Marvell Technology (MRVL) delivered solid first-quarter fiscal 2027 financial results. The semiconductor company posted solid revenue growth, raised its long-term expectations, and signaled that demand across its AI infrastructure portfolio remains exceptionally strong. In particular, Marvell’s data center business remains the biggest beneficiary of the ongoing AI spending boom.

Further, management’s guidance indicates that Marvell has entered a phase where its growth is expected to accelerate, supporting the stock’s bull case.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

However, investors shouldn’t rush to buy MRVL stock as valuation remains the key concern after a sharp rally.

www.barchart.com

www.barchart.com Marvell’s Growth to Accelerate

Marvell reported quarterly revenue of $2.42 billion, up 28% year-over-year and 9% sequentially. Its adjusted earnings per share (EPS) rose 29% to $0.80. More importantly, management pointed to exceptionally strong bookings across its data center portfolio, signaling that demand remains robust. That strength is now translating into materially stronger guidance.

For the second quarter, Marvell expects revenue to rise 12% sequentially and 35% year-over-year at the midpoint. More importantly, the company expects data center revenue to grow in the mid to high teens sequentially and roughly 45% annually, marking an acceleration in growth.

A major driver behind that momentum is Marvell’s interconnect business, which has become increasingly critical in large-scale AI deployments.

Management now expects its interconnect business to grow more than 70% year-over-year in fiscal 2027, significantly above its earlier forecast of roughly 50% growth. The increase is being driven by stronger demand for scale-out networking as well as growing contributions from scale-up and scale-across architectures.

The company is also seeing increasing traction in custom AI chips and Ethernet switching. Management said it now has visibility into more than $10 billion in annual custom silicon revenue by fiscal 2029.

Earlier this year, Marvell projected quarterly revenue would approach $3 billion by the end of fiscal 2027. Marvell now expects to hit that milestone by the third quarter instead. Management also raised its expected sequential revenue growth rate for the second half of the year to at least 10%, up from its prior forecast of 8%.

As a result, Marvell now expects fiscal 2027 revenue to grow roughly 40% year-over-year to nearly $11.5 billion, up from its prior forecast of around $11 billion. The data center segment is expected to grow approximately 50% this year.

The longer-term outlook appears even stronger. For fiscal 2028, Marvell expects data center revenue growth to accelerate further to around 55% year-over-year. The company also expects its custom silicon business to more than double, while Ethernet switching revenue continues to ramp.

Overall, Marvell now projects fiscal 2028 revenue of approximately $16.5 billion, up from its earlier forecast of about $15 billion.

Notably, this is the second major upward revision in a relatively short period. Last quarter, management had already increased its fiscal 2028 revenue outlook to $15 billion, about $2 billion above the projection it gave during its December earnings call. The latest increase suggests that customer demand is holding up and strengthening materially.

MRVL’s Valuation a Concern

Marvell’s strong outlook and accelerating growth in data center networking, custom silicon, and interconnect solutions continue to support the bullish case for the stock. The company’s robust revenue momentum is also expected to drive significant earnings growth.

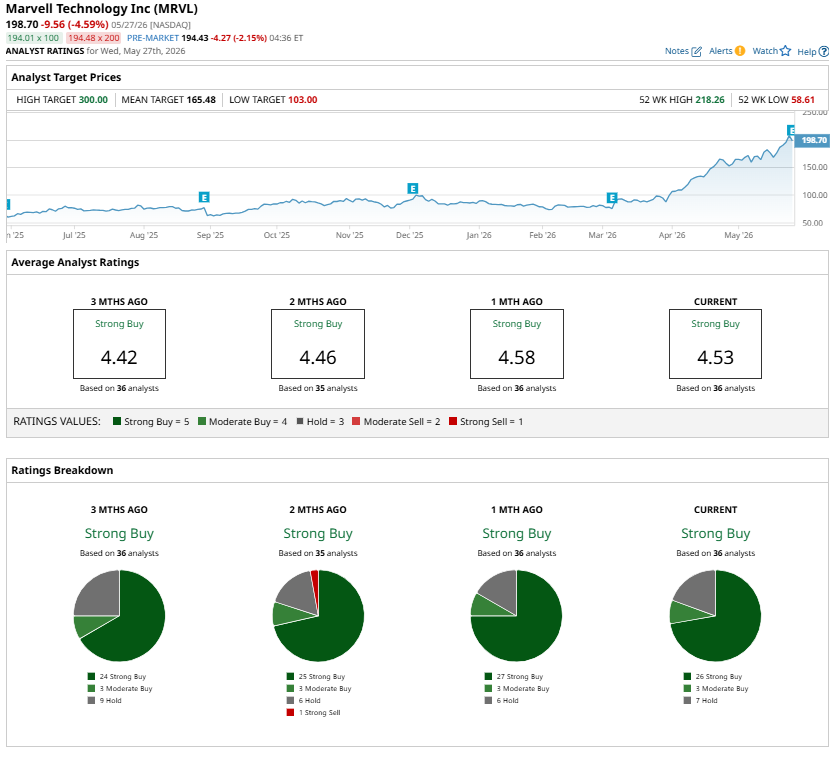

Wall Street analysts remain optimistic about MRVL, with the stock currently carrying a “Strong Buy” consensus rating. Earnings are projected to grow by 41% in fiscal 2027, followed by another increase of more than 48% the following year.

That said, valuation remains a key concern. Marvell is currently trading at 64.5 times forward earnings, a relatively high multiple that suggests much of the positive outlook may already be reflected in the stock price.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Lululemon Stock Has Crashed 60% Over the Past Year, But 1 Ugly Distraction Is Finally Gone Micron Stock Just Joined the Trillion-Dollar Club. Wall Street Says MU Still Has Room to Run. As ARR Swells on AI Tailwinds, CrowdStrike Stock Is a Cash Flow Machine Marvell’s Q1 Earnings Strengthen Its Bull Case — But MRVL Stock Isn’t a Screaming Buy Yet