Zumiez Inc. ZUMZ reported impressive fourth-quarter fiscal 2025 results, wherein the top line came in line with the Zacks Consensus Estimate, while earnings surpassed the same. The top and bottom lines increased year over year. Also, comparable sales (comps) improved year over year.

The fiscal fourth-quarter results reflect continued resilience in Zumiez’s operations, highlighted by strong full-price selling in North America during the holiday season. This performance drove positive comparable sales growth and contributed to meaningful gross margin expansion. Overall, the results demonstrate the company’s ability to deliver profitable growth while navigating diverse market conditions.

More on Zumiez’s Q4 Results

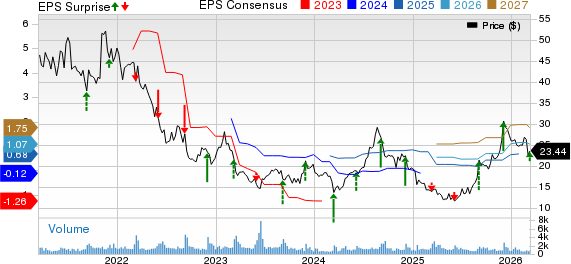

ZUMZ posted quarterly earnings of $1.16 per share, which beat the Zacks Consensus Estimate of $1.08. Also, the bottom line increased from 78 cents in the year-earlier quarter.

Zumiez Inc. Price, Consensus and EPS Surprise

Zumiez Inc. price-consensus-eps-surprise-chart | Zumiez Inc. Quote

Total net sales of $291.3 million increased 4.4% from $279.2 million in the prior-year quarter. This growth was largely driven by the strong performance in the North America business, which remained robust despite growing macroeconomic uncertainty, influenced by global trade policy developments.

Comps rose 2.2% year over year, marking the seventh consecutive quarter of growth. The Zacks Consensus Estimate for comps growth was pegged at 4% for the quarter under review. The rise in comps was driven by higher dollars per transaction and an increase in the number of transactions. Dollars per transaction rose due to a higher average unit retail and an increase in units per transaction.

ZUMZ’s Regional & Category Performance

From a regional perspective, North America’s net sales were $224.4 million, up 4.8% year over year. Other international sales, comprising Europe and Australia, were $66.9 million, up 3% year over year. Excluding the foreign currency translation impacts, North America net sales rose 4.6%, and other international net sales declined 7.1% over the prior-year quarter.

Comps in North America rose 5.5%, marking the eighth consecutive quarter of growth, while international comps declined 7.5% in the quarter under review.

By category, men’s merchandise delivered the strongest comps rise, followed by womem’s, hard goods and accessories. Footwear was the only category with negative comps.

Insights Into Zumiez’s Margins & Costs

Gross profit jumped 10.3% year over year to $111.4 million, whereas the gross margin expanded 200 bps to 38.2%. This rise was attributable to a 50-basis-point leverage in store occupancy costs due to higher sales, the closure of underperforming stores and 180 bps of product margin improvement. These gains were somewhat offset by a 20-bps impact from higher incentive costs tied to improved performance.

Selling, general and administrative (SG&A) costs of $86.4 million increased 6.7% from $80.9 million in the prior-year quarter. As a percentage of sales, SG&A was 29.6%, up 60 basis points from the year-ago quarter.

This increase was driven by a 100-basis-point of higher incentive costs tied to improved performance and 20 basis points related to corporate wage expenses. These benefits were partially offset by a 50-basis-point leverage in store wages, driven by higher sales and better management of labor hours, along with 20 basis points of leverage in other store operating costs.

Zumiez reported an operating income of $25 million compared with $20.1 million in the year-ago quarter.

ZUMZ’s Financial Health

As of Jan. 31, 2026, the company held $160.6 million in cash and current marketable securities compared with $147.6 million as of Feb. 1, 2025. The increase was primarily driven by $53.5 million in cash flow from operations, a $2.9 million gain from foreign currency fluctuation and the release of $2.7 million in restricted cash, partially offset by $38.3 million used for share repurchases and $11.1 million in capital expenditure. As of Jan. 31, 2026, the company had no debt.

Total shareholders’ equity was $324.3 million. In fiscal 2025, the company repurchased 2.7 million shares at an average cost of $14.18 per share, including commissions, for a total expenditure of $38.3 million. On March 11, 2026, the board of directors approved a new share repurchase authorization of up to $40 million of common stock. The program is expected to run through Jan. 29, 2028.

This Zacks Rank #3 (Hold) company ended the quarter with $147 million in inventory, a 0.2% increase from $146.6 million in the prior-year period. On a constant-currency basis, inventory levels were down 3.8% year over year.

ZUMZ’s Store Details

As of Feb. 28, 2026, Zumiez operated 716 stores, including 560 in the United States, 45 in Canada, 83 in Europe and 28 in Australia. Management continues to expect five store openings in fiscal 2026. They also plan to close 25 stores in fiscal 2026, including up to 20 in North America and five in Europe.

