Docusign, Inc. DOCU is benefiting from rising customer demand for eSignature. Its recurring subscription revenues, global presence and product expansion strategy boost long-term growth. Strong relationships with tech giants further support DOCU’s ecosystem.

Meanwhile, the pricing structure poses a significant concern for the company. Low liquidity further pressures profitability and scalability, while a non-dividend strategy makes the stock less attractive to investors.

How Is DOCU Faring?

Docusign continues to drive growth through strong customer demand for eSignature in a large addressable market. The company has consistently extended its customer base over the years, growing from 1.3 million in fiscal 2023, 1.5 million in fiscal 2024, 1.7 million in fiscal 2025 and 1.8 million in fiscal 2026. Despite this rising demand, the eSignature market remains largely untapped, giving DOCU significant opportunities to expand eSignature across businesses globally and boost its revenues.

DOCU’s total revenue mainly consists of fees generated through a strong subscription model, generally ranging from one to three years, which includes its product usage and access to customer support. This model helps the company expand the market by making expensive software more affordable and accessible to limited-resource companies. Numerous customer programs, initiatives and customer additions have steadily supported subscription revenue growth over time.

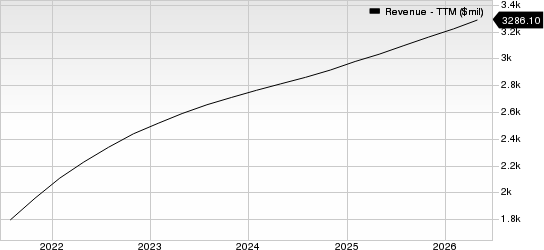

Docusign Inc. Revenue (TTM)

Docusign Inc. revenue-ttm | Docusign Inc. Quote

The company has witnessed rising international revenues over time, representing 26%, 28% and 29% of total revenues in fiscal 2024, 2025 and 2026, respectively. The company has experienced rising demand and is directing its sales and marketing efforts to tap this potential across multiple countries like Canada, the United Kingdom and Australia.

DOCU is focused on its growth strategy, which includes the expansion of its product use case into adjacent markets by managing and automating various agreement workflows across different business processes. The company continues investing in its Application Programming Interfaces (APIs) and other forms of support to further drive its value creation cycle between developers and itself.

DOCU pursues growth with strategic investments and partnerships. Its expanded relationships with tech giants such as Salesforce CRM and Microsoft MSFT have significantly boosted the company’s overall growth. DOCU and Salesforce are jointly developing solutions to automate the contract creation process and enhance collaboration among organizations that use Salesforce’s Slack. Recently, Docusign integrated eSignature with Microsoft Teams and became an official electronic signature provider in Microsoft Teams’ Approvals app. This will enable DOCU to sell products to a far greater number of client accounts.

Meanwhile, Docusign’s pricing structure is at risk from competitive pressure. New competitors’ products and aggressive pricing could limit DOCU's ability to attract and retain customers using its traditional pricing model. Companies may demand price discounts as part of sales contract negotiations, which will affect the business, operating results and financial position of the company.

The company’s current ratio (a measure of liquidity) at the end of the fourth quarter of 2026 was 0.73, lower than the industry average of 1.92. A current ratio of less than 1 often indicates that the company may not be well-positioned to pay off its short-term obligations.

DOCU does not offer dividends, making share price appreciation the primary source of returns for its shareholders. This makes the stock less attractive to investors seeking cash dividend returns.

Docusign currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Salesforce, Inc. (CRM): Free Stock Analysis Report

Docusign Inc. (DOCU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).