H.B. Fuller Company FUL gives investors a focused way to track changing demand in specialty materials. The company is not relying on one end market or one margin lever.

Its current setup rests on three connected trends: deeper exposure to regulated medical markets, solid demand in aerospace and electronics and pricing actions aimed at offsetting inflation and supply disruptions.

H.B. Fuller Pushes Deeper Into Medical

Medical is becoming a more important part of H.B. Fuller’s portfolio. The proposed acquisition of Advanced Medical Solutions would expand the company into tissue bonding adhesives, surgical tapes, dressings and biosurgical products.

The deal is expected to increase H.B. Fuller’s total addressable market by $15 billion to $95 billion. It also supports the company’s goal of reaching an adjusted EBITDA margin of more than 20% by 2028.

This matters because medical demand tends to be more procedure-driven and regulated than many industrial or consumer applications. That can make the business mix less tied to short-cycle demand swings.

3M Company MMM remains a relevant comparison for investors watching materials innovation across healthcare, electronics and industrial applications. Its breadth shows why higher-specification materials businesses often attract attention when customers need reliability and regulatory know-how.

H. B. Fuller Company Price and Consensus

H. B. Fuller Company price-consensus-chart | H. B. Fuller Company Quote

FUL Benefits From Aerospace and Electronics

FUL’s growth is not coming from medical alone. In Engineering Adhesives, organic growth was roughly 5% excluding the exit from the lower-margin solar business.

Aerospace was up 30%, while electronics and general industries posted double-digit gains. Those areas are helping offset softness in automotive, where demand remained weaker across regions.

These trends point to the value of higher-performance niches. FUL’s adhesives are tied to applications where reliability, qualification and technical service matter.

Avery Dennison Corporation AVY is another materials name investors may watch when tracking specialty materials demand. Like FUL, it gives investors exposure to markets where product performance and customer-specific solutions can shape growth.

H.B. Fuller Navigates an Inflation Era

Pricing remains central to the FUL story. In the second quarter of fiscal 2026, pricing increased net revenues by 3% and more than offset slightly lower volume.

Adjusted gross margin rose 200 basis points to 34.2%, helped by pricing execution and restructuring savings. Adjusted EBITDA increased 9% to $181 million, with adjusted EBITDA margin improving to 19.1%.

The operating backdrop remains unsettled. Nearly 90% of raw materials were higher in the fiscal second quarter versus the first quarter, and more than 50 force majeure events remained in place.

Management expects high-single-digit pricing in the second half. That gives FUL a margin-defense lever, but it also shows that input-cost pressure has not fully eased.

Why FUL Still Needs Better Volume Trends

The trend story is not a clean cyclical rebound. Volume weakness remains a constraint, especially in more consumer-linked parts of the portfolio.

Flexible packaging stayed soft, and automotive declined by mid-single digits. Management’s fiscal 2026 framework also includes low- to mid-single-digit volume declines in the second half.

That keeps the investment case tied to mix improvement, pricing and restructuring rather than broad volume recovery. FUL can still improve margins, but stronger demand would make the growth profile more balanced.

The solar exit also creates noise in Engineering Adhesives comparisons. As that headwind laps, healthier niches may become easier to see, but the company still needs better volume confirmation.

FUL Screens Well for This Trend Setup

The bottom line is that FUL is participating in attractive specialty materials trends, but the stock still needs a firmer volume backdrop to turn margin resilience into a more decisive growth story.

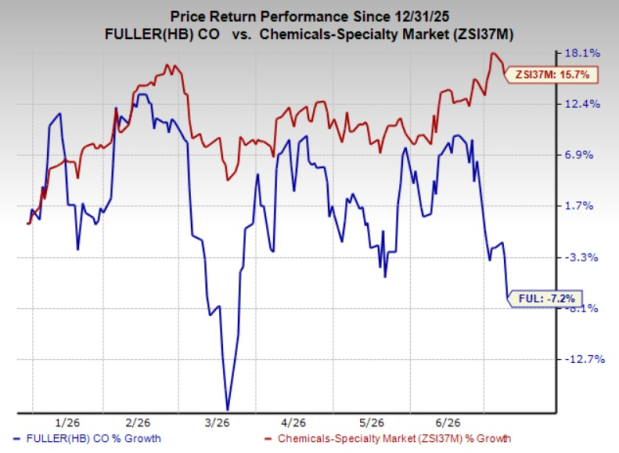

Shares of FUL have lost 7.2% so far this year against the industry’s 15.7% rise.

Image Source: Zacks Investment Research

FUL currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stock also has a VGM Score of A, supported by a Value Score of A and Momentum Score of A. Those scores suggest the stock screens well for investors who focus on valuation and earnings-related momentum. The Growth Score of C keeps the signal more balanced, fitting a company with improving mix and pricing power but uneven end-market demand.

The setup is constructive, not risk-free. FUL’s medical expansion, aerospace and electronics exposure, and pricing execution give the stock useful support, while consumer softness, automotive pressure and input-cost volatility remain key areas to watch.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

H. B. Fuller Company (FUL): Free Stock Analysis Report

3M Company (MMM): Free Stock Analysis Report

Avery Dennison Corporation (AVY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).