Zeta Global Holdings Corp. ZETA offers a useful lens on how enterprise marketing platforms are changing in 2026.

The company is riding AI-driven customer intelligence, vendor consolidation and agency workflow expansion. The same shift is creating margin and cash-timing friction, complicating the growth narrative.

How ZETA Reflects AI Platform Demand

Zeta’s recent results point to rising demand for AI-native marketing platforms. First-quarter 2026 revenues grew 50% year over year as enterprises used the Zeta Marketing Platform across email, connected TV, mobile and social channels.

Athena is central to that trend. The product reached general availability for all enterprise customers in the first quarter, and agentic interactions increased more than sevenfold in the first week.

Those interactions accounted for more than 60% of AI usage. Multi-use-case customers increased more than 50%, while customers using more than three channels rose roughly 40%.

Why Zeta Benefits From Vendor Consolidation

Zeta is benefiting as enterprises standardize on fewer platforms that can deliver measurable outcomes. Its sales pipeline expanded roughly 40% year over year in the first quarter, and nine of the top 10 industries grew more than 20%.

Direct platform revenue mix held at 75%, aligning with the company’s 70-75% target. That mix gives Zeta more control than third-party integrated channels.

Cross-sell adds to the theme. Marigold integration is creating opportunities to bundle loyalty with Zeta’s acquire and grow use cases. The Trade Desk TTD, a demand-side platform used by advertisers and agencies, is tied to automated media buying. LiveRamp Holdings, Inc. RAMP, with its data collaboration platform, sits in a related area where identity, data access and measurement remain important.

Where ZETA Exposes Agency Model Friction

The agency opportunity is not immediately margin friendly. New agency wins have often ramped through social channels first, and that mix lifted GAAP cost of revenue to 41% in the first quarter of 2026.

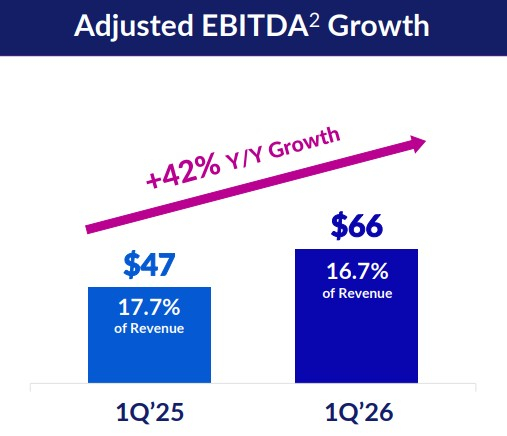

Adjusted EBITDA margin was 16.7%, down 100 basis points year over year, even though adjusted EBITDA increased 42%. Management expects social-led agency activity to become accretive to adjusted EBITDA and free cash flow over time, but early onboarding can dilute margins.

Cash timing also reflects the agency model. Free cash flow conversion reached 63% in the first quarter, but longer agency payment cycles created a roughly 13-point headwind.

How Zeta Tracks Open Data and Integration Needs

Zeta’s recent strategic updates point to another marketing technology trend: enterprises want connected data layers and lower integration friction. Its partnership with Palantir will rearchitect Zeta’s Data Cloud on Palantir Foundry and link operational intelligence, customer intelligence and marketing execution.

Zeta also joined the Snowflake-led Open Semantic Interchange initiative. The effort is designed to support vendor-neutral semantic model standards, helping data and insights work across AI and analytics tools.

These moves fit a market where interoperability can influence adoption. For large enterprises, AI-enabled marketing workflows are more useful when they connect with existing data, analytics and governance systems.

What ZETA Signals Say About the Trend

Bottom line, Zeta reflects powerful shifts in marketing technology, but the stock still has to prove that growth can translate into cleaner earnings momentum. AI adoption, vendor consolidation and interoperability support the business, while agency mix, discretionary spending exposure and synergy timing keep the setup balanced.

ZETA currently carries a Zacks Rank #4 (Sell), which points to caution over the next one to three months because the Rank is driven by earnings estimate revision trends. That signal matters when a company’s story depends on a second-half margin ramp and steady execution.

The Style Scores are mixed. ZETA has a Growth Score of A, a Momentum Score of F and a VGM Score of B. The Growth and VGM readings suggest the company still screens well on business expansion and balanced style traits, but the weak Momentum Score and Zacks Rank #4 show that thematic strength alone is not enough. The trend looks compelling, but the stock needs cleaner execution to confirm it.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zeta Global Holdings Corp. (ZETA): Free Stock Analysis Report

The Trade Desk (TTD): Free Stock Analysis Report

LiveRamp Holdings, Inc. (RAMP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).