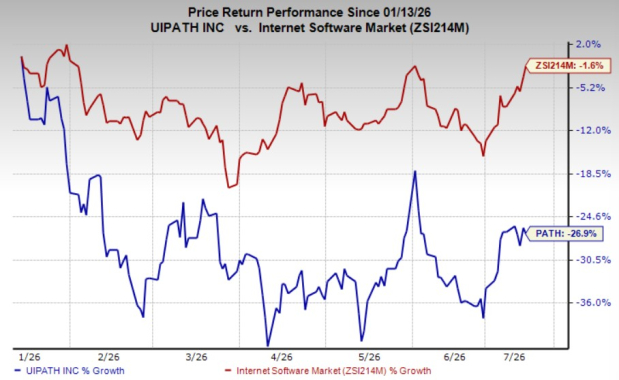

UiPath PATH has experienced a sharp share price correction over the past six months, declining 27% compared with the industry’s 2% decline.

While concerns over AI competition and cautious enterprise spending have weighed on the stock, the company continues to strengthen its financial performance, expand its automation platform and deepen customer adoption. With a more reasonable valuation and growing traction in agentic AI, UiPath appears well-positioned to benefit from the next phase of enterprise automation.

PATH’s Agentic AI Adoption Continues to Accelerate

One of the most encouraging developments for UiPath is the increasing adoption of its agentic AI platform. Roughly one year after making its agentic products generally available, the company is seeing customers move beyond pilot programs into full production deployments.

This transition is significant because production deployments typically indicate that customers are realizing measurable business value and integrating AI capabilities into mission-critical workflows rather than simply experimenting with new technology.

UiPath's role extends beyond simply providing AI agents. Its platform serves as an orchestration layer that coordinates workflows, automates execution and integrates AI-generated outputs directly into enterprise operations. As organizations increasingly deploy AI agents, this orchestration capability becomes increasingly valuable.

The recent introduction of UiPath for Coding Agents further strengthens the company's AI strategy by helping customers accelerate deployments and achieve faster time to value, potentially driving broader platform adoption across enterprise customers.

Maestro Case Broadens PATH’s Enterprise Platform

UiPath recently expanded its automation portfolio with the launch of Maestro Case, a capability designed to help enterprises manage complex, long-running workflows involving multiple participants, business systems and AI agents.

Many organizations still rely on fragmented processes involving emails, spreadsheets, and disconnected software to manage customer requests, approvals, and investigations. Maestro Case addresses these inefficiencies by treating every business case as an evolving workflow while combining automation with human oversight.

The launch appears to expand UiPath's competitive positioning against ServiceNow NOW and Pegasystems PEGA. While ServiceNow has built a strong franchise in enterprise workflow management and Pegasystems has long specialized in case management and business process automation, UiPath aims to differentiate itself by integrating robotic process automation, workflow orchestration, and agentic AI within a unified platform. As enterprises increasingly seek AI-enabled workflow solutions, PATH's broader automation capabilities could provide a meaningful competitive advantage over Pegasystems and ServiceNow.

Large Customer Growth Supports Long-Term Outlook

UiPath continues to demonstrate strong enterprise adoption, particularly among its largest customers.

Customers generating more than $100,000 in annual recurring revenue increased from 2,365 to 2,624 over the past year, reflecting broader platform adoption and continued expansion within existing enterprise accounts.

Even more encouraging, customers contributing more than $1 million in ARR increased from 316 to 374. These larger customers typically represent deeper deployments, stronger retention and greater long-term expansion opportunities.

The company's expanding enterprise presence also strengthens its competitive position relative to Pegasystems, ServiceNow and Salesforce. While Salesforce continues to invest aggressively in enterprise AI and workflow automation, UiPath is carving out a differentiated position by combining robotic process automation, AI orchestration and workflow management into a single platform. Likewise, Salesforce's broader AI initiatives further validate the growing enterprise demand that UiPath is targeting.

Healthy Growth Projections Strengthen

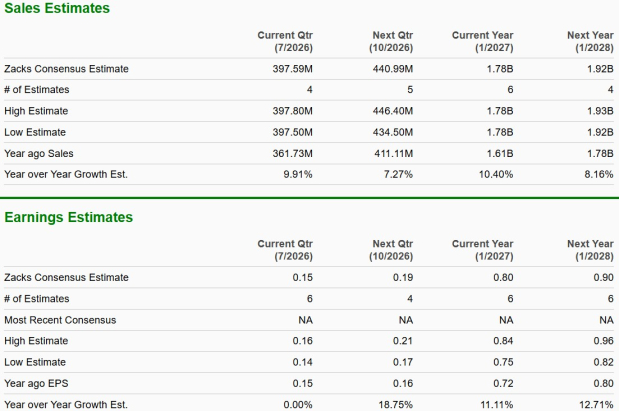

UiPath's long-term growth outlook remains healthy, supported by steady expansion in both earnings and revenues. The Zacks Consensus Estimate projects earnings growth of 10.4% in fiscal 2027, followed by an additional 8.2% increase in fiscal 2028, indicating sustained profitability despite a maturing business. Revenue growth is also expected to remain robust, with sales forecast to rise 11.1% in fiscal 2027 and 12.7% in fiscal 2028. The acceleration in top-line growth during fiscal 2028 suggests continued demand for UiPath's AI-powered automation platform, while consistent earnings expansion reflects improving operating leverage and disciplined execution.

Although risks such as enterprise IT spending uncertainty and intensifying competition remain, much of this caution now appears reflected in the current valuation, creating a more favorable risk-reward profile for patient investors.

Attractive Valuation Creates a Better Entry Point

The recent pullback has compressed its valuation to a forward price-to-earnings multiple of 13.82X, well below the industry average of 28.28X.

The lower valuation comes despite improving business fundamentals. Annualized recurring revenue (ARR) continues to expand steadily, operating margins have improved and UiPath recently reported its first-ever first-quarter GAAP profit. Management also raised its full-year guidance, signaling confidence in customer demand and the company's ability to monetize its expanding AI-powered automation portfolio.

PATH is a Buy Now

UiPath's recent share price weakness appears disconnected from its improving operating performance. The company is expanding profitability, growing recurring revenue, strengthening relationships with large enterprise customers, and successfully extending its platform into workflow orchestration and agentic AI.

Although competitive pressures and macroeconomic uncertainty remain important risks, UiPath's discounted valuation, expanding AI capabilities, and growing enterprise adoption suggest the long-term investment thesis remains intact. If management continues executing on its AI roadmap while sustaining profitable growth, the current pullback could prove to be an attractive buying opportunity for long-term investors.

PATH stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

UiPath, Inc. (PATH): Free Stock Analysis Report

ServiceNow, Inc. (NOW): Free Stock Analysis Report

Pegasystems Inc. (PEGA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).