Stitch Fix, Inc. SFIX reported second-quarter fiscal 2026 results, wherein the top and bottom lines beat the Zacks Consensus Estimate. Also, both metrics increased from the year-earlier quarter.

The fiscal second quarter reflected a period of continued transition for Stitch Fix, with management emphasizing disciplined execution and sharper strategic focus. The company continued refining its operating model, prioritizing brand relevance, assortment quality and a more consistent customer experience.

Artificial intelligence and data science remained central to these efforts, supporting personalization, inventory decisions and more efficient internal workflows. Management highlighted growing confidence in the impacts of these AI-driven initiatives as execution improved. Reflecting this momentum, the fiscal 2026 outlook was raised, signaling stronger conviction in the company’s forward trajectory.

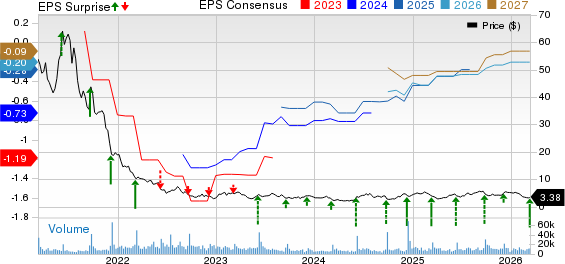

Stitch Fix, Inc. Price, Consensus and EPS Surprise

Stitch Fix, Inc. price-consensus-eps-surprise-chart | Stitch Fix, Inc. Quote

More on Stitch Fix’s Q2 Results

SFIX reported an adjusted loss of 2 cents per share, narrower than the Zacks Consensus Estimate of an adjusted loss of 5 cents. The metric was also narrower than the loss of 5 cents incurred in the year-ago quarter.

Stitch Fix recorded net revenues of $341.3 million, which surpassed the Zacks Consensus Estimate of $339 million. Also, the metric increased 9.4% from the year-ago quarter, supported by broad-based demand that remained resilient across all income cohorts.

The number of active clients engaged in ongoing operations was 2,288,000, marking a year-over-year decline of 3.5%. The average net revenues generated per active client (RPAC) from ongoing operations were $577, representing an increase of 7.4% from the previous year, which met our estimate.

This marks the eighth consecutive quarter of year-over-year growth and the highest RPAC reported since the company became public. The increase in RPAC indicates that the company’s strategy is effectively driving higher client engagement and spending, resulting in a greater share of wallet from clients.

The fix average order value (AOV) increased 9.8% year over year. This increase was driven by higher average unit retail, which increased 7.7% year over year, marking the sixth consecutive quarter of growth. This increase was largely supported by a more compelling assortment and a favorable product mix.

The category performance was led by outerwear, which rose 26% across women’s and men’s, while denim increased 17%. Activewear and athleisure grew 37% combined, special-occasion styles rose 46%, footwear advanced 33% with sneakers up 46%, and accessories increased 51%, underscoring broad-based demand strength and improving client engagement trends.

Insight Into SFIX’s Margins & Expenses

In the fiscal second quarter, this Zacks Rank #3 (Hold) company’s gross profit increased 7.3% to $148.9 million from $138.9 million in the year-ago period. However, the gross margin decreased 90 basis points (bps) year over year to 43.6%, with contribution margins remaining above 30% for the eighth consecutive quarter. We expected the gross profit to increase 6% year over year to $147.2 million.

Selling, general and administrative expenses (SG&A) increased 3.9% from $147.9 million in the prior-year quarter to $153.7 million. SG&A expenses, as a percentage of net revenues, were 45%, down 240 basis points from 47.4% in the prior-year quarter. Advertising represented 8.5% of revenues in the fiscal second quarter, slightly below the expected 9-10%.

Stitch Fix reported an adjusted EBITDA of $15.9 million, which remained flat year over year. We note that the adjusted EBITDA margin declined 40 bps year over year to 4.7% in the quarter under review.

SFIX’s Financial Snapshot: Cash, Inventory & Equity Overview

The company ended the fiscal second quarter with cash and cash equivalents of $118.8 million, short-term investments of $108.9 million, no debt, net inventory of $122.1 million, and shareholders’ equity of $209.3 million.

The net cash provided by operating activities was $7.3 million and the free cash was $3.4 million in the fiscal second quarter.

SFIX Stock Past 3-Month Performance

Image Source: Zacks Investment Research

Stitch Fix’s FY26 Guidance

For the third quarter of fiscal 2026, SFIX expects net revenues of $330-$335 million, reflecting year-over-year growth of 1.5-3.1%. Adjusted EBITDA is projected to fall $7-$10 million, implying an adjusted EBITDA margin of 2.1-3%.

For the second half of the year, the revenue guidance range has been tightened, reflecting greater confidence in the company’s underlying momentum, while maintaining a measured outlook on the broader environment. Growth rates are expected to moderate as the company laps a strong two-year AOV comparison, though there remains an opportunity to continue driving steady AOV improvement.

Ongoing enhancements to the client experience, including a stronger and more relevant assortment, continued category expansion, increased Fix flexibility and the use of AI to support more dynamic client engagement, are expected to provide a durable foundation for continued progress. At the same time, the company’s methodical approach to rebuilding its active client base is showing results. Continued improvement in active client trends is encouraging, and sequential net active client additions are expected to be positive in the fiscal third quarter.

Management raised its fiscal 2026 guidance, reflecting the positive business trends. For fiscal 2026, Stitch Fix forecasts total revenues between $1.33 billion and $1.35 billion, indicating year-over-year growth of 5-6.5%. Adjusted EBITDA is anticipated to be $42-$50 million, indicating a margin of 3.2-3.7%. The company expects the gross margin between 43% and 44%, while advertising expenses are projected to account for 9-10% of total revenues. Stitch Fix anticipates generating a positive free cash flow for the full fiscal year.

The SFIX stock has tumbled 37.5% in the past three months compared with the industry’s 7% decline.

Stocks to Consider

Some better-ranked stocks are FIGS Inc. FIGS, Deckers Outdoor Corporation DECK and Boot Barn Holdings, Inc. BOOT.

FIGS is a direct-to-consumer healthcare apparel and lifestyle brand, and it currently flaunts a Zacks Rank #1 (Strong Buy). FIGS delivered a trailing four-quarter earnings surprise of 187.5%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for FIGS’s current financial-year sales indicates growth of 11.4% from the year-ago reported number.

Deckers is a leading designer, producer and brand manager of innovative, niche footwear and accessories. It sports a Zacks Rank #1 at present.

The Zacks Consensus Estimate for Deckers’ current fiscal-year earnings and sales indicates growth of 8.5% and 8.9%, respectively, from the year-ago actuals. DECK delivered a trailing four-quarter average earnings surprise of 36.9%.

Boot Barn operates as a lifestyle retail chain devoted to western and work-related footwear, apparel and accessories. It currently carries a Zacks Rank of 2 (Buy).

The Zacks Consensus Estimate for Boot Barn’s current fiscal earnings and sales suggests growth of 26% and 17.7%, respectively, from the year-ago actuals. Boot Barn delivered a trailing four-quarter average earnings surprise of 4.9%.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Deckers Outdoor Corporation (DECK): Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT): Free Stock Analysis Report

Stitch Fix, Inc. (SFIX): Free Stock Analysis Report

FIGS, Inc. (FIGS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).