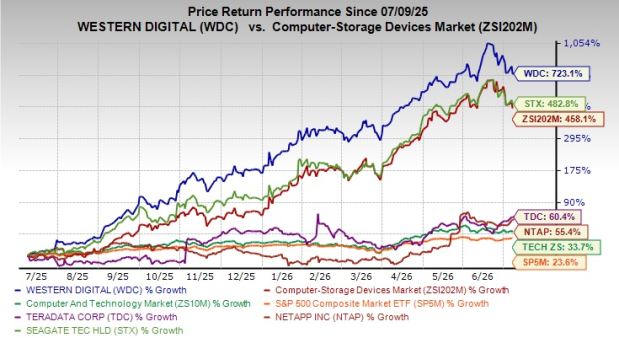

Western Digital Corporation WDC has been a standout performer in the storage industry over the past year. Its shares have skyrocketed 723.1% over the past year, outpacing the 458.1% growth of the Zacks Computer-Storage Devices industry. The stock has also outperformed the Zacks Computer & Technology sector’s and the S&P 500’s growth of 33.7% and 23.6%, respectively. After enduring a prolonged downturn caused by weak PC demand and excess memory inventory, the company has benefited from a recovery in storage pricing, growing enterprise demand and the accelerating adoption of AI.

Image Source: Zacks Investment Research

Western Digital competes against several major players in both HDD and flash storage markets, such as Seagate Technology Holdings plc STX, NetApp, Inc. NTAP and Teradata TDC. STX, TDC and NTAP have gained 482.8%, 60.4% and 55.4%, respectively, in the same time frame.

WDC boasts a 52-week high of $799.87. With WDC outperforming many peers over the last 12 months, investors wonder whether there is still upside potential or whether most of the gains have already been priced in.

Here's a closer look.

Industry Tailwinds Continue to Favor WDC Stock

Several broader trends continue supporting long-term storage demand, such as the AI boom, healthy cloud spending, rising enterprise digital transformation and improving operational efficiency. Driven by rising demand for AI-related storage, WD is strengthening its capacity leadership through continuous innovation. The company is advancing 44TB HAMR and 40TB ePMR high-capacity drives in qualification, with volume production expected in the second half of 2026 and a roadmap extending beyond 100TB.

It is also expanding adoption of its UltraSMR technology, now used by three major customers and supporting nearly all exabyte demand. In addition, WD is introducing high-bandwidth drives and dual-pivot technology to optimize AI workloads, while long-term customer agreements extending through 2028 and 2029 provide greater revenue visibility. AI workloads, agentic AI, synthetic data and physical AI are driving strong demand for HDD storage, with long-term exabyte growth projected to exceed 25% CAGR. As AI-generated data continues to expand, HDDs remain the preferred solution for long-term data retention in hyperscale data centers, complementing flash storage, which is optimized for high-speed performance.

Western Digital is also benefiting from higher pricing, a favorable product mix and cost efficiencies. It expects pricing momentum to continue into late 2026, while improvements in areal density, UltraSMR adoption and supply chain efficiencies are lowering costs and supporting margin expansion without requiring additional manufacturing capacity. The UltraSMR JBOD platform aims to broaden market reach, especially into Tier 2 CSPs and some hyperscalers in Asia. By the end of calendar 2027, most key customers will be on UltraSMR, either fully adopted or in qualification. The forecast indicates that close to 60% of exabytes shipped will be on UltraSMR by the end of fiscal 2027. Expansion into Tier 2 CSPs and hyperscalers is a key strategy.

The company is also considering investments in head and media capacity to support multiyear customer commitments, focusing on technological improvements rather than unit capacity. No new unit capacity investments are planned. The focus is on increasing capacity per drive through technology, such as higher aerial density and more platters. There is potential to increase capacity from 14 disks over time if it proves to be economically viable.

