Delivery major FedEx's (FDX) freight business will become a separate entity from June 1, and analysts at J.P. Morgan like it. Led by Brian Ossenbeck, the firm said, “We have been of the view that the structural improvements underway at legacy Federal Express through Network 2.0 are increasingly visible as the last several quarters of solid execution put the company on a credible path to its calendar year 2029 targets."

Notably, the freight business will trade under the name FedEx Freight and have the ticker FDXF. And for every two FedEx shares owned, FedEx shareholders will receive one share of FedEx Freight.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About FedEx

Founded in 1971, FedEx is one of the world’s largest transportation and logistics companies, specializing in express parcel delivery, ground shipping, freight transportation, e-commerce logistics, and supply chain management, among others. And FedEx Freight will be the first subsidiary of the company to get listed, which includes FedEx Express, FedEx Ground, FedEx Office, FedEx Logistics, and FedEx Supply Chain.

Valued at a market cap of $95.4 billion, FDX stock has had an impressive 2026 so far, rising 42.4%. The stock also offers a dividend yield of 1.47%, and with a payout ratio of under 30%, there remains further headroom for growth.

www.barchart.com

www.barchart.com However, with FedEx Freight going its own way, what effect will it have on FDX stock? Let's find out.

Fine Move by FedEx?

Well, J.P. Morgan thinks it to be. Ossenbeck and his team believe the SOTP value of the remaining business is $460 per share, which implies an upside potential of about 12% from current levels. Commenting further, the analyst said, “Overall, while the stock has had a strong run over the past year, we still believe there is attractive upside relative to the rest of the sector based on our SOTP math with the spin set to serve as a near-term catalyst that should improve transparency as idiosyncratic initiatives at both entities make progress.”

Moreover, the strategic logic behind the separation rests on a straightforward premise that two distinct management teams operating under two separate cost structures will give shareholders a far cleaner and more transparent view of what each business is actually worth. Management has also set out a medium term target of expanding operating margins to around 15%, which would represent a 300 basis point improvement over the fiscal 2026 baseline of 12%.

The decision to spin off the freight segment carries its own margin logic too. In the most recent quarter, the Express segment operated at a 7.4% margin, while the Freight segment contributed just 0.4%, a dramatic deterioration from the 12.5% it had recorded in the prior year period. Revenue within that segment also contracted, falling 5% yearly in the third fiscal quarter of 2026. Removing that drag from the consolidated picture will allow the underlying margin profile of the remaining business to improve further.

Additionally, the separation also unlocks capital that the company can redirect toward two of its most consequential ongoing initiatives: DRIVE and Network 2.0. As both programs continue to advance and their benefits flow through the financials, the margin trajectory should strengthen further. Under the DRIVE program, FedEx has already locked in approximately $4 billion in permanent cost reductions, with an additional $1 billion targeted for fiscal 2026.

Whereas Network 2.0 addresses the cost structure from a different angle, bringing Express and Ground operations together under shared facilities to eliminate the redundant infrastructure, sorting capacity, and delivery routes that have historically run in parallel. Roughly 24% of eligible volume is already moving through integrated facilities, with management aiming to reach approximately 65% by the next peak season. As the program matures toward that target, FedEx anticipates a reduction in its facility footprint of around 30% and cumulative cost savings of about $2 billion by fiscal 2027.

Technology investment is providing an additional layer of productivity improvement alongside these structural programs. FedEx has deployed AI-powered tools across a workforce of more than 500,000 employees, spanning applications in route planning, workforce scheduling, and customer service. Among the most tangible of these is Tricolor, an advanced analytics initiative that optimizes pickup and delivery routing in ways that are already producing measurable reductions in cost per stop and better utilization of physical assets. Taken together with the structural programs underway, the medium- to long-term margin outlook for the business appears genuinely encouraging.

On the growth side, FedEx has identified data center logistics as a high-value vertical worth pursuing with dedicated resources. The accelerating global buildout of AI infrastructure, cloud computing capacity, and broader digital infrastructure is generating sustained demand for time-sensitive, high-value shipments covering servers, networking hardware, and associated components. The company has assembled a specialized sales team focused exclusively on this vertical, offering tailored solutions and premium service tiers designed around the specific requirements of these customers. As that vertical matures within the FedEx portfolio, it has the characteristics of a durable and meaningful growth contributor over time.

However, the company should find ways to register growth organically. It will be tough when the economic environment comes under pressure as crude prices remain elevated. The initiatives, though laudable and somewhat appropriate in the current environment, should not be the default strategy of the company. Rather, as and when the economy comes out of its uncertainties, FedEx should be ready to seize the opportunity to continue to be the logistics major it is.

Q3 Beat

Amid all the upheaval due to the freight business spin-off, FedEx's Q3 results managed to exceed expectations.

Revenues increased by 8% from the previous year to $24 billion, with earnings going up to $5.25 per share from $4.51 per share in the year-ago period. Notably, the latter came in much higher than the consensus estimate of $4.15 per share.

Moreover, the company has raised its revenue guidance for fiscal 2026. While earlier it was expecting revenue growth to be between 5% to 6%, it is now at 6%-6.5%. For EPS, the projections are at $16.05 to $16.85 per share, up from $14.80 to $16 earlier.

