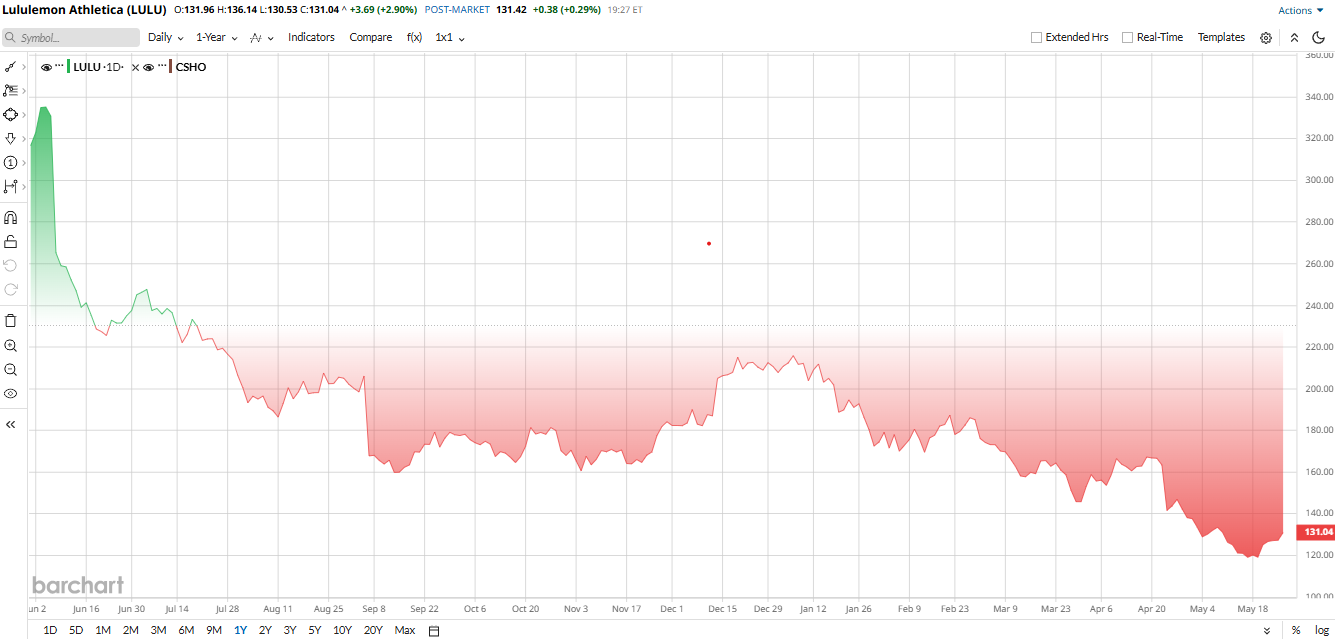

Lululemon (LULU) has been stuck in a rough stretch. The stock has fallen nearly 60% over the past year and about 37% in 2026, as North American sales weakened, tariffs pressed margins, and the founder’s proxy fight kept the market on edge.

Now that fight is easing. Lululemon reached a deal with founder Chip Wilson that pauses his public criticism and gives his side two board seats, and investors liked the news enough to push the stock up about 3% in Wednesday trading. That does not fix the business overnight, but it does remove one ugly distraction.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com On valuation, the picture is mixed. LULU trades at 1.36 times sales versus a sector median of 0.89, so it is not cheap on revenue. But its price-to-earnings ratio of 10x is below the sector’s 16x, which makes it look much more reasonable on profits. That is why this stock feels tricky. It is not expensive enough to ignore, but it is not cheap enough to call a clean bargain either.

Why Founders Deal Matters

The founder deal matters because it clears the air. Wilson has been loud about the brand, the board, and the company’s direction. Now the company gets a break from that noise, and management gets a little more room to focus on the turnaround. The truce should let incoming CEO Heidi O’Neill focus on the business instead of the boardroom fight. That is the right move for investors, because Lululemon needs better products and better execution more than it needs more drama.

