Adobe (ADBE) is walking into a defining moment on Thursday, June 11, releasing its Q2 FY2026 earnings results after markets close in a report carrying enormous weight. Leadership changes, deepening fears around artificial intelligence (AI) competition, and a stock that has bled nearly 27.49% year-to-date (YTD) have all sent the stakes sky high on what Adobe delivers now.

Adobe's Firefly generative AI sits at the very top of the company's growth ladder right now. Firefly crossed $250 million in ending ARR, and AI first annual recurring revenues (ARR) tripled year-over-year (YOY). The June 11 report now has to prove the trajectory holds solid and carries enough firepower to reverse the stock's brutal decline.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Also, Adobe is managing three game changing developments alongside its earnings season. CEO Shantanu Narayen announced his exit after nearly two decades at the helm, bringing leadership uncertainty into the picture at a time the market can least afford it. Adobe is acquiring Semrush for $1.9 billion, and the company also authorized a massive $25 billion stock repurchase program running through April 2030.

Investor confidence is building ahead of the earnings report. Renowned investor Michael Burry called Adobe a "fat pitch," citing Firefly's enterprise integrations as a powerful moat that competitors will struggle to crack. Whether the earnings report confirms or crushes that bullish view will define Adobe's strategic trajectory and investor trust for all of 2026.

About Adobe Stock

Headquartered in San Jose, California, Adobe develops software and cloud-based platforms spanning digital media, document management, marketing, analytics, ecommerce, advertising, and customer experience management.

Adobe commands a market cap of $104.5 billion, and its portfolio covers creative design tools, PDF and document solutions, digital marketing technologies, business workflow applications, and generative AI powered content creation services.

ADBE stock has taken investors on a rough ride. Shares are down 39.1% over the last 52 weeks.

www.barchart.com

www.barchart.com Coming to valuation, ADBE stock is currently trading at 13.39 times forward adjusted earnings, a multiple sitting at a discount to both the industry average and the stock's own five-year average multiple. This signals a potential entry point for investors who believe the turnaround story has legs.

Adobe Surpasses Q1 Earnings

Adobe reported its Q1 FY2026 earnings on March 12 and topped expectations on both the top and bottom lines. The stock still tanked about 7.6% on March 13 despite the record Q1 beat, because longtime CEO Shantanu Narayen dropped a bombshell by announcing his departure after 18 years at the helm.

Narayen's exit carries particular weight because he was the chief architect of Adobe's enormously successful shift to the Creative Cloud subscription model, and that departure lands at a critical inflection point where Adobe faces existential threats from generative AI startups and open-source competitors.

Setting that aside, revenue grew 12% YOY to $6.40 billion, clearing analyst estimates of $6.28 billion. Adjusted EPS rose 19.3% from the year-ago value to $6.06, surpassing analyst estimates of $5.87.

Acrobat and Express, Creative Cloud Pro, the overall strength in CXO enterprise solutions, and Adobe's AI first applications all powered that momentum forward. Moreover, total Adobe ending ARR reached $26.06 billion, growing 10.9% YOY. Total customer group subscription revenue came in at $6.17 billion, growing 13% YOY.

Remaining Performance Obligations (RPO) exiting the quarter stood at $22.22 billion, growing 13% YOY while cRPO grew 12%. Cash flows from operations hit a Q1 record of $2.96 billion. Plus, the company exited Q1 with ending cash and short-term investments of $6.89 billion.

Looking ahead, for Q2 FY2026, Adobe is targeting total revenue of $6.43 billion to $6.48 billion. Business Professionals and Consumers subscription revenue is expected in the range of $1.80 billion to $1.82 billion, while Creative and Marketing Professionals subscription revenue is targeted between $4.41 billion and $4.44 billion. Adobe also guided for non-GAAP EPS of $5.80 to $5.85.

On the other hand, analysts are forecasting Q2 FY2026 EPS to grow 15.6% YOY to $4.74. For full FY2026, analysts project the bottom line to grow 11.3% YOY to $19.14, while FY2027 projections call for EPS growth of 14.5% to reach $21.91.

