PayPal (PYPL) will release its first-quarter 2026 earnings on Tuesday, May 5. Ahead of the release, PYPL’s management unveiled a structural reorganization that simplifies operations into three core segments, including Checkout Solutions & PayPal, Consumer Financial Services & Venmo, and Payment Services & Crypto. This realignment signals a strategic push to streamline operations, improve execution, and accelerate growth.

Notably, separating high-value assets, particularly Venmo, into a standalone reporting unit is significant. It reflects Venmo’s importance as a primary driver of growth while also giving management more flexibility. This could open the door to strategic options such as partnerships, a spin-off, or a potential sale.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Venmo remains a bright spot for PayPal. The platform generated $1.7 billion in revenue in 2025, up 20% year-over-year (YOY). Moreover, it marked 14% increase in average revenue per account. Venmo is deepening monetization while maintaining strong user engagement. With over 100 million active users reported at the end of Q4, Venmo is evolving into a broader financial ecosystem, which could justify a premium valuation.

However, the optimism around structural improvements and asset quality is tempered by near-term headwinds. Macroeconomic pressures, including elevated energy costs and cautious consumer spending, are likely to weigh on transaction volumes. Moreover, competition in digital payments is rising. And PayPal is facing challenges in Germany, one of the company's important growth markets. At the same time, PayPal’s decision to step up investments to support long-term growth may compress earnings in the short run.

Also, market behavior around earnings warrants caution. PayPal’s stock has a history of negative post-earnings reactions, declining in three of the past four quarters, including a sharp drop of 20.3% following its last report.

Nevertheless, the recent decline in the stock price has eased valuation concerns, potentially limiting further downside. Over the past year, the stock has underperformed the broader market. Moreover, it is down 24.78% from its 52-week high of $79.50.

The options market is signaling a move of about 7% in either direction following the report, which is slightly below the average swing seen in recent quarters.

PayPal’s Q1 Earnings to Decline

PayPal’s Q1 could show continued softness in its top line growth rate, while its earnings will likely decline. For the first quarter, management expects top line revenue to grow in the low single digits on a currency-neutral basis. This signals a moderation in transaction volumes.

Management has indicated that transaction margin dollars will decline slightly in Q1, reflecting rising competition and increased investment in platform capabilities.

Macroeconomic conditions further complicate the outlook. Slowing consumer spending across key markets is emerging as a meaningful headwind, particularly as inflationary pressures, including elevated energy costs, erode discretionary income. Moreover, PayPal’s significant global footprint amplifies this exposure. In Germany, the company’s growth is expected to soften amid a heightened competitive landscape and the rise of alternative payment solutions taking share.

Nonetheless, Venmo and buy now, pay later (BNPL) will continue to sustain momentum, supporting PayPal’s growth.

On the earnings front, the outlook remains cautious. Management has guided toward a mid-single-digit decline in adjusted earnings per share, with consensus estimates currently at $1.27, implying a YOY contraction of roughly 4.5%. The projected decline reflects the impact of higher investments. Moreover, it reported weaker-than-expected fourth-quarter performance.

Is PayPal Stock a Buy Now?

PayPal is facing heightened competition in the digital payments space. Further, a challenging macroeconomic backdrop will likely weigh on its growth rate. In addition, the company’s increased investment could affect its profitability in the near term. However, PayPal will continue to benefit from ongoing momentum in Venmo and its BNPL offerings.

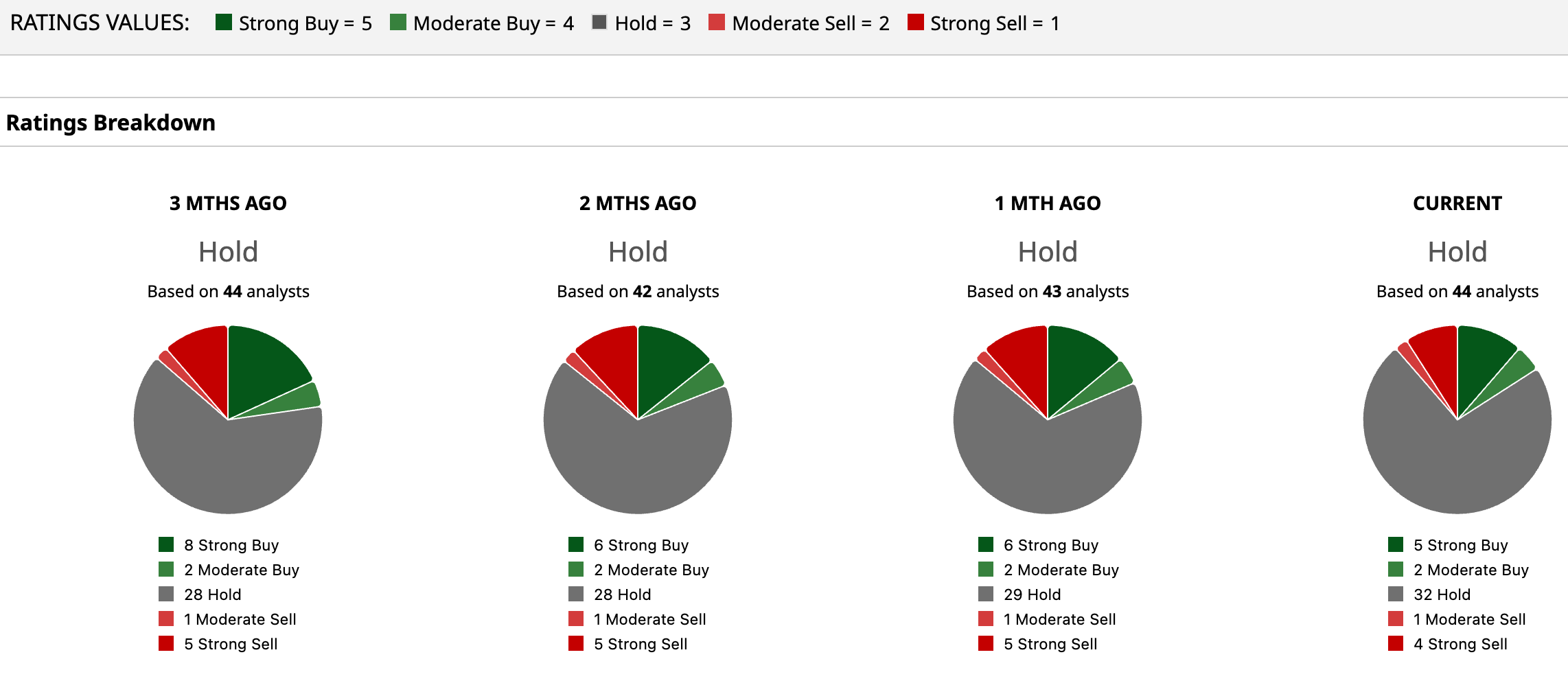

While PYPL stock has lost significant value, easing valuation concerns, investors should exercise caution ahead of the Q1 earnings release. Moreover, analysts maintain a “Hold” rating on PYPL stock ahead of Q1 earnings release.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.