Dell Technologies (DELL) used to be the kind of stock people owned for stability, not excitement. That story has changed fast. The latest earnings season turned Dell into one of the market’s loudest AI hardware winners. Investors are rewarding companies that can actually ship the infrastructure behind artificial intelligence, and Dell is now right in the middle of that trade. The stock has ripped higher double digits, the guidance has jumped, and the business mix is shifting toward AI servers and storage. That is a big change for a company many investors once filed under old-school PC hardware.

AI Server Demand Is Fueling the Rally

Dell’s share price has been one of the strongest in the market this year. Recent figures say the stock is up about 270% year-to-date and roughly 319% over the past year, while another report said it jumped more than 30% in a single session after earnings. That kind of move does not happen unless investors think something real is changing in the business. In Dell’s case, the change is AI server demand. The company said AI server revenue hit $16.1 billion in the quarter, up 757% from a year earlier, while its Infrastructure Solutions Group reached $29 billion in revenue and kept outpacing the PC business.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

By valuation, Dell isn’t screaming “bubble” yet. It trades around 24× trailing earnings with a PEG under 1, which is not out of line for fast growth. The forward P/E is in the low 20x, a premium to old-line PC peers but not wild given its booming segment. Compared to its sector, the stock looks fairly priced or even a little cheap on growth-adjusted terms, since analysts expect major profit gains.

www.barchart.com

www.barchart.com Dell Smashes Q1 Earnings Estimate

Dell’s latest quarter was the kind of report that changes a story. Revenue came in at $43.8 billion, up 88% year-over-year, and adjusted earnings-per-share reached $4.86, up from $1.55 a year earlier. The Infrastructure Solutions Group jumped to $29 billion, while the PC side still contributed $14.6 billion. Dell also posted net income of $3.44 billion. Free cash flow came in at $4.1 billion, and the company returned $2.1 billion to shareholders. That is not just growth. That is growth with cash behind it.

Management also did something even more important than beating the quarter. It raised the guide. Dell now expects fiscal 2027 revenue of $165 billion to $169 billion, up from $138 billion to $142 billion. It also lifted its full-year adjusted EPS view to $17.90 at the midpoint and guided second-quarter revenue to $44 billion to $45 billion with adjusted EPS around $4.80. The company said the AI server business should reach $60 billion in fiscal 2027, up from the earlier $50 billion outlook. That is the number investors really seized on. It says demand is still ahead of supply.

What’s Next for Dell?

Beyond the numbers, Dell is busy building on AI. At its world conference in May, it rolled out new products and partnerships. Notably, it enhanced its AI Factory with NVIDIA platform, which now has over 5,000 customers worldwide. This initiative bundles Dell servers and tools so enterprises can move AI projects from experiment to production. Dell also launched a Deskside Agentic AI solution to secure on-premises AI workstations and new data platform and storage upgrades to feed enterprise AI workloads.

On top of that, Dell started an AI Ecosystem Program to let software firms validate their tools on Dell hardware, speeding real-world deployments.

In other news, Dell just won a huge contract: roughly a $9.7 billion, five-year deal with the U.S. Department of Defense to centralize licenses and cloud services. That’s a vote of confidence in Dell’s infrastructure chops.

Meanwhile, Dell has committed to generous shareholder returns: it just raised its dividend 20% (to $0.63 per quarter) and added a $10 billion buyback authorization. All in all, Dell is doubling down on the AI and data center theme.

Wall Street Opinion on Dell Stock

Wall Street has turned more upbeat, fast. Mizuho lifted its target to $435 and Melius Research to $565 after the results. Wells Fargo also raised its target to $270, while BofA, Evercore, Goldman Sachs, JPMorgan, and Citi have all pointed to Dell’s strong AI position and better execution. More than a dozen brokerages raised their targets, with a new median of $255, up from $170. That tells you how quickly sentiment has shifted.

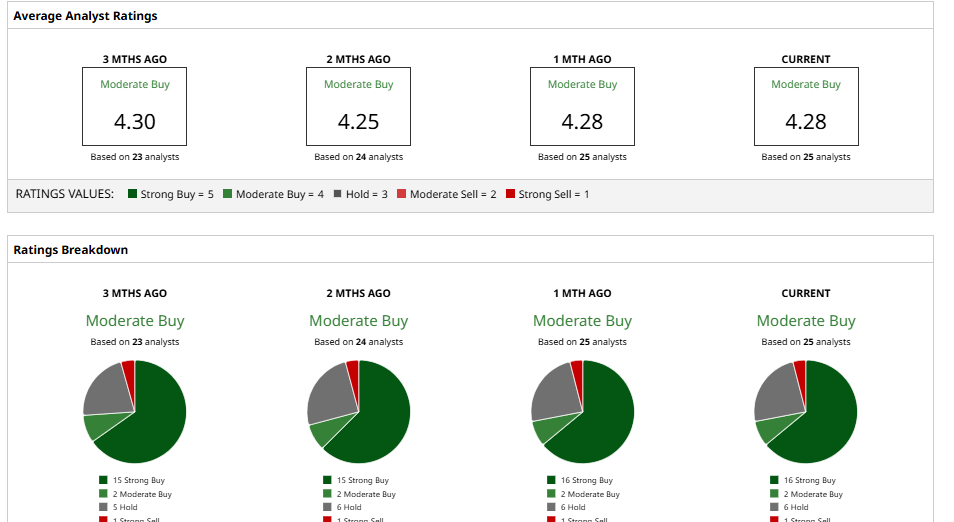

Overall, Dell carries a "Moderate Buy" consensus rating, with a mean price target of about $215, suggesting the stock could pull back by about 54% from its current level. However, that doesn't seem likely, given Dell's transformation from a traditional hardware company into an AI infrastructure leader. After a move this big, Dell has earned its new valuation the hard way, and now it has to keep delivering.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A $5 Billion Reason to Buy Salesforce Stock Now Nvidia CEO Jensen Huang Is Building the Future Faster Than Infrastructure Can Support It Dell Stock Is the New Nvidia of AI Infrastructure Why Okta Is One of the Hottest AI-Driven Stocks to Buy Now