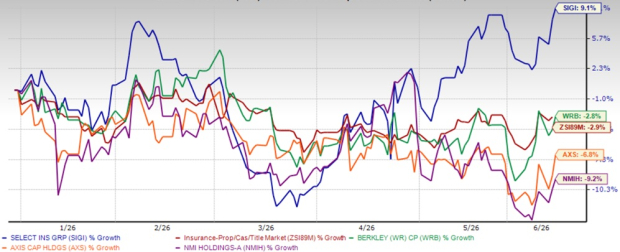

Shares of Selective Insurance Group, Inc. SIGI have gained 9.1% in the year-to-date period, outperforming the industry’s decline of 2.9%. The company’s share price closed at $91.34 on Wednesday and is hovering near its 52-week high of $91.99. This proximity underscores investor confidence. It has the ingredients for further price appreciation.

Selective Insurance has outperformed its peers, including Axis Capital Holdings Limited AXS, NMI Holdings Inc. NMIH and W.R. Berkley Corporation WRB, which have lost 6.8%, 9.2% and 2.8%, respectively, in the year-to-date period.

1 Year Performance - SIGI, AXS, NMIH, WRB & Industry

Image Source: Zacks Investment Research

Target Price Reflects Potential Upside

Based on short-term price targets offered by seven analysts, the Zacks average price target is $92.43 per share. The average indicates a potential 2.4% upside from the last closing price.

SIGI’s Valuation

SIGI’s shares are trading at a premium compared to the industry. Its forward price-to-book value of 1.61X is higher than the industry average of 1.38X, but lower than the Finance sector’s 4.42X and the Zacks S&P 500 Composite’s 8.01X. It currently has a Value Score of A.

Image Source: Zacks Investment Research

SIGI’s Growth Projection Encourages

The Zacks Consensus Estimate for Selective Insurance’s 2026 EPS indicates a year-over-year increase of 5.8%. The consensus estimate for revenues is pegged at $5.5 billion, implying a year-over-year improvement of 3.2%.

The consensus estimate for 2027 EPS and revenues indicates an increase of 13.4% and 3.1%, respectively, from the corresponding 2026 estimates.

Optimistic Analyst Sentiment for SIGI

One analyst has raised estimates for 2026 and 2027 over the past 30 days, against no downward movement. Thus, the Zacks Consensus Estimate for 2026 and 2027 earnings has moved north 0.6% and 0.5%, respectively, over the same period.

SIGI’s Favorable Return on Equity

Return on equity in the trailing-12 months was 13.7%, better than the industry average of 6%. This highlights the company’s efficiency in utilizing shareholders’ funds.

Factors Favoring SIGI Stock

SIGI continues to prioritize underwriting profitability over aggressive premium growth. Strong performance in the Excess & Surplus (“E&S”) segment, with a combined ratio of 89.5% in first-quarter 2026 (vs 92.5% year-ago) and improved Personal Lines profitability, with a combined ratio of 92.8% (vs 98 % year-ago), highlights the benefits of disciplined underwriting and selective risk retention. Management is selectively retaining its best-performing accounts while reducing exposure to underperforming businesses.

SIGI continues to raise renewal rates to address elevated loss-cost trends. The company achieved renewal price increases of nearly 10% in general liability over the past seven quarters, well above industry averages. In commercial auto liability, it witnessed pure price increases of almost 12% in the first quarter. Management believes these rate increases position the company to offset social inflation and improve long-term underwriting profitability.

Selective Insurance is steadily expanding its Standard Commercial Lines business toward a near-national footprint, now operating in 36 states and the District of Columbia. This growth is driven by an agent-based model with around 1,680 partners across 2,940 offices, supporting geographic diversification and more stable, cycle-resilient premium growth.

Higher net investment income continues to support earnings growth. After-tax net investment income increased 18% year over year in the first quarter, benefiting from favorable yields and a conservatively positioned investment portfolio. Selective Insurance expects after-tax net investment income of $465 million in 2026. Strong and reliable returns from its growing fixed-income portfolio, supported by higher returns from its short-term investments, are likely to drive the metric.

Selective Insurance is also investing heavily in artificial intelligence and technology capabilities to enhance underwriting, claims processing and risk management. AI tools have already processed more than 0.5 million claims-related documents, while a significant portion of the company's 2026 strategic technology spending is focused on improving risk selection and pricing accuracy.

Selective Insurance continues to return capital through dividends and repurchases while keeping flexibility for underwriting and investment opportunities. The company continues to prioritize profitable growth and aims to return 20-25% of earnings to shareholders through dividends.

Risks for SIGI

Persistent social inflation in commercial casualty creates some uncertainty around margin improvement. Hence, Selective Insurance is focusing on rate adequacy over growth, which can affect its size.

Property catastrophe exposure remains a key earnings risk. In first-quarter 2026, catastrophe losses added 620 bps to the combined ratio, highlighting earnings volatility. At the same time, rising competition in commercial lines is constraining premium growth and new business momentum.

Conclusion

While Selective Insurance remains well-positioned to gain from strong renewals, favorable E&S lines marketplace conditions and higher income earned on fixed-income securities portfolio, challenges facing the company, such as exposure to catastrophe losses, rising competition and social inflation, can drive earnings volatility.

SIGI should benefit from favorable growth estimates, higher ROE, optimistic analyst sentiment and prudent capital deployment. It is, therefore, wise to retain this Zacks Rank #3 (Hold) stock at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

W.R. Berkley Corporation (WRB): Free Stock Analysis Report

Axis Capital Holdings Limited (AXS): Free Stock Analysis Report

Selective Insurance Group, Inc. (SIGI): Free Stock Analysis Report

NMI Holdings Inc (NMIH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).