Cummins CMI is no longer just a heavy-duty truck engine company. While its traditional engine business remains an important part of operations, the company is increasingly benefiting from its Power Systems segment.

Demand for backup power generators and data center power infrastructure is growing, providing Cummins with a stronger and less cyclical revenue stream. This shift is helping CMI drive earnings growth, reduce dependence on truck sales, and position the company to benefit from the expanding need for reliable power solutions.

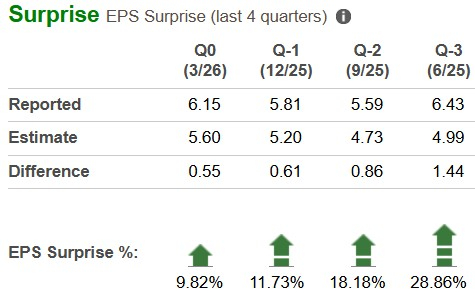

Cummins has a solid earnings surprise history.

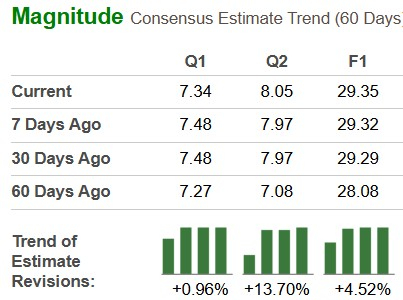

The Zacks Consensus Estimate for CMI’s 2026 and 2027 EPS implies a year-over-year uptick of 23% and 16%, respectively. The consensus mark for EPS has moved up over the last 60 days, depicting analysts’ growing optimism.

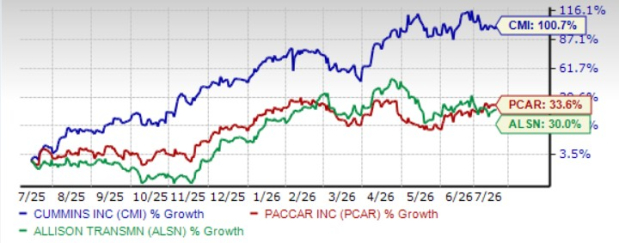

Cummins shares have almost doubled over the past year, handily outperforming peers like PACCAR PCAR and Allison Transmission Holdings ALSN.

After such a strong run, is it still worth buying Cummins or have you missed the bus? Let’s discuss.

Cummins Boosts Dividend

On July 12, CMI approved a quarterly dividend hike of 10% to $2.20/share. This marks the 17th consecutive year of a payout hike. The dividend will be paid on Sept. 3, 2026, to shareholders as of Aug. 21, 2026.

While the company's dividend yield stands at 1.18%, it has raised its dividend six times in the last five years, with a five-year annualized dividend growth rate of 8%. The payout ratio of 33% looks sustainable.

Reasonable debt levels and operational efficiency allow management to return value to shareholders. The company has a manageable long-term debt to capital ratio of 0.33. Cummins boasts an “A” credit rating from S&P Global Ratings. CMI's return on equity of 25% compares favorably with the auto sector's 5.85%.

CMI’s Strong Prospects Ahead

Cummins’ dividend hike isn't just a capital-return story— it's backed by genuine operating momentum. The clearest story is unfolding in Power Systems, where revenues jumped 19% year over year to $1.96 billion in first-quarter 2026 and EBITDA margin expanded from 23.6% to 29.5%. The segment benefited from surging demand for power generation equipment tied to data center buildout.

As AI infrastructure investment accelerates globally, the need for backup and prime power generation is becoming a durable long-term demand driver. Full-year 2026 guidance calls for Power Systems revenue growth of 14-19%, with margins expected to reach 25-26%, the highest for any Cummins segment, underscoring how central this business has become to the company's earnings trajectory.

The Distribution segment is riding the same wave. Its revenues grew 7% to $3.1 billion, with margins improving to 14.2% from 12.9%, again driven by stronger power generation demand across North America and Asia Pacific. Since Distribution also carries a meaningful mix of parts and service revenues, this growth adds a layer of earnings resilience that isn't tied to new equipment cycles alone.

Even Cummins' currently loss-making Accelera segment— which houses its battery, fuel cell, and electrolyzer businesses— is moving in the right direction. Adjusted EBITDA losses narrowed to $78 million in the last reported quarter from $86 million a year earlier, and full-year guidance points to losses shrinking further, to a range of $270 million to $300 million versus $438 million in 2025. What was once a drag on consolidated earnings is steadily becoming a smaller one, with the added potential for upside if electrification and hydrogen adoption accelerate.

Cummins’ Raised 2030 Financial Targets

Cummins raised its long-term financial targets, reflecting management's confidence in the company's growth prospects. At its 2026 Analyst Day, the company increased its expected annual revenue growth target to 6-9% through 2030, up from its historical growth rate of around 2%. It also expects more than 250 basis points of EBITDA margin expansion, while continuing share repurchases, dividend growth, and maintaining top-quartile return on invested capital.

These higher targets are supported by multiple growth drivers, including AI-driven data center demand and the expansion of its aftermarket business. Together, they suggest Cummins is entering a stronger and more profitable growth phase.

Conclusion

Cummins is evolving into a more diversified industrial company with multiple growth drivers beyond its traditional truck engine business. AI-led data center demand is creating a powerful new earnings engine, while its distribution business, improving Accelera economics, and disciplined capital allocation add further support.

The recent dividend hike reinforces management's confidence in future cash flows. Although the stock has rallied significantly over the past year, its improving earnings outlook and long-term growth opportunities suggest the story is far from over. For long-term investors, Cummins, carrying a Zacks Rank #2 (Buy), remains a compelling buy.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cummins Inc. (CMI): Free Stock Analysis Report

PACCAR Inc. (PCAR): Free Stock Analysis Report

Allison Transmission Holdings, Inc. (ALSN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).