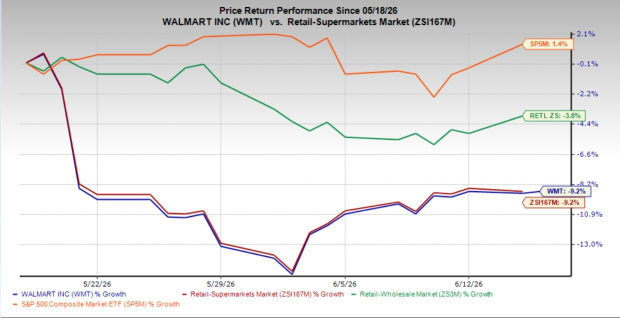

Walmart Inc. WMT shares have declined 9.2% over the past month, matching the industry's performance. However, the omnichannel retail giant has lagged the broader Zacks Retail - Wholesale sector's 3.8% decline and the S&P 500's 1.4% gain over the same period.

Meanwhile, Target Corporation TGT has rallied 8.1%, while other retailers like Costco Wholesale Corporation COST and The Kroger Co. KR have dipped 8.3% and 6.1%, respectively, over the past month.

The recent drop in WMT stock has raised questions about whether investors should view the pullback as a buying opportunity or remain cautious amid near-term macroeconomic uncertainties.

Image Source: Zacks Investment Research

Why Did Walmart Stock Decline?

Walmart’s recent pullback appears to be driven primarily by external pressures rather than company-specific execution issues. The company delivered solid first-quarter fiscal 2027 results and reaffirmed its full-year outlook, but investors are weighing the impact of a tougher cost and consumer backdrop.

A major concern is elevated fuel costs. In the first quarter, Walmart absorbed approximately $175 million in higher fuel expenses across its global distribution and fulfillment network, reducing operating income growth by roughly 250 basis points. Management also noted that if fuel costs remain elevated, retail price inflation could increase in the second quarter and the back half of the year.

Consumer behavior is another watchpoint. Walmart continues to benefit from strong traffic and market-share gains, but management noted that lower-income shoppers remain budget-conscious and are showing signs of financial pressure. Higher-income customers are spending more confidently, but weaker discretionary demand from value-seeking households could weigh on some categories.

Together, fuel-related cost pressure, consumer uncertainty and sector-wide weakness have weighed on shares despite the company’s solid fundamentals.

WMT’s Growth Drivers & Fundamental Strengths Remain Intact

Despite the recent stock decline, Walmart's underlying business remains on a solid footing. The company reported first-quarter revenue growth of 7.3%, while global e-commerce sales surged 26%. Walmart U.S. comparable sales increased 4.1%, driven by a 3% rise in transactions and continued market-share gains across key categories. Management noted that transaction growth in the United States was the strongest in six quarters, underscoring the strength of Walmart's value proposition.

The company's omnichannel model continues to be a key differentiator. Walmart is leveraging its extensive store network to deliver greater convenience and faster fulfillment. More than 36% of U.S. store-fulfilled deliveries were completed within three hours during the quarter, while the company can now reach roughly 60% of the U.S. population within 30 minutes. These capabilities are helping drive customer engagement and repeat purchases.

Higher-margin businesses are also becoming increasingly important contributors to growth. Walmart's global advertising business grew 37% in the first quarter, while membership fee revenues rose 17.4%. Walmart+ continued to add members at a healthy pace, supporting stronger customer loyalty and creating recurring revenue streams that complement the company's core retail operations.

Marketplace expansion remains another major growth opportunity. U.S. marketplace sales increased nearly 50% during the quarter as Walmart expanded assortment, attracted more sellers and improved fulfillment capabilities. The company's marketplace ecosystem is also driving greater advertising demand and strengthening the value proposition of Walmart Fulfillment Services.

Walmart continues to invest heavily in technology, automation and artificial intelligence. Its AI-powered shopping assistant, Sparky, is gaining traction with customers, while automation initiatives across fulfillment centers and distribution facilities are improving productivity and operating efficiency. Together, these initiatives position Walmart to enhance profitability while delivering a better customer experience over the long term.

Valuation Reflects Walmart's Premium Positioning

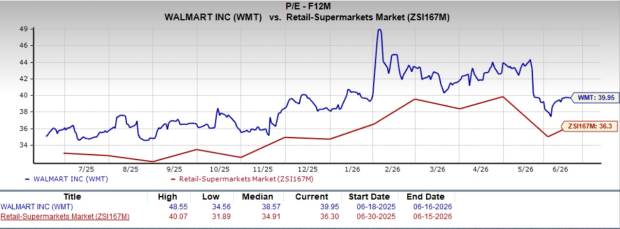

Walmart currently trades at a forward 12-month P/E multiple of 39.95, above the industry average of 36.3. While the stock commands a premium, the valuation reflects Walmart's strong competitive position, consistent market-share gains and growing portfolio of higher-margin businesses.

Image Source: Zacks Investment Research

The stock trades at a premium to Target and Kroger, which carry forward P/E multiples of 15.6 and 11.92, respectively, though it remains below Costco's 44.79. This positioning reflects investors' confidence in Walmart's resilient business model, market-share gains and long-term growth prospects.

WMT’s Estimate Revisions Signal Stability

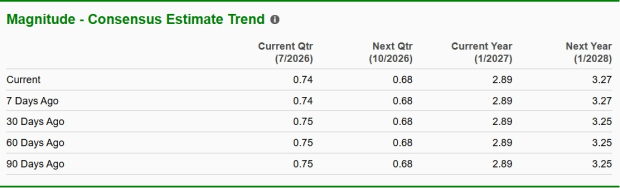

Analysts' earnings estimate revisions present a relatively balanced picture for Walmart. The Zacks Consensus Estimate for the current quarter has moved down by a penny over the past 30 days, reflecting some caution regarding near-term cost pressures and the broader consumer environment.

However, the consensus estimate for the current fiscal year has remained unchanged during the same period, indicating that analysts continue to view Walmart's earnings outlook as stable. The consensus estimate for the next fiscal year has increased by 2 cents over the past month, signaling confidence in the company's ability to sustain growth through its expanding higher-margin businesses, improving e-commerce economics and productivity initiatives.

Image Source: Zacks Investment Research

Should Investors Hold Walmart Stock?

Walmart's recent pullback reflects concerns about fuel costs, consumer spending pressures and broader market uncertainty rather than weakening fundamentals. The company continues to execute well across e-commerce, marketplace, advertising and membership initiatives while maintaining a stable earnings outlook. Although near-term headwinds warrant monitoring, Walmart's resilient business model, premium positioning and long-term growth prospects support its case as a core holding after the recent pullback. WMT currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Walmart Inc. (WMT): Free Stock Analysis Report

The Kroger Co. (KR): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).