Then, for the nine months ended February 28, 2026, FedEx's net cash from operating activities rose to $5.66 billion from $4.52 billion in the same period a year ago. Overall, the company closed the quarter with a cash balance of $8 billion, which was much higher than its short-term debt levels of $5 billion.

FedEx is trading at reasonable levels as well. While its forward P/E of 20.23x almost matches the sector median, its forward P/S and P/CF of 1.02x and 12.03x are below the sector medians of 1.86x and 14.90x, respectively.

Analyst Opinion

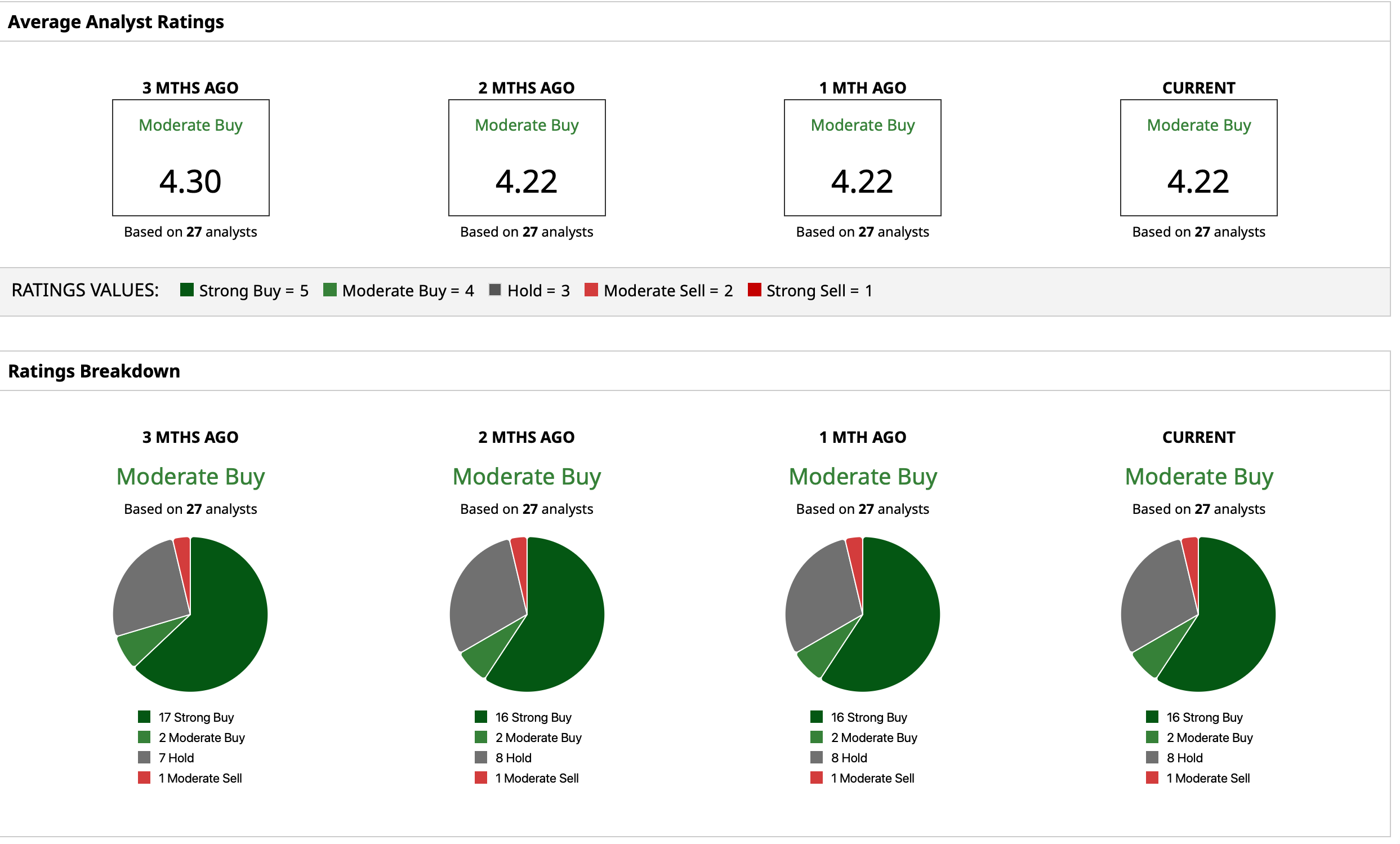

Thus, analysts have deemed FDX stock to be a “Moderate Buy.” The mean target price has already been surpassed, and the high target price of $479 indicates an upside potential of about 16.5% from current levels. Out of 27 analysts covering the stock, 16 have a “Strong Buy” rating, two have a “Moderate Buy” rating, eight have a “Hold” rating, and one has a “Moderate Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Lululemon Stock Has Crashed 60% Over the Past Year, But 1 Ugly Distraction Is Finally Gone Micron Stock Just Joined the Trillion-Dollar Club. Wall Street Says MU Still Has Room to Run. As ARR Swells on AI Tailwinds, CrowdStrike Stock Is a Cash Flow Machine Marvell’s Q1 Earnings Strengthen Its Bull Case — But MRVL Stock Isn’t a Screaming Buy Yet