For most of the Grains sector, Friday's session marks the end of the week, month, quarter (and in wheat the marketing year), and meteorological season.

Rain is in the forecast as North America transitions from meteorological spring to meteorological summer, a situation that in days gone by could spark selling interest.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

This time around the calendar, there is a good deal of hullaballoo over something called a “Super El Nino”. Though the US does tend to get hotter during summer most years.

Morning Summary: It’s pre-dawn Friday morning as I write this Commentary. The month of May is finally, mercifully, set to come to an end and frankly, from a personal point of view, this can’t come soon enough. Those focused on the Grains sector have much to look forward to today as well as Friday marks the end of the week (naturally), the last trading day of the month, which is also the last trading day of the third quarter for corn and soybeans, the end of marketing year for the wheat sub-sector, and the end of meteorological spring. It’s the latter that will likely garner the most attention over the coming days as the end of spring means the beginning of meteorological summer. Much of the US Midwest, aka the Eastern Corn Belt, has seen favorable weather conditions this season, with the din rising over a “Super El Nino” as we move into summer. In other words, the green fields we see today will be replaced by a desert across the entire US, at least according to some of the loudest voices in the industry. As for me, I’ll wait and see. I seem to recall we transition into summer every year, meaning weather tends to get hot and dry.

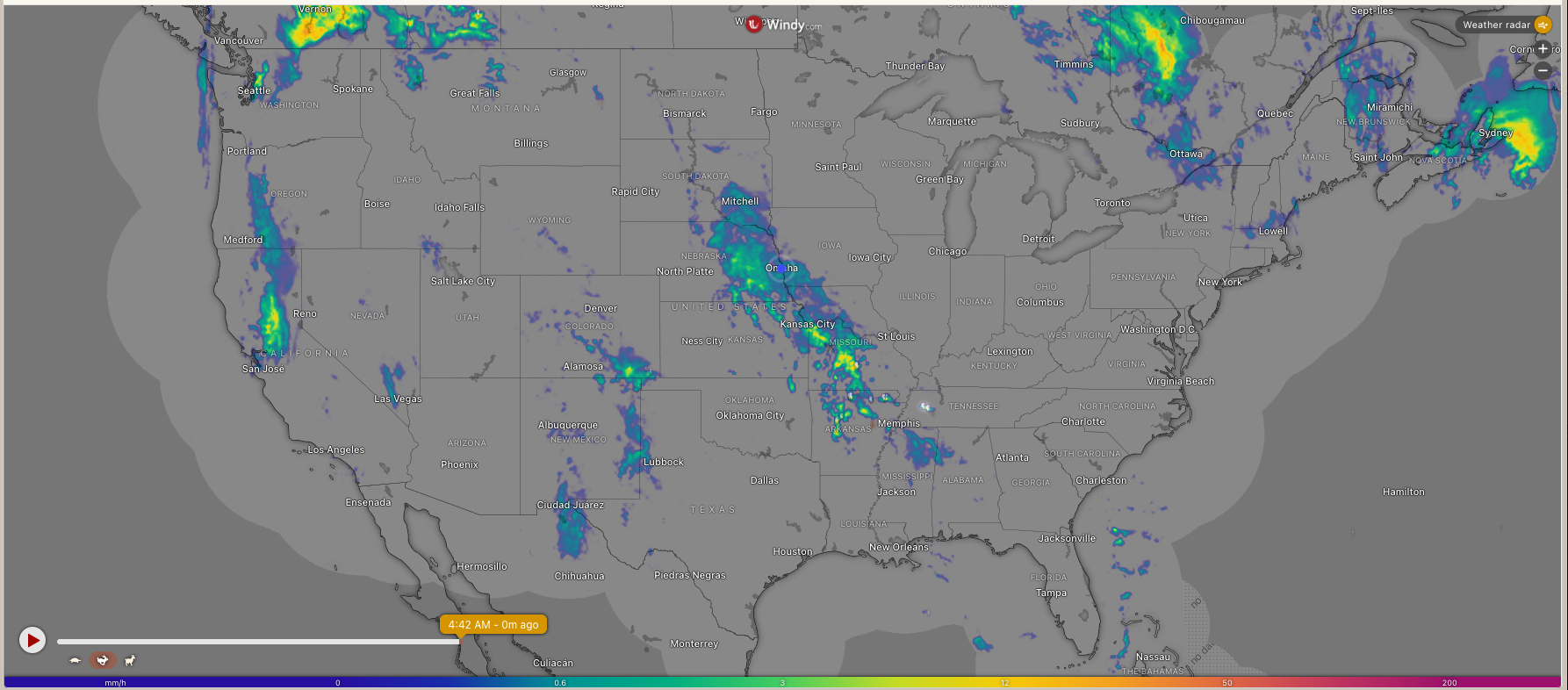

Corn: The corn market was in the red to start the day on light overnight trade volume. July (ZCN26) was down 2.75 cents at this writing, and on its session low, while registering 20,000 contracts changing hands. Recall July finished Thursday’s session 3.25 cents in the green, followed by the National Corn Index coming in roughly 3.75 cents higher for the day last night. This put national average basis at 37.75 cents under July futures as compared to the previous 10-year low weekly close for this week of 39.5 cents under July. Again, Friday is the end of Q3 of the 2025-2026 marketing year, with the National Corn Index priced at $4.18 as compared to the Q2 final price of $4.08. In other words, US supply and demand didn’t change all that much during the spring season. As for new-crop, both September (ZCU26) and December (ZCZ26) futures were down about 2.0 cents pre-dawn, both at or near overnight lows. A look at Friday’s weather forecast and we see rain is expected for much of the US Plains and Midwest growing areas. Early morning radar shows a band of rain moving across Nebraska into Iowa. In days gone by, this would’ve been enough to keep new-crop corn under pressure.