Spin-Off Creates New Opportunities for WDC

Western Digital has been restructuring its business by separating its flash memory operations into Sandisk SNDK from its HDD business. Investors often reward companies that simplify their business models, allowing each segment to pursue strategies tailored to its specific market. During the fiscal third quarter, WDC strengthened its balance sheet by selling 5.8 million SanDisk shares and using the proceeds to reduce debt by $3.1 billion, leaving only $1.6 billion in convertible debt.

Image Source: Zacks Investment Research

The company also ended the quarter with a net cash position of $450 million and expanded its capital return program by authorizing an additional $4 billion in share repurchases. Strong free cash flow continues to support WesternDigital's shareholder return strategy. The company increased its quarterly dividend by 20%, and has returned $2.2 billion to shareholders through dividends and share repurchases since the fourth quarter of 2025. Supported by a net cash position, management remains focused on returning excess free cash flow through ongoing buybacks and dividends.

Despite the positive outlook, Western Digital remains far from risk-free. The storage industry remains highly cyclical, with supply-demand imbalances capable of quickly pressuring pricing, margins and profitability. The company also faces intense competition, while any slowdown in AI investment or broader macroeconomic weakness could reduce demand for storage infrastructure.

Upbeat Estimate Revision Trend for WDC

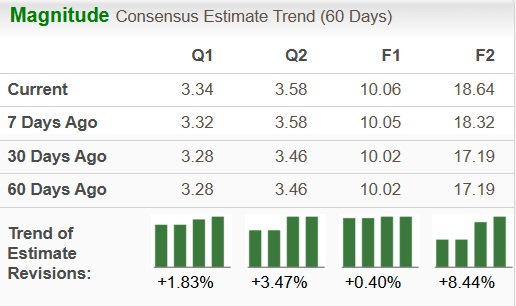

WDC’s estimate revisions are on an upward trajectory currently. The Zacks Consensus Estimate for WDC’s earnings for fiscal 2026 has been revised north by 0.4% to $10.06 over the past 60 days, while the same for fiscal 2027 has gone up 8.4% to $18.64.

Image Source: Zacks Investment Research

Valuation Considerations

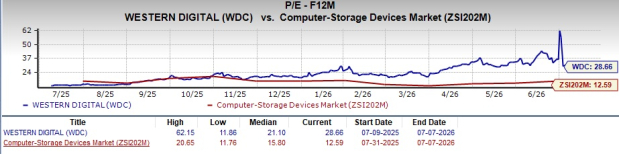

Several factors could support continued appreciation, including rising enterprise demand, a better pricing environment, improving margins, the expansion of AI infrastructure and benefits from corporate restructuring. Going by the price/earnings ratio, the company’s shares currently trade at 28.66 forward earnings compared with 12.59 for the industry.

Image Source: Zacks Investment Research

In comparison, the forward 12-month price/earnings multiple for STX, TDC and NTAP are 29.51X, 19.71X and 22.67X, respectively.

Should You Consider Buying WDC Stock Now?

Western Digital’s improving fundamentals, recovering storage markets, better profitability and growing exposure to AI-driven infrastructure spending drove its strong performance. Its long-term prospects remain encouraging as cloud computing, AI and exploding global data creation continue boosting storage demand. The company's strategic restructuring could unlock further shareholder value over time. However, short-term volatility, pricing swings and macroeconomic uncertainty could create periods of weakness even if the long-term trajectory remains intact.

For long-term investors who can tolerate industry cycles, WDC still appears to offer an attractive way to participate in the growing demand for enterprise storage and AI infrastructure. While last year's outsized gains may be hard to repeat, continued execution and favorable industry trends could still support further upside.

Flaunting a Zacks Rank #1 (Strong Buy), WDC is an appealing portfolio pick at the moment. You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Western Digital Corporation (WDC): Free Stock Analysis Report

NetApp, Inc. (NTAP): Free Stock Analysis Report

Seagate Technology Holdings PLC (STX): Free Stock Analysis Report

Sandisk Corporation (SNDK): Free Stock Analysis Report

Teradata Corporation (TDC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).