Lululemon’s Tops Q4 Earnings Estimate

The latest quarter was better than the market feared, but it was not a blowout. For the fourth quarter of fiscal 2025, revenue rose 1% to $3.6 billion, while full-year revenue increased 5% to $11.1 billion.

Gross profit fell 8% to $2 billion, while operating income dropped 22% to $812.3 million. Adjusted EPS came in at $5.01, down from $6.14 a year earlier. That decline shows how much pressure tariffs and markdowns are putting on profitability.

Still, Lululemon’s balance sheet remains a major positive. The company ended the quarter with $1.8 billion in cash and cash equivalents and generated $1.6 billion in operating cash flow during the year. That gives management flexibility to invest in new products and international expansion even during a slowdown.

Management is trying to reset the story. Interim Co-CEO and Chief Financial Officer Meghan Frank said the company is focused on bringing in “new and differentiated products” while improving full-price selling in North America.

Looking ahead, Lululemon is all set to report its Q1 earnings on June 4. Wall Street expects revenue of about $2.4 billion to $2.43 billion and adjusted EPS of $1.67, both below the company’s earlier outlook and a sign that North American demand is still under pressure. Investors will watch full-price selling, markdowns, and margin trends closely after tariffs and softer traffic hurt the last outlook.

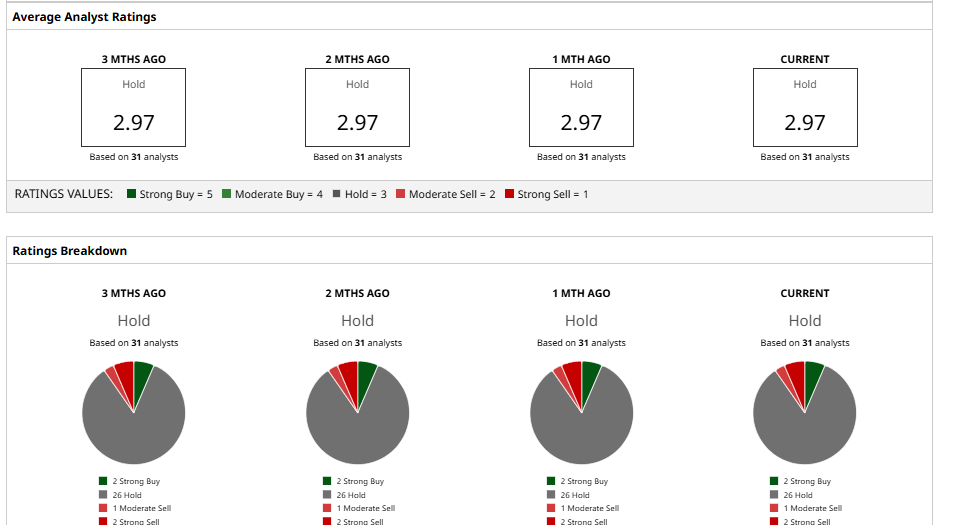

What Do Analysts Think of LULU Stock

Wall Street remains cautious on the stock. For example, Morgan Stanley lowered its price target to $185 and kept an “Equal Weight” rating, saying the company still needs stronger product momentum. Goldman Sachs trimmed its target to $200 and pointed to slowing North American demand as a concern.

Baird also stayed “Neutral” with a $170 target, while Jefferies cut its target to $145 and maintained a “Hold” rating. Analysts continue to like Lululemon’s brand strength and international growth, especially in China, but many believe margins and growth could remain under pressure through 2026.

The broader analyst consensus is still mostly “Hold.” Yet the average 12-month price target of $180 still implies an expected upside of 37% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Lululemon Stock Has Crashed 60% Over the Past Year, But 1 Ugly Distraction Is Finally Gone Micron Stock Just Joined the Trillion-Dollar Club. Wall Street Says MU Still Has Room to Run. As ARR Swells on AI Tailwinds, CrowdStrike Stock Is a Cash Flow Machine Marvell’s Q1 Earnings Strengthen Its Bull Case — But MRVL Stock Isn’t a Screaming Buy Yet