Culp, Inc. CULP used its fourth-quarter earnings call to argue that two years of restructuring are beginning to show up in the numbers. Management’s central message was not that the turnaround is finished, but that revenue momentum, lower costs and a leaner platform have started to improve operating leverage.

That matters because the company is heading into fiscal 2027 with limited formal guidance, a still-weak home furnishings market and a balance sheet that it is trying to stabilize. The call focused on what Culp believes it can control: mix, pricing, efficiency, inventory and debt reduction.

CULP Sets the Turnaround Frame

President and CEO Iv Culp said the fourth quarter showed building momentum as the company exited fiscal 2026. He pointed to sequential gains in sales, gross profit, operating results and the bottom line as evidence that restructuring and integration efforts are starting to translate into better performance.

Revenues rose 5.8% year over year to $51.6 million, exceeding the Zacks Consensus Estimate of $50.1 million by 3%. The company posted a net loss of $2.2 million or 17 cents, missing the consensus mark by 54.6%.

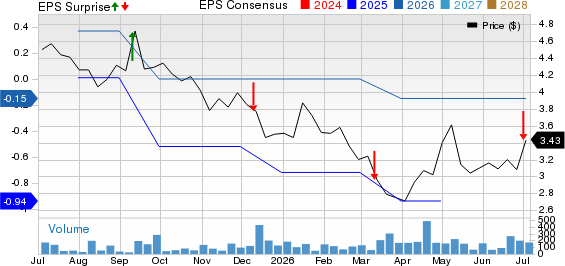

Culp, Inc. Price, Consensus and EPS Surprise

Culp, Inc. price-consensus-eps-surprise-chart | Culp, Inc. Quote

Management also kept the tone measured. Iv Culp said there is still meaningful ground to cover before the company reaches the profitability level it expects, even as he described fiscal 2027 as a potential turning point.

Culp Leans on Bedding for Growth

Bedding was the clearest source of momentum on the call. Fourth-quarter bedding sales rose 12.5% year over year to $30.5 million, and management said share gains, new product innovation and stronger sewn mattress cover execution drove the improvement.

Iv Culp spent considerable time describing sewn covers as a way to raise the company’s value per mattress unit. He said broader cover offerings and improved offshore and nearshore manufacturing execution are helping Culp deepen relationships with targeted customers.

Gross profit in bedding climbed 38% sequentially from the third quarter, although margin remained below the prior-year level. Management attributed the quarter-over-quarter gain to higher sales and improved operating efficiency, while noting that year-over-year comparisons were distorted by last year’s inventory valuation policy change.

CULP Keeps Working Through Upholstery

Upholstery remained the more pressured business. Fourth-quarter sales declined 2.5% year over year to $21.1 million, with management attributing the softer demand backdrop to trends in housing activity, consumer spending, and travel and leisure, which are affecting residential and hospitality furniture.

Even so, executives emphasized the importance of sequential progress. Iv Culp said the business posted quarter-to-quarter revenue growth and margin improvement, helped by lower fixed costs and the continued integration of domestic upholstery operations into the bedding footprint in North Carolina.

Management also highlighted a reduced facility footprint in China and added capabilities in Vietnam, including a new showroom. The message was that upholstery remains demand-constrained but is structurally better positioned to recover more profitably when furniture markets improve.

Culp’s Balance Sheet Gets a Tariff Boost

Chief financial officer Kenneth Bowling made inventory and debt central to the call. Inventory ended the quarter at $47.5 million, down about $5 million from the third quarter, which management framed as evidence that tighter controls are beginning to free up cash.

Liquidity at year-end stood at $24.2 million, including $8.3 million in cash, while outstanding debt totaled $19.1 million. Net debt was about $10.9 million, and Bowling said the borrowings were primarily used to fund working capital and restructuring actions.

The biggest near-term swing factor was the roughly $7 million of IEEPA tariff refunds received in the first quarter of fiscal 2027. Management said that cash should cut net debt to about $5 million at first-quarter end, improve liquidity and help offset elevated tariff-related costs absorbed in fiscal 2026.

CULP Offers Limited but Clearer Outlook

Formal guidance was narrow, but the direction of travel was clearer. Management said first-quarter fiscal 2027 sales should improve moderately both sequentially and from the prior-year period, even as home furnishings demand remains challenged.

Culp also said cost and efficiency gains from restructuring should produce breakeven to positive adjusted EBITDA in the first quarter without any benefit from the tariff refunds. With the refunds included, management expects profitability to improve further.

In Q&A, a Water Tower Research analyst pressed management on product mix, margins and cost savings. Iv Culp responded that bedding should continue to outgrow upholstery in the near term, bedding margins should improve in fiscal 2027 and the company still has room for additional cost or pricing actions if demand does not recover as hoped.

Culp Leaves Investors With a Disciplined Tone

The call ended with management emphasizing discipline over optimism. Iv Culp repeatedly returned to the need to manage what it can control: costs, pricing, inventory, supply chain flexibility and debt.

That tone was reinforced in Q&A when Bowling said the company will prioritize paying down higher-cost U.S. debt first while potentially keeping some low-cost China borrowings in place for strategic flexibility.

The overall posture takeaways from the call were that Culp sees the platform reset as largely complete but still needs a steadier demand backdrop and continued execution to convert those structural changes into sustained profitability.

Zacks Signals Remain Cautious

CULP carries a Zacks Rank #3 (Hold), along with Value, Growth and Momentum Scores of D each and a VGM Score of F. Under the Zacks framework, the rank is the primary signal, while Style Scores are meant to refine stock selection, with A and B grades indicating stronger characteristics and D or F indicating weaker near-term appeal. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

A Zacks Rank #3 does not carry the same favorable implication as a Zacks Rank #1 or 2 (Buy), and weak Style Scores further temper the setup. The Zacks view can also change after earnings, as analyst estimate revisions are updated, so the current rank and scores should be viewed as a snapshot rather than a fixed verdict.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Culp, Inc. (CULP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).