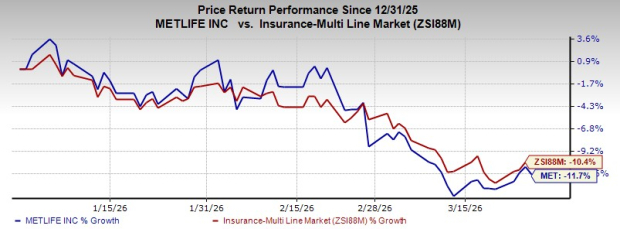

MetLife, Inc. MET is a global insurance-based financial services provider offering protection and investment solutions to both individual and institutional clients. Shares have lost 11.7% year to date, underperforming the broader industry’s 10.4% decline.

Image Source: Zacks Investment Research

Nevertheless, its diversified product portfolio, strong corporate relationships, and presence in more than 40 markets are likely to help shares bounce back in the days ahead.

From a valuation perspective, MetLife appears attractively priced. With a market capitalization of approximately $45.9 billion, the stock trades at a forward P/E ratio of 6.9X, which is significantly below the industry average of 8.3X, indicating potential undervaluation relative to its peers. The company has a Value Score of A.

Courtesy of solid prospects, MET currently carries a Zacks Rank #3 (Hold).

Where Do Estimates for MET Stand?

The Zacks Consensus Estimate for MetLife’s 2026 earnings is pegged at $9.85 per share, suggesting an 11.6% year-over-year increase. Over the past 30 days, the estimate has seen one upward revision compared to two downward revisions. The consensus estimate for 2026 revenues is pegged at $77.7 billion. The company’s earnings beat estimates in two of the trailing four quarters and missed in the other two, delivering an average surprise of 0.12%.

MetLife, Inc. Price, Consensus and EPS Surprise

MetLife, Inc. price-consensus-eps-surprise-chart | MetLife, Inc. Quote

MET’s Business Tailwinds

MetLife is expanding through targeted acquisitions and strategic alliances. Acquisitions of Versant Health, PetFirst, and PineBridge Investments, combined with partnerships with Aura, Nayya, and Fidelity Investments, are enhancing capabilities in benefits, asset management, and annuities. Initiatives like Chariot Re and expansion in India through PNB MetLife further enhance diversification and long-term growth potential.

MetLife has seen a steady recovery in premiums, supported by its diversified product portfolio, tailored insurance solutions, and strong relationships with large corporate clients. These factors help to maintain stable business volumes. Total premiums rose 10.8% year over year in 2025, driven by solid performance across its Asia, Group Benefits, RIS and EMEA segments.

The company is improving margins through disciplined cost management and technology adoption. Under its New Frontier 2025 strategy, MetLife is targeting lower unit costs via automation, AI-driven underwriting and streamlined operations. These efforts reduced the net direct expense ratio to 11.7% in 2025, supporting ongoing margin expansion.

MetLife has a strong balance sheet and solid liquidity. This supports consistent capital returns. At the end of 2025, it held $22 billion in cash and cash equivalents. This compares with $355 million in short-term debt and $14.5 billion in long-term debt, highlighting its financial strength. The company continues to return capital to shareholders. It had $2.1 billion remaining under its share repurchase authorization at the end of 2025.

Risks to Consider

MET’s investment income has been volatile in recent years and remained below target at $1.5 billion in 2025. The company expects $1.6 billion in 2026, but performance remains sensitive to private equity and real estate markets.

MetLife’s return on invested capital (ROIC) is 1.83%, below the industry average of 2.05%. This indicates relatively weaker capital efficiency and modest returns on its investments.

Key Picks

Some better-ranked stocks in the broader Finance space are The Allstate Corporation ALL, Mercury General Corporation MCY and HCI Group, Inc. HCI, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Allstate’s 2026 earnings is pegged at $26.01 per share, which has witnessed seven upward revisions in the past 30 days, with no movement in the opposite direction. ALL beat earnings estimates in each of the trailing four quarters, with the average surprise being 54.3%. The consensus estimate for 2026 revenues is pinned at $72.9 billion, implying 7.4% year-over-year growth.

The Zacks Consensus Estimate for Mercury General’s 2026 earnings is pegged at $9.00 per share, indicating 13.9% year-over-year growth. MCY has witnessed one upward revision in the past 30 days, with no movement in the opposite direction. The consensus estimate for 2026 revenues is pinned at $6.2 billion, implying 6.1% year-over-year growth.

The Zacks Consensus Estimate for HCI’s 2026 earnings is pegged at $16.88 per share, which has witnessed one upward revision in the past 30 days, with no movement in the opposite direction. HCI beat earnings estimates in each of the trailing four quarters, with the average surprise being 46.2%. The consensus estimate for 2026 revenues is pinned at $1 billion, implying 12.3% year-over-year growth.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

MetLife, Inc. (MET): Free Stock Analysis Report

The Allstate Corporation (ALL): Free Stock Analysis Report

HCI Group, Inc. (HCI): Free Stock Analysis Report

Mercury General Corporation (MCY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).