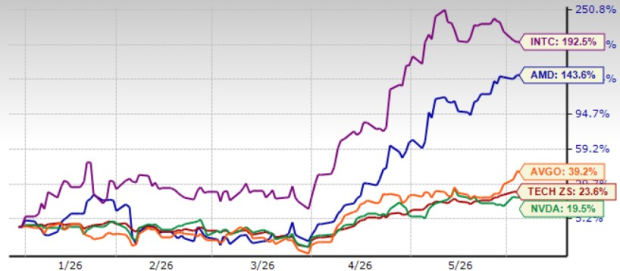

Advanced Micro Devices AMD shares closed at $521.54 on June 2, just shy of the 52-week high of $527.20 the company hit on May 28. It has been benefiting from strong demand for data center EPYC processors and Instinct GPUs. AMD shares have jumped 143.6% year to date (YTD), outperforming the broader Zacks Computer and Technology sector’s return of 23.6%.

However, AMD is facing stiff competition from the likes of NVIDIA NVDA, Broadcom AVGO and Intel INTC across domains, including AI-powered data-centers, high-performance computing and AI PCs, which might limit further appreciation in AMD shares. YTD, shares of NVIDIA, Broadcom and Intel have returned 19.5%, 39.2% and 192.5%, respectively. So, what should investors do with AMD stock?

AMD Stock’s Price Performance

Image Source: Zacks Investment Research

Expanding Data Center Footprint Boosts AMD’s Prospects

AMD is entering a stronger growth phase as AI infrastructure demand shifts the company’s mix toward the Data Center segment, revenues from which surged 57% year over year to $5.8 billion, driven by EPYC CPUs and Instinct GPUs. AMD’s core upside case is that AI inference and agentic AI are expanding demand not only for GPUs, but also for high-performance server CPUs used for orchestration, data movement, and head-node workloads. AMD management guides Q2 Data Center revenues to approximately $11.2 billion, implying another 46% year-over-year increase.

AMD reported server CPU revenue growth of more than 50% in the first quarter of 2026 and guided server CPU growth above 70% year-over-year in the second quarter of 2026. AMD management raised its estimate of the server CPU total addressable market (TAM) from roughly $60 billion to over $120 billion by 2030, driven by growing CPU requirements for inference, orchestration, and agentic AI workloads. AMD believes it can continue gaining share with its EPYC Turin and upcoming Venice product families.

AMD's AI strategy is gaining traction through large-scale partnerships. Meta Platforms plans to deploy up to 6 GW of AMD Instinct GPUs. Expanding relationships with OpenAI and other hyperscalers is a key catalyst. Management stated that customer forecasts for MI450 deployments are exceeding original expectations and that AMD sees a path to "tens of billions of dollars" of annual Data Center AI revenue in 2027.

Meanwhile, AMD is moving beyond individual chips into integrated AI infrastructure. The upcoming Helios rack-scale platform combines MI450 GPUs with Venice CPUs, while management emphasized strong customer validation activity and successful sampling. AMD also highlighted leadership performance-per-watt, growing ROCm software maturity, and a broad portfolio spanning CPUs, GPUs, adaptive computing and custom silicon.

AMD’s Earnings Estimate Revision Shows Rising Trend

The Zacks Consensus Estimate for second-quarter 2026 earnings is pegged at $1.60 per share, up 11.1% over the past 30 days. AMD reported earnings of 48 cents in the year-ago quarter.

Advanced Micro Devices, Inc. Price and Consensus

Advanced Micro Devices, Inc. price-consensus-chart | Advanced Micro Devices, Inc. Quote

The consensus mark for 2026 earnings is pegged at $7.21 per share, up 7.6% over the past 30 days, suggesting 72.9% growth from 2025’s reported figure.

AMD’s Gross Margins Under Pressure from Unfavorable Mix

AMD expects the ramp of MI450 beginning the third quarter of 2026 and into the fourth quarter to hurt gross margin expansion. While MI450 and Helios represent major growth drivers, management explicitly noted that MI450 carries gross margins below the corporate average. As AI accelerators become a larger portion of revenue, the mix could pressure overall profitability and partially offset benefits from higher-margin server CPUs and embedded products.

In the first quarter of 2026, gross margin expanded 170 basis points (bps) to 55%, driven by a favorable product mix, including a higher data center revenue contribution. For the second quarter of 2026, AMD expects gross margin to be roughly 56%, driven by higher CPU sales.

Moreover, supply constraints are expected to limit upside. AMD has repeatedly acknowledged that demand exceeds available supply, particularly at advanced nodes and packaging. Management stated that supply remains tight through 2026 and that future growth depends on securing sufficient capacity from partners such as TSMC.

AMD also expects PC shipments to be lower in the second half due to higher memory and component costs. This is expected to hurt higher margin client revenues, likely putting gross margin under pressure. Moreover, lower-margin gaming revenues are also expected to decline due to higher memory and component costs.

AMD Shares Are Overvalued

AMD shares are overvalued, as suggested by a Value Score of F. The AMD stock is trading at a forward 12-month price/earnings (P/E) of 57.24X compared with the broader sector’s 26.69X.

AMD shares are trading at a premium compared with peers, including NVIDIA and Broadcom. Shares of NVIDIA and Broadcom are trading at a P/E multiple of 23.75 and 31.56, respectively.

AMD Stock’s Valuation

Image Source: Zacks Investment Research

Here’s Why AMD Stock is a Hold Now

AMD’s expanding portfolio and growing data center AI footprint are expected to improve its top-line growth over the long term. The investment case for AMD is increasingly centered on AI infrastructure, server CPU share gains, and hyperscaler GPU deployments, which are driving unusually strong revenue growth and expanding long-term market opportunities. So, investors currently holding the stock should stay put. However, AMD’s near-term prospects are limited given stiff competition and stretched valuation.

AMD currently has a Zacks Rank #3 (Hold), suggesting that it may be wise for investors to wait for a more favorable entry point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intel Corporation (INTC): Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).