net returns for investors. Equally important is the distribution advantage Robinhood brings to the table. With more than 24 million funded accounts already on the platform, the company possesses a reach that no legacy venture capital firm can realistically replicate.

Further, the product roadmap has undergone an equally significant transformation. Robinhood Strategies arrived as a wealth management offering built around professionally managed portfolios, available at zero management fees for Gold members committing above $100,000. Robinhood Banking followed, targeting everyday checking and savings needs with a feature set that has historically been the preserve of high-net-worth clients at traditional institutions.

Sitting across all of this is an AI layer that the company is leaning into with increasing conviction. Robinhood Cortex, its AI investment tool, delivers real-time market analysis through features such as Stock Digests and Trade Builder, giving users a clearer picture of what is moving markets without the platform making decisions on their behalf.

The adoption figures attached to these initiatives confirm that the strategy is gaining real traction. Robinhood Strategies crossed $1.5 billion in assets under management, while Robinhood Banking surpassed $1.5 billion in deposits. Gold subscribers reached a record 4.2 million by the close of 2025. Taken together, these products are steadily pulling the company away from its historical dependence on transaction fees and toward a revenue base that is both more recurring in nature and considerably stickier over time.

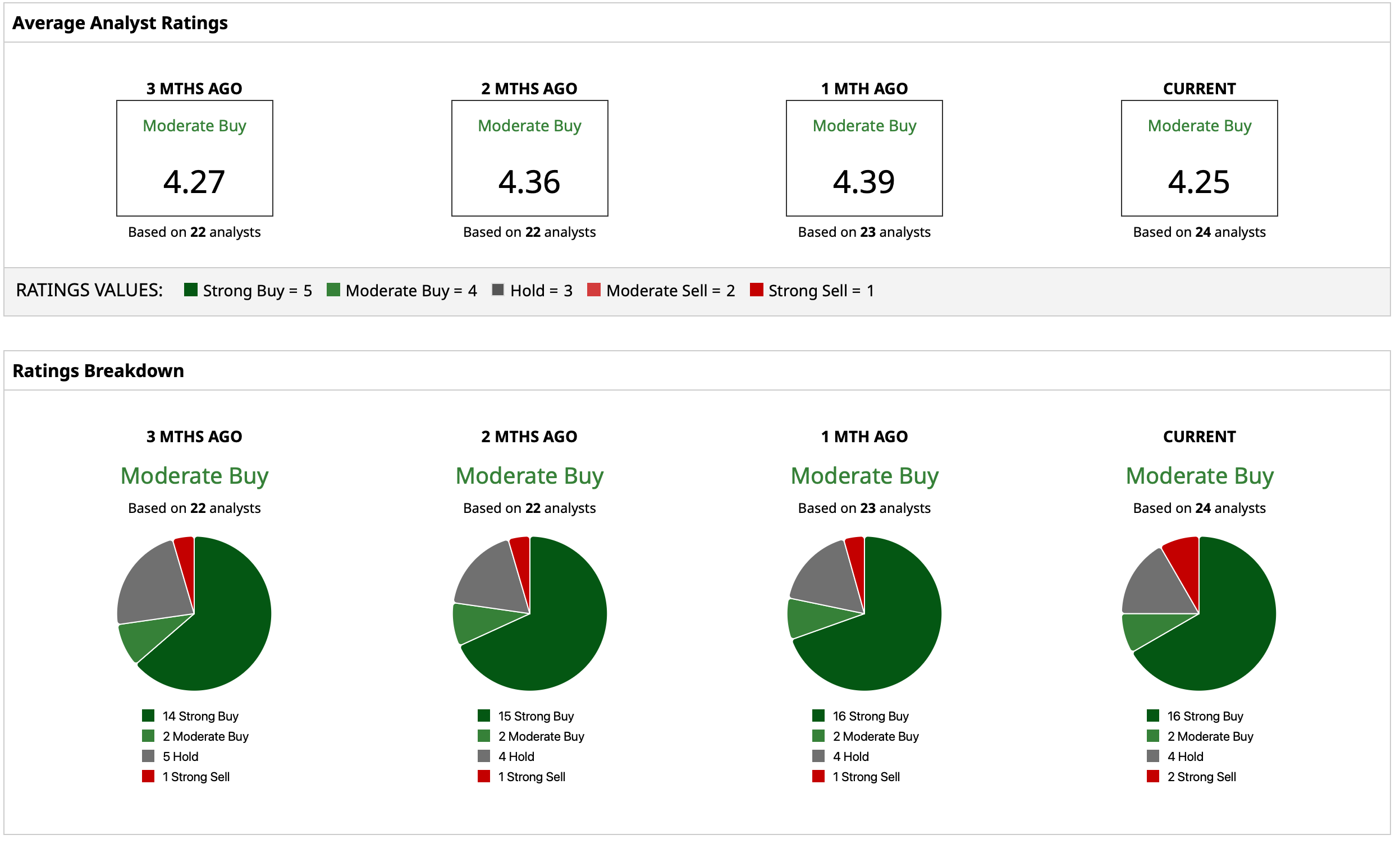

Analyst Opinion of HOOD Stock

Thus, analysts have deemed HOOD stock a consensus “Moderate Buy,” with a mean target price of $105.91. This indicates an upside potential of about 44% from current levels. Out of 24 analysts covering the stock, 16 have a “Strong Buy” rating, two have a “Moderate Buy” rating, four have a “Hold” rating, and two have a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

The Selloff in Robinhood Stock Shows Just How Much Wall Street Was Counting on Crypto MicroStrategy’s Market Cap Is Less Than Its Bitcoin Holdings and MSTR Stock Has Halved in Just the Past Year. What Gives? Why were Bitcoin and COIN Shares Stuck in Neutral? Capital Group Is Doubling Down on MicroStrategy. Should You Buy MSTR Stock Here Too?