The rally in Micron (MU) stock has been nothing short of a dream run. In the last 52-weeks, MU stock has returned almost 800%. The most important point about this rally is that it’s not euphoria. It’s purely based on fundamental developments for the company and industry.

It’s therefore not surprising that analysts remain bullish on Micron's stock. With Q3 results on June 24, Needham has reiterated its “Buy” rating for MU stock and increased the price target to $1,550. At the core of this bullish thesis is continued strength in the memory market and limited capacity additions. Recently, Deutsche Bank also raised Micron stock’s price target to $1,500 with “AI-driven DRAM demand and pricing tailwinds” being the key factors.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Another point to note is that Micron has delivered earnings surprise on a continued basis in the last few quarters. Considering the demand and pricing trend, it’s likely that another blowout quarter is on the cards and will translate into MU stock trending higher.

About Micron Stock

Headquartered in Boise and commanding a market valuation of $1.3 trillion, Micron is a designer, developer, and manufacturer of memory and storage products. The company’s global product portfolio includes DRAM, NAND, NOR, solid-state drives, graphics and high bandwidth memory, managed NAND, and multichip packages.

Micron has four reportable business segments: Cloud Memory Business Unit, Core Data Center Business Unit, Mobile and Client Business Unit, and Automotive and Embedded Business Unit.

With structural artificial intelligence backed tailwinds, Micron has been on a robust growth trajectory. For Q2 FY26, the company’s revenue surged by 196% on a year-on-year (YoY) basis to $23.9 billion. At the same time, with favorable pricing, the company’s margins have expanded and Micron reported operating cash flow of $11.9 billion for the quarter. With stellar growth and swelling free cash flows, MU stock has skyrocketed by 292% in the last six months.

Although MU is feeling some selling pressure today (along with the rest of the tech world) before the earnings announcement and is down almost 11% in morning trading.

www.barchart.com

www.barchart.com High Capex Will Support Growth

There is no doubt on the point that the demand-supply mismatch is meaningful. To address this gap, Micron is investing more than $25 billion in capex for FY26. Further, Micron expects “2027 capex to step up meaningfully to support HBM- and DRAM-related investments.” These investments provide a clear path for sustained top-line growth. At the same time, Micron expects to “meaningfully increase” its R&D investment in 2027, which will support technology advancement.

From an innovation perspective, Micron has commenced manufacturing of 1α (1-alpha) DRAM. It’s the most advanced memory ever produced in the United States. Further, Micron's 1α node is considered as the most advanced DDR4 technology. With these innovation and continued investment in capex, Micron is well positioned to create value.

What Do Analysts Say About MU Stock?

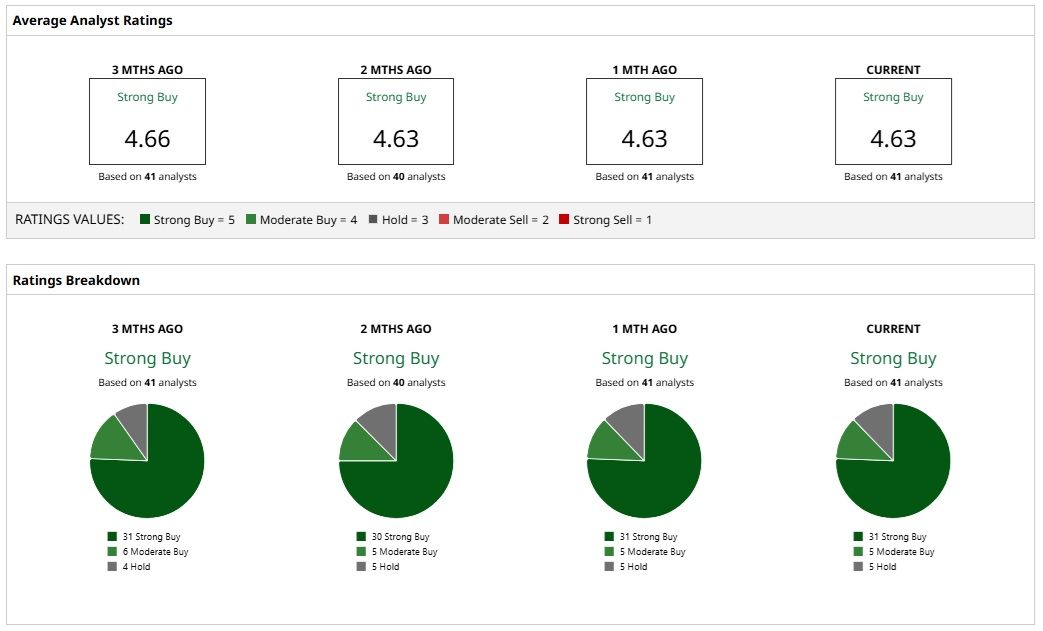

Based on 41 analysts with coverage, MU stock has a consensus “Strong Buy” rating. While 31 analysts have a “Strong Buy” rating for MU stock, five have a “Moderate Buy,” and five have a “Hold” rating.

The mean price target of $1,006.34 represents a potential downside of 7% from current levels. However, the most bullish price target of $1,750 suggests that MU could climb as much as 62% from here.

www.barchart.com

www.barchart.com Concluding Views

Any doubt that Micron is expensive can be cleared by the point that the stock trades at a forward price-earnings ratio of 18. With stellar earnings growth, the price-earnings-to-growth ratio is less than 1.

From a balance sheet perspective, Micron ended Q2 with a cash buffer of $20.2 billion. Further, with adjusted free cash flow for the quarter at $6.9 billion, there is ample scope for value creation through dividend growth and accelerated share repurchase.

At the same time, a portfolio of 60,000 patents underscores the company’s focus on innovation. With high financial flexibility, it’s likely that Micron will stay ahead of the curve in the memory and storage industry.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Amkor Technology Is a ‘Picks-and-Shovels’ Winner Up 327% as AI Chip Stocks Lead the Way Attractively Valued Micron Stock Seems Poised for Further Upside After Q3 Earnings Lululemon Shareholders Can Partly Blame Nike for LULU Stock’s Latest Bearish Price Surprise Wedbush Gives a Thumbs Up to Cerebras Ahead of Its First Quarterly Earnings. What This Means for CBRS Stock Investors.