Closer Look at Zumiez’s Other Updates

Net sales for the four-week ended Feb. 28, 2026, increased 9.8% from the same period in the previous year. Comps for the period rose 7.5% year over year.

From a regional standpoint, net sales for the North America business increased 5.6% for the 31-day period, while net sales in other international markets increased 27.6%. Excluding the impacts of foreign currency translation, North America net sales increased 5.3%, and international net sales increased 12% from the prior-year period.

Comps in North America rose 6% for the four-week period ended Feb. 28, 2026, while comps in other international markets increased 13.2%. By category, hard goods delivered the strongest comps performance, followed by women’s, accessories and men’s. Footwear was the only category with negative comps.

ZUMZ’s Q1 Guidance

For the first quarter of fiscal 2026, Zumiez anticipates total sales of $189-$193 million, suggesting year-over-year growth of 3-5%. Comps are expected to increase 2-4%.

The operating loss is expected to be between $15.6 million and $17.8 million compared with a loss of $19.9 million in the prior-year quarter. The improvement is expected to be supported by product margin expansion in North America and Europe and the absence of a $2.9 million one-time wage-and-hour litigation settlement recorded in the first quarter of 2025. Overall, operating margin is projected to improve 140-270 basis points, driven by gross margin expansion of 130-200 basis points and SG&A leverage of 10-70 basis points.

The loss per share is estimated between 77 cents and 87 cents, whereas it incurred a loss of 79 cents in the prior year.

Zumiez’s FY26 Outlook

For fiscal 2026, Zumiez expects to build on the momentum from seven straight quarters of positive comparable sales and the steady start to the new year. While management remains confident in its strategy and operational execution, it continues to exercise caution due to uncertainty in the broader macroeconomic environment and therefore has not issued detailed annual guidance.

Sales trends in North America remain strong, and the European business is showing improvement after cycling past last year’s promotional activity and a difficult snow season that affected fourth-quarter results. Assuming relatively stable economic conditions, the company believes total sales could increase in the low-single-digit range for 2026, even after factoring in roughly $12 million in lost revenues from store closures.

ZUMZ also expects product margins to improve year over year, supported by continued operational progress in North America and disciplined pricing strategies in international markets. Growth in the private-label segment is anticipated to contribute to overall performance and may also provide benefits if current tariff conditions persist. Combined with anticipated sales growth, this is expected to generate leverage in SG&A expenses and lead to operating margin expansion of approximately 50-100 basis points in fiscal 2026. The company also expects its full-year effective tax rate to be around 35-40%, compared with 44.4% in fiscal 2025.

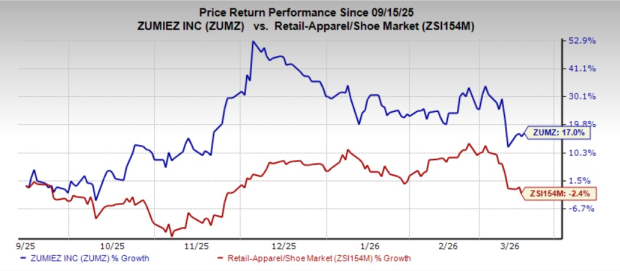

Capital expenditure for fiscal 2026 is expected to be between $14 million and $16 million, whereas it reported $11.1 million in fiscal 2025. Shares of the company have jumped 17% in the past six months against with the industry’s decline of 2.4%.

ZUMZ Stock's Price Performance

Image Source: Zacks Investment Research

Stocks to Consider

Deckers Outdoors Corporation DECK, together with its subsidiaries, designs, markets and distributes footwear, apparel and accessories for casual lifestyle use and high-performance activities in the United States and internationally. At present, Deckers sports a Zacks Rank #1 (Strong Buy).

You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for DECK’s current fiscal-year sales and earnings indicates growth of 8.9% and 8.5%, respectively, from the year-ago figures. DECK delivered a trailing four-quarter earnings surprise of 36.9%, on average.

Five Below, Inc. FIVE operates as a specialty value retailer in the United States. At present, FIVE sports a Zacks Rank of 1.

The consensus estimate for FIVE’s current fiscal-year sales and earnings implies growth of 22.1% and 25%, respectively, from the year-ago figures. FIVE has delivered a trailing four-quarter earnings surprise of 62.1 %, on average.

American Eagle Outfitters, Inc. AEO operates as a specialty retailer of casual apparel, accessories and footwear for men and women. At present, AEO sports a Zacks Rank of 1.

The Zacks Consensus Estimate for AEO’s current fiscal-year sales and earnings indicates growth of 4.6% and 16.7%, respectively, from the year-ago figures. American Eagle delivered a trailing four-quarter earnings surprise of 37.6%, on average.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zumiez Inc. (ZUMZ): Free Stock Analysis Report

American Eagle Outfitters, Inc. (AEO): Free Stock Analysis Report

Deckers Outdoor Corporation (DECK): Free Stock Analysis Report

Five Below, Inc. (FIVE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).