SSR Mining SSRM is setting up for a distinctly back-half weighted 2026. Management expects production to skew to the second half, with unit costs normalizing as volumes ramp. That creates a clearer line of sight to stronger free cash flow in the second half of 2026.

At the same time, near-term sequencing matters. Front-loaded sustaining capital, elevated first-half all-in sustaining costs, and ongoing costs tied to the suspended Çöpler asset keep early-2026 free cash flow under pressure. The investment debate centers on whether the cost curve improves on schedule and whether the Türkiye overhang clears.

SSRM’s Short-Term Rating Signals a Hold

SSRM carries a Zacks Rank #3 (Hold) for the one- to three-month horizon. Its Zacks Style Scores show a VGM Score of B, with Value at B, Growth at C, and Momentum at F. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

This combination points to a stock that looks reasonably priced on near-term earnings expectations and has a balanced fundamental profile, but is not showing strong near-term trading strength. For a one- to three-month window, that usually argues for patience rather than pressing either a bullish or bearish view.

SSR Mining’s Price Target Frames the Base Case

The six–12 month price target is $26.00, paired with a Neutral long-term stance. The setup reflects a “balanced risk/reward” view, where potential upside from higher second-half production and lower unit costs is offset by timing and cost uncertainty.

In this context, balanced risk/reward also ties to near-term free cash flow pressure. Sustaining capital is weighted to the first half while production is weighted to the second half, which can leave reported costs elevated early in the year and delay cash generation until later in 2026.

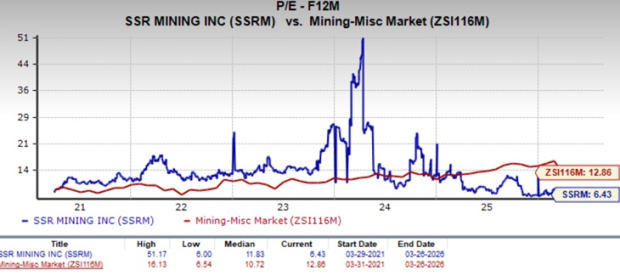

SSRM’s Valuation Discounts a Lot Already

On a forward 12-month earnings basis, SSRM trades at 6.43x. That compares with 12.86x for the Zacks sub-industry, 14.65x for the Zacks Basic Materials sector and 20.8x for the S&P 500.

The $26 price target is based on a 6.78x forward 12-month earnings multiple. Read that as the market already pricing in a meaningful amount of near-term risk, while leaving room for multiple support if the second-half cost and production normalization shows up as expected.

SSR Mining’s Bull Case Is a Cleaner Americas Platform

The constructive case starts with scale in the United States. SSRM is positioned as the third-largest U.S. gold producer, anchored by long-lived Marigold in Nevada and Cripple Creek & Victor in Colorado. Both assets are expected to be weighted toward second-half 2026 production, which supports the view that unit costs can improve as volumes rise.

Puna adds diversification and cash generation. The mine exceeded production guidance for a third straight year in 2025 and has continued work aimed at extending mine life, with pathways that include pit laybacks and additional targets under evaluation.

The growth pipeline is largely organic. The company is advancing brownfield work at Marigold (Buffalo Valley, New Millennium), Seabee (Santoy resource development and Porky engineering) and Puna. Consolidated 2026 growth spending totals $150 million, supporting medium-term visibility without relying on major acquisitions.

SSRM’s Bear Case is the 1H Cash Squeeze

The cautious case is mostly about sequencing risk. Management expects all-in sustaining costs to be highest in the first half across the portfolio, while sustaining capital is 60–70% weighted to the first half and production is 55–60% weighted to the second half. That mix can compress early-year margins and dampen first-half free cash flow.

Operational variability adds another layer. Marigold faces blending constraints and mine-plan complexity that can extend elevated unit costs, while Seabee’s cost profile has been volatile and remains sensitive to grades, mine development progress and scheduled maintenance.

Çöpler remains suspended and excluded from 2026 production and cost guidance, with no restart timing estimate. Care and maintenance costs are expected at roughly $35–$40 million per quarter, including $20–$25 million in cash care and maintenance per quarter that is included within consolidated all-in sustaining costs.

SSR Mining’s Capital Allocation is a Balancing Act

Liquidity is a core support for the story. The company ended 2025 with total liquidity of $1.0 billion and cash and equivalents of about $535 million, which helps fund 2026 sustaining capital of $202 million alongside development initiatives.

Capital returns are also on the table. The board authorized up to $300 million of share repurchases over the next 12 months, intended to be executed opportunistically.

The tension is timing. Buybacks, combined with pre-production funding needs at Hod Maden and first-half cost inflation, can tighten near-term free cash flow even if the longer-cycle outlook improves. Hod Maden spending is running ahead of a construction decision and development cash outflows come well before projected operating cash generation later in the decade.

SSRM’s Decision Checklist for Investors

Staying constructive depends on visible execution in the second half of 2026. Key markers include production and cost normalization as Marigold and CC&V ramp, plus evidence that portfolio all-in sustaining costs ease as planned after first-half peaks.

Clarity around Türkiye also matters. The company has a definitive agreement to sell its 80% stake in the Çöpler mine for $1.5 billion in cash, with an expected close in the third quarter of 2026 subject to approvals and customary conditions. Progress toward closing would reduce the ongoing care-and-maintenance burden and sharpen the portfolio’s Americas tilt.

Reasons to stay cautious include an extended period of elevated all-in sustaining costs, slippage in Marigold execution, a slower Seabee recovery, or a prolonged pre-production spending phase at Hod Maden that pushes cash generation further out.

Contextually, several Mining – Miscellaneous peers show how dispersion can be wide even within the same group. Fortuna Mining Corp. FSM and Wheaton Precious Metals Corp. WPM are listed among industry peers, both carrying Neutral on the peer table, underscoring that SSRM’s path is being judged more on execution and cash timing than on broad sector beta alone.

Where SSRM Could Surprise Next

The most recent quarter showed the operating leverage in the model when prices and mine performance cooperate. Fourth-quarter adjusted earnings were 88 cents per share compared with a 59-cent consensus estimate, alongside operating cash flow of $172.1 million and free cash flow of $106.4 million.

Looking ahead, “beat or miss” drivers are likely to center on price and volume sensitivity and cost phasing. If second-half volumes ramp as guided while first-half cost peaks fade on schedule, reported all-in sustaining costs should trend lower and free cash flow should improve. If cost inflation, mine-plan complexity, or downtime extends into the back half, the cash inflection could arrive later than expected.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Fortuna Mining Corp. (FSM): Free Stock Analysis Report

Silver Standard Resources Inc. (SSRM): Free Stock Analysis Report

Wheaton Precious Metals Corp. (WPM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).