Soybeans: The oilseed sub-sector was mostly lower, with soybeans the outlier this time around the clock. I’ll get to beans in a moment, but let’s start with soybean oil. Recall it was bean oil leading the way higher Thursday with the July issue closing 1.44 cents (1.9%) in the green. Overnight through early Friday morning we see the same July issue slipped as much as 0.6 cent and was down 0.05 at this writing. Some of the pressure might’ve been tied to diesel fuel with the spot-month distillates contract down 4.9 cents (1.4%) pre-dawn. Over in soybeans, July (ZSN26) was up 1.5 cents after rallying as much as 6.25 cents overnight on light trade volume of roughly 14,000 contracts. July finished Thursday’s session with a gain of 9.25 cents followed by the National Soybean Index coming in 9.5 cents higher for the day. On the penultimate evening of Q3, the Index was priced at about $11.32 as compared to the end of Q2 price of $10.94 and last year’s Q3 price of $9.92. New-crop November (ZSX26) was up 1.25 cents to start the day after adding as much as 5.0 cents overnight on trade volume of 8,100 contracts. Again, based on Friday’s weather forecast, Nov could see selling heading into the weekend.

Wheat: The wheat sub-sector was lower across the board heading into the last trading day of the 2025-2026 marketing year. That being said, based on analysis of the three major National Cash Price Indexes, we can conclude US supply and demand tightened this time around the calendar. The National SRW Index was priced near $5.68 last night as compared to the end of February’s $5.38 and the May 2025 final figure of $4.80. It was a more dramatic change in HRW where the latest Index price was $5.99 versus last year’s $4.68, and this is before the bulk of what is expected to be a short 2026 crop has been harvested. This sets the stage for a good debate about the HRW market this coming weekend. The HRS Index came in last night at $6.25 as compared to the final May 2025 price of $6.03. As for Friday morning, with rain in the forecast across the US Plains and Southeast growing areas we see July HRW (KEN26) down 3.0 cents after slipping as much as 5.75 cents overnight on trade volume of 4,800 contracts. July SRW (ZWN26) dipped as much as 4.25 cents while registering 9,500 contracts changing hands but was only one tick (0.25 cent) lower at this writing.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

What Do We Know About Supply and Demand in the Grains Sector Friday Morning? Soybean Prices Are Moving Higher. Expect More Upside. Corn Prices Are Still Falling, But a Floor Is Close. Try This Swing Trade for Profits Here. Was World Sugar’s Price Weak Considering the Action in Crude Oil?