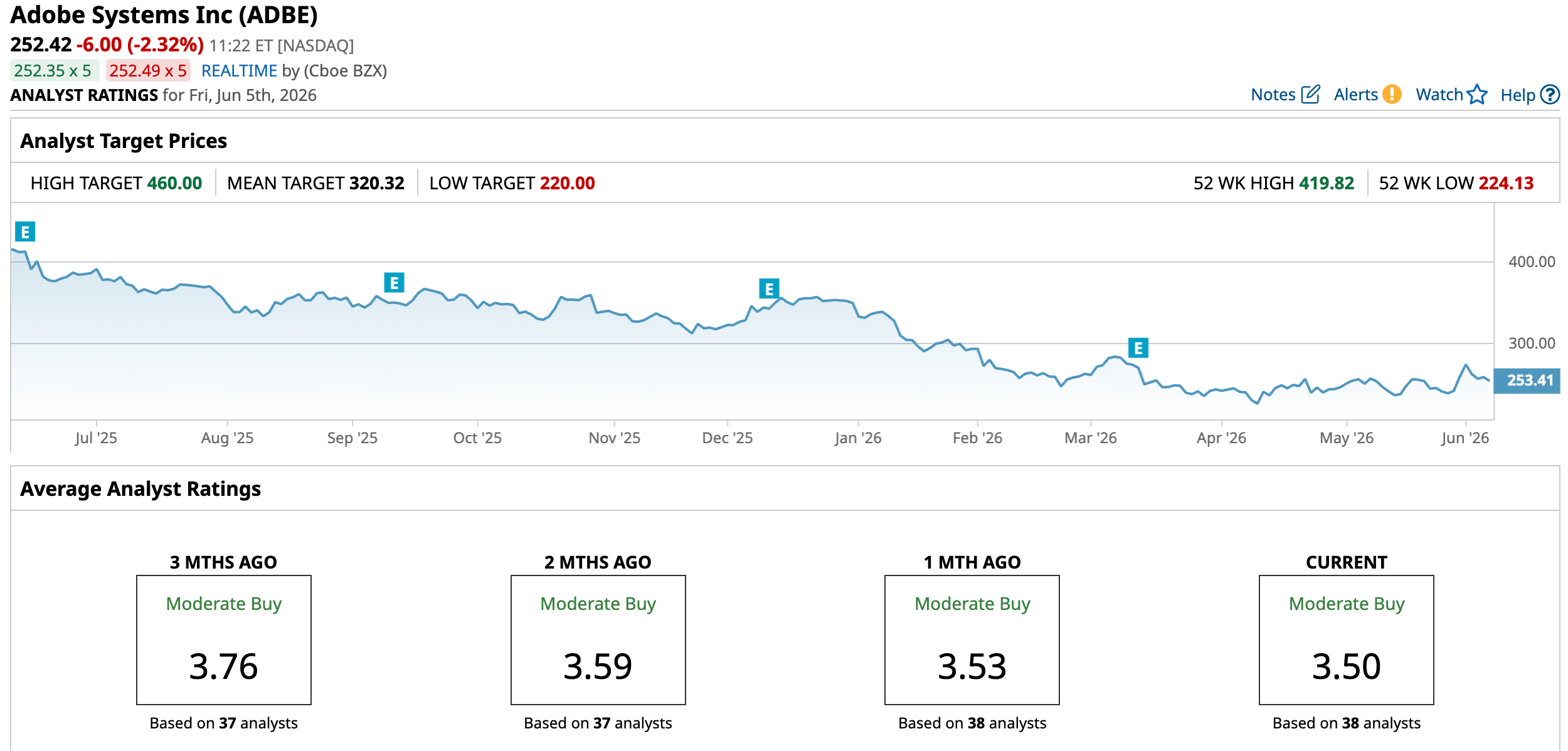

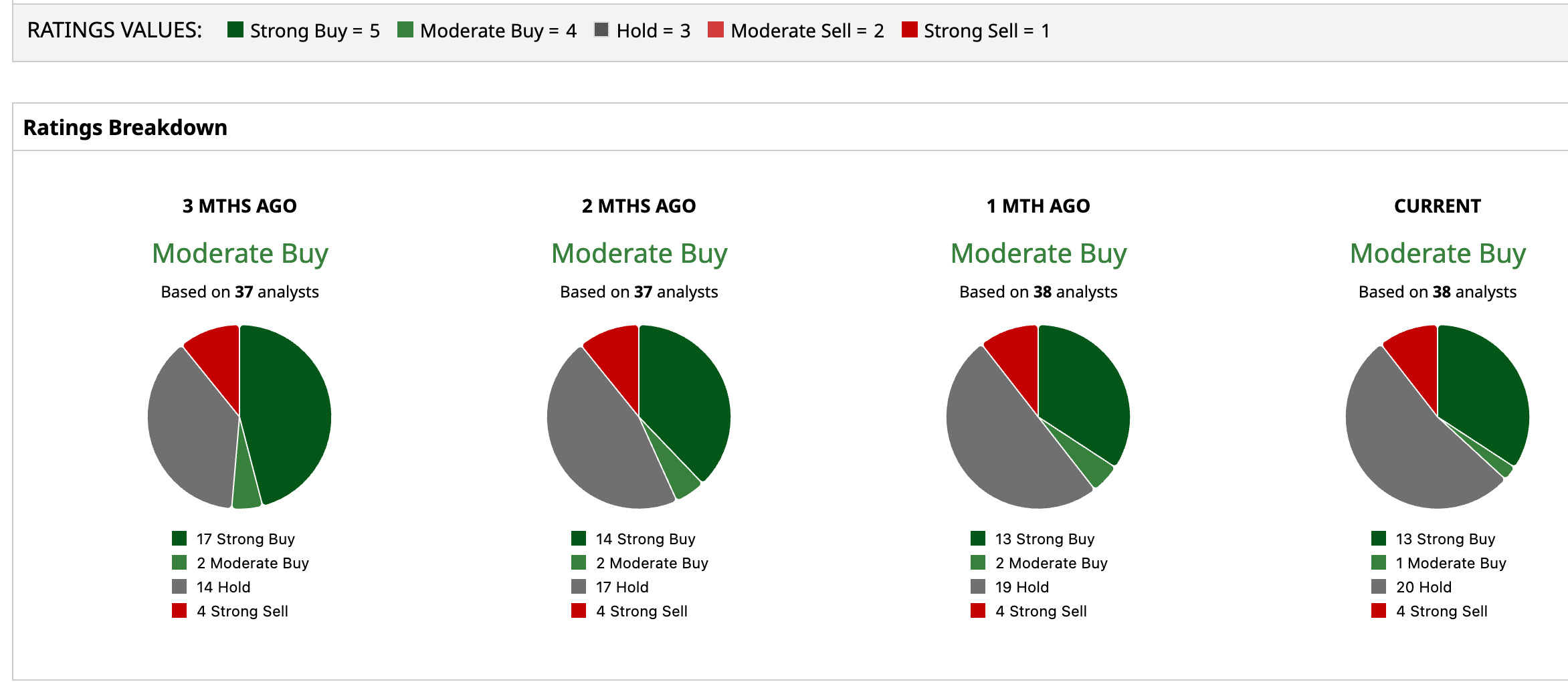

What Do Analysts Expect for Adobe Stock?

Wall Street continues to lean bullish on Adobe, assigning the stock an overall "Moderate Buy" rating. Out of 38 analysts covering the stock, 13 recommend "Strong Buy," one recommends "Moderate Buy," 20 suggest "Hold," and four flag a "Strong Sell."

To that end, the stock’s average price target of $320.32 represents potential upside of 26.9%. Meanwhile, the Street-High target of $460 suggest a gain of 82.24% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Hunting for the Next Nvidia Is No Easy Feat. Small-Cap Tech Stocks Promise Riches but Really Are Just Rags. Dear Adobe Stock Fans, Mark Your Calendars for June 11 Bloom Energy Stock Is Surging. Its CEO Said These Magic Words. Billionaire Mark Cuban Says Let’s Take Health Care Back to 1955 — ‘Patients Get a Bill and if They Can Afford It, They Pay That Bill’