The quick-service restaurant industry continues to navigate a challenging consumer environment, with value offerings, digital engagement and international expansion playing increasingly important roles in driving growth.

Against this backdrop, both McDonald's Corporation MCD and Yum! Brands, Inc. YUM remains the sector's most influential players, backed by globally recognized brands and predominantly franchised business models. While McDonald's leverages its unmatched scale, operational efficiency and strong value proposition, Yum! Brands is capitalizing on the expansion of KFC and Taco Bell while accelerating digital innovation and AI-driven capabilities. With both companies pursuing distinct growth strategies, investors may be wondering which restaurant stock offers the stronger long-term opportunity.

The Case for MCD

McDonald's continues to demonstrate the resilience of its business model despite a challenging consumer environment. In the first quarter of 2026, the company posted 3.8% global comparable sales growth and gained market share in nearly all of its top 10 markets. Management attributed the performance to its focus on value offerings, impactful marketing campaigns and menu innovation, reinforcing the effectiveness of the "three-for-three" strategy.

The company is also well-positioned for long-term growth through its global scale and digital initiatives. McDonald's is rolling out new beverage platforms across key markets, expanding its value menu in the United States and remains on track to open about 1,000 restaurants in China this year while reaffirming the broader 2026 financial targets. These initiatives should support customer traffic and strengthen its competitive position.

However, McDonald's continues to face several headwinds. Management acknowledged that the macroeconomic backdrop remains difficult, with lower-income consumers still under pressure from inflation and elevated fuel prices. The company also expects second-quarter comparable sales growth to slow due to difficult comparisons and an uncertain demand environment.

Profitability also remains an area of concern. McDonald's admitted that margins at its U.S. company-operated restaurants were below expectations, while franchisees continue to grapple with higher labor, commodity and supply-chain costs. Rising construction expenses could also affect future restaurant development if projected returns become less attractive.

The Case for YUM

Yum! Brands delivered another solid quarter, driven by broad-based growth across its core businesses. System sales increased 6%, global same-store sales rose 3% and the company opened more than 1,000 new restaurants during the quarter. Strong contributions from KFC and Taco Bell, coupled with disciplined cost management, fueled double-digit core operating profit growth.

Taco Bell remains Yum! Brands' biggest growth engine. The brand posted strong U.S. same-store sales growth, outperforming the broader quick-service restaurant industry for the eighth straight quarter. Management credited the performance to its value platform, menu innovation, digital engagement and operational improvements, while also raising the full-year restaurant margin outlook.

Yum! Brands is also strengthening its long-term competitive position through technology and global expansion. Digital sales approached $11 billion during the quarter, with the digital mix reaching a record 63%. The company continues to expand the Byte technology platform, deploy AI-powered tools across its brands and accelerate restaurant development at KFC and Taco Bell, creating multiple avenues for sustained growth.

On the downside, Yum! Brands still face external risks. Geopolitical tensions in certain international markets and persistent inflationary pressures could weigh on consumer demand and restaurant development in some regions. While management expects only a limited impact, these factors remain worth monitoring.

How Does the Zacks Consensus Estimate Compare for MCD & YUM?

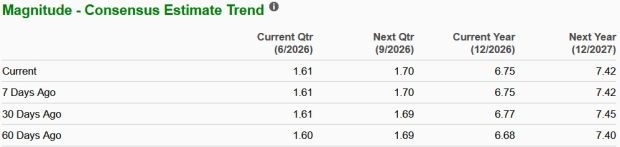

The Zacks Consensus Estimate for McDonald’s 2026 sales and EPS implies year-over-year growth of 5.7% and 6%, respectively. Earnings estimates for 2026 have witnessed downward revisions of 2.1% in the past 60 days.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Yum! Brands’ 2026 sales and EPS indicates a year-over-year increase of 11% and 11.6%, respectively. Earnings estimates for 2026 have witnessed upward revisions of 1% in the past 30 days.

Image Source: Zacks Investment Research

Price Performance & Valuation

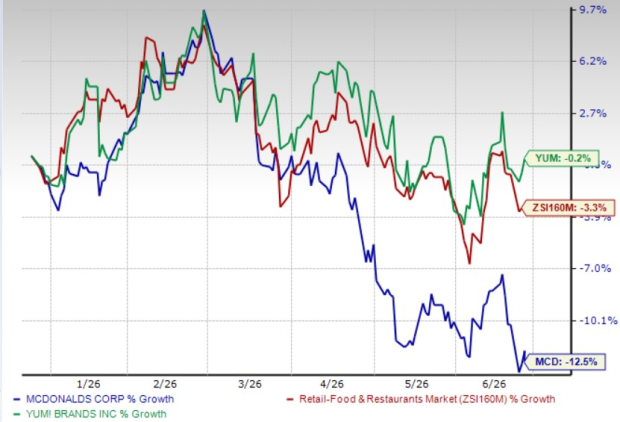

MCD stock has lost 12.5% in the past six months, compared with the industry's 3.3% decrease. Conversely, YUM’s shares have declined 0.2% in the same time frame.

Price Performance

Image Source: Zacks Investment Research

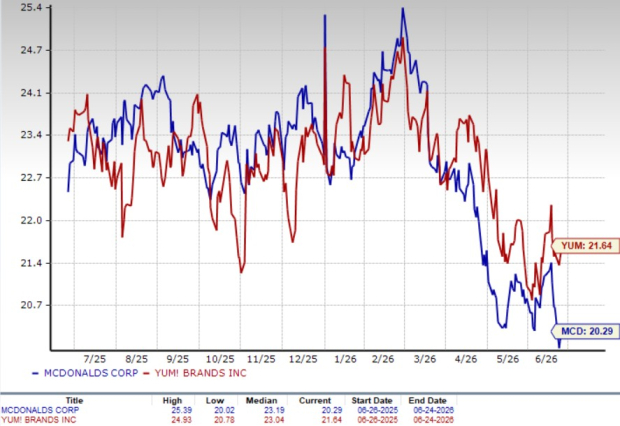

MCD is trading at a forward 12-month price-to-earnings ratio of 20.29X, below its median of 23.19X over the last year. YUM’s forward earnings multiple is 21.64X, below its median of 23.04X over the same time frame.

P/E (F12M)

Image Source: Zacks Investment Research

Wrapping Up

While both companies trade below their historical valuation averages, Yum! Brands appears better positioned for growth. The company is benefiting from stronger earnings and revenue expectations, improving analyst sentiment and sustained momentum at Taco Bell, supported by international expansion and digital innovation.

In contrast, McDonald's is facing softer earnings estimate revisions, pressure on company-operated restaurant margins and a more challenging consumer backdrop. Yum! Brands also continues to streamline its portfolio following the announced divestiture of Pizza Hut, allowing management to sharpen focus on the faster-growing KFC and Taco Bell businesses.

Yum! Brands currently carries a Zacks Rank #3 (Hold), while McDonald's has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

McDonald's Corporation (MCD): Free Stock Analysis Report

Yum! Brands, Inc. (YUM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).