CrowdStrike Holdings CRWD is currently trading at a high price-to-sales (P/S) multiple, far above the Zacks Security industry. CrowdStrike’s forward 12-month P/S ratio sits at 30.45X, significantly higher than the Zacks Security industry’s forward 12-month P/S ratio of 15.98X. The Zacks Value Score of F also suggests that CRWD stock is overvalued.

Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

CRWD stock also trades at a higher P/S multiple compared with other industry peers, including Qualys Inc. QLYS, Okta OKTA and SentinelOne S. At present, Qualys, Okta and SentinelOne have P/S multiples of 6.94X, 7.39X and 4.65X, respectively.

While this elevated valuation reflects investor confidence in the company’s long-term potential, it also raises concerns about whether the stock can justify such lofty multiples, especially amid near-term challenges.

CrowdStrike Encounters Slowing Sales Growth

Although CrowdStrike has experienced impressive growth since its IPO, recent quarterly reports have shown a deceleration in its growth rate. The company's revenue growth, while still robust, is not as explosive as in previous years.

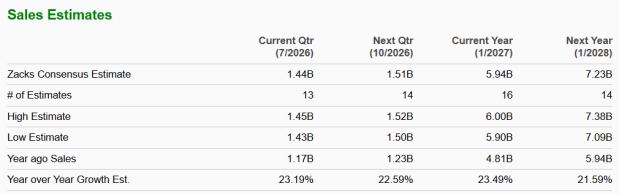

CrowdStrike had enjoyed more than 35% year-over-year top-line growth till fiscal 2024. However, the growth rate decelerated to 29% in fiscal 2025 and further decelerated to 22% in fiscal 2026.

For fiscal 2027, CrowdStrike expects total revenues to be in the range of $5.915 billion to $5.959 billion, indicating a year-over-year increase of 23% to 24%. While the Zacks Consensus Estimate for fiscal 2027 revenues indicates a year-over-year increase of 23.5%, the same for fiscal 2028 suggests that the top-line growth will further decelerate to around 21.6%. This indicates that the deceleration in CrowdStrike's revenue growth is likely to continue in the upcoming years.

Image Source: Zacks Investment Research

Despite near-term concerns, the growing adoption of the Falcon Flex subscription model is anticipated to boost CrowdStrike's prospects in the coming quarters.

Falcon Flex Adoption Aids CrowdStrike’s Subscription Gains

CrowdStrike’s subscription business model is driving its overall top-line performance. The company’s revenues crossed the $1 billion mark for the seventh consecutive time during the first quarter of fiscal 2027 and marked a year-over-year improvement of nearly 26%. This was partly achieved due to the strong adoption of the Falcon Flex Subscription Model, which allows customers to commit upfront and later choose modules, eliminating procurement friction.

CrowdStrike’s subscription customers, who adopted six or more cloud modules, represented 51% of the total subscription customers at the end of the second quarter. Those with seven or more cloud modules accounted for 35%, and those with eight or more cloud modules represented 25% as of April 30, 2026. In the first quarter, Annual Recurring Revenues (ARR) from Falcon Flex customers were more than $1.9 billion, rising 99% on a year-over-year basis. Management said Falcon Flex is now one of the most common ways customers choose to buy and expand on the Falcon platform.

Falcon Flex helps customers adopt new modules without long contract steps, which leads to faster platform usage. This is also driving strong re-Flex activity, where more than 380 customers expanded their Flex contracts in the fourth quarter. In the first quarter of fiscal 2027, CrowdStrike added more than 300 Flex customers and ended the first quarter with over 1,900 customers who have adopted Falcon Flex.

Falcon Flex helps customers adopt new modules without long contract steps, which leads to faster platform usage. The model is helping CrowdStrike benefit from platform consolidation. Customers are using Flex to adopt additional offerings such as Next-Gen SIEM, Identity Protection, Cloud Security and AI Detection and Response without negotiating separate contracts. If these patterns continue, Falcon Flex could remain one of CrowdStrike’s most important growth drivers through fiscal 2027 and beyond.

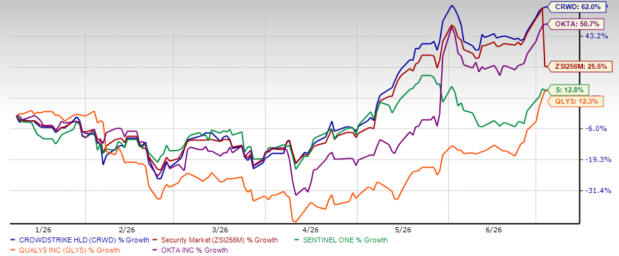

These factors seem to have instilled investors’ confidence in CRWD’s prospects, as reflected in a rise in share price over the past six months. CRWD stock has surged 62% over the past six months, outperforming the industry’s return of 25.5%. The stock has outperformed its industry peers as well, such as Qualys, Okta and SentinelOne. Over the past six months, shares of Qualys, Okta and SentinelOne have returned 12.3%, 50.7% and 12.8%, respectively.

6-Month Price Return Performance

Image Source: Zacks Investment Research

Key Technical Indicator Signals Bullish Trend for CRWD

CRWD shares are trading above their 50-day & 200-day moving averages, a bullish technical signal that indicates the potential for continued upward momentum in the near term.

CRWD’s 50-Day & 200-Day Simple Moving Averages

Image Source: Zacks Investment Research

Conclusion: Hold CrowdStrike Stock Right Now

As businesses continue prioritizing AI-driven cybersecurity solutions, CrowdStrike’s leadership in threat prevention, response and recovery will only strengthen. The company’s subscription-based model and recurring revenue streams should provide stability and gradual growth, even amid ongoing macroeconomic challenges and geopolitical issues.

However, the company’s premium valuation and slowing sales growth warrant a cautious approach to the stock. CrowdStrike currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CrowdStrike (CRWD): Free Stock Analysis Report

SentinelOne, Inc. (S): Free Stock Analysis Report

Qualys, Inc. (QLYS): Free Stock Analysis Report

Okta, Inc. (OKTA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).