QIAGEN N.V. QGEN is sending investors a mixed near-term message after first-quarter earnings miss and a reset to its 2026 growth outlook. The stock carries a Zacks Rank #3 (Hold), and the Style Scores tilt defensive rather than directional.

With a VGM Score of D, QGEN screens as “balanced at best” today, especially with Value stronger than Growth and Momentum. The question is whether the company’s profitability and liquidity can steady the story while demand visibility stays choppy.

QIAGEN’s Q1 Print and What Drove the Miss

First-quarter 2026 results pointed to uneven demand and modest execution pressure. Adjusted earnings were $0.54 per share, down 2% year over year, and the result missed the consensus estimate by 1.2%. On a GAAP basis, earnings were $0.33 per share versus $0.41 a year ago.

Revenue was $492 million, up 2% year over year on a reported basis but down 1% at constant exchange rates. The top line also fell short of expectations, missing by 0.8%. Together, the numbers suggest demand did not cooperate evenly across end markets, and the company did not fully offset that with upside elsewhere during the quarter.

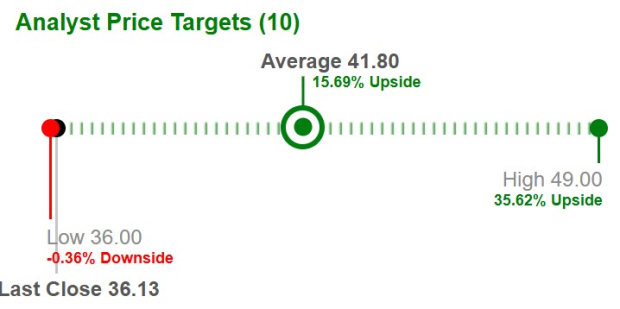

Based on short-term price targets from 10 analysts, the average price target for QIAGEN’s is $41.80, representing a potential 15.69% upside from the last closing price.

Image Source: Zacks Investment Research

QIAGEN’s Offsets: Profitability, Cash Flow, and Balance Sheet

Even with softer demand signals, QIAGEN delivered financial stabilizers that can matter in a reset year. The adjusted operating income margin was 27.4% in the first quarter, reflecting sustained profitability despite targeted investments and headwinds from tariffs and currency movements.

Cash generation also remained constructive. Free cash flow was $54 million in the quarter, supporting ongoing investment needs, including systems and infrastructure initiatives.

The balance sheet adds another layer of flexibility. QIAGEN ended the quarter with $646.3 million in cash and cash equivalents and no current debt. That liquidity can help the company keep funding targeted launches and workflow improvements, even as tariffs and foreign-exchange movements continue to pressure profitability.

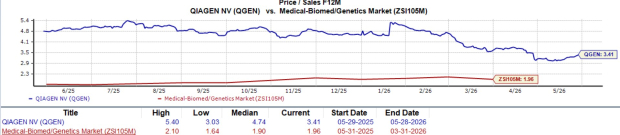

QGEN’s Valuation Framing vs. Benchmarks

The stock’s decline provides important context for the current debate. QIAGEN shares are down 23.7% year to date and also down 23.7% over the past 12 months.

On valuation, QGEN trades at about 3.4 times forward 12-month sales. That is above the Zacks sub-industry and sector comparisons, but below the S&P 500 multiple shown in the same benchmark set.

Image Source: Zacks Investment Research

The $38 price target is framed through a multiple-based approach. It reflects 3.5 times forward 12-month sales, essentially signaling modest upside from recent levels while keeping expectations constrained by the slower growth outlook.

QIAGEN’s Decision Checklist From the Report’s Risks

For investors weighing a buy-versus-hold stance, the downside checklist is clear. QIAGEN remains sensitive to macro conditions and demand fluctuations, including reduced QuantiFERON immigration testing volumes, cautious spending from U.S. Life Sciences customers, and uneven original equipment manufacturer ordering patterns.

Foreign-exchange exposure is another swing factor, given that more than half of revenue is generated outside the United States. Tariffs also pressured profitability in the first quarter, and those costs can complicate margin forecasting while the company continues investing behind launches.

Execution timing in partnerships matters, too. Companion diagnostics programs can deliver multi-year opportunity, but revenue recognition depends on partner timelines and commercial success. QIAGEN reported $115 million in remaining performance obligations tied to companion diagnostic co-development contracts, with roughly half expected over the next 12 to 18 months.

Finally, competitive intensity can lengthen sales cycles when lab budgets tighten. That dynamic is not unique to QIAGEN. Illumina, Inc. ILMN is a major player in sequencing and array solutions used across genomics workflows, and spending cycles in that ecosystem can influence broader purchasing behavior. Thermo Fisher Scientific Inc. TMO also spans a wide range of life sciences research tools and consumables, underscoring how well-funded competitors can pressure pricing and decision timelines in cautious environments.

You can see the complete list of today’s Zacks Rank #1 (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Thermo Fisher Scientific Inc. (TMO): Free Stock Analysis Report

Illumina, Inc. (ILMN): Free Stock Analysis Report

QIAGEN N.V. (QGEN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).