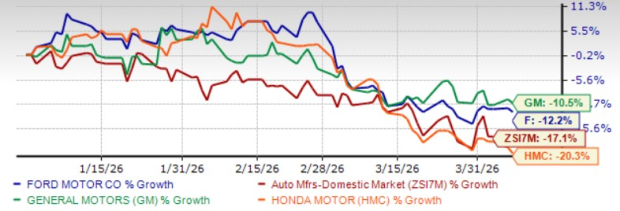

U.S. legacy automaker Ford F kicked off 2026 on a weak footing, and the numbers tell a clear story. The legacy automaker reported first-quarter deliveries of 457,315 vehicles, down 9% year over year. That decline reflects a broader slowdown across the auto industry as economic uncertainty, affordability concerns, elevated vehicle prices and high borrowing costs weigh on demand. Ford’s arch rival General Motors GM and Japan’s auto biggie Honda HMC also saw their U.S. deliveries fall around 10% and 4%, respectively.

Ford’s challenges were particularly visible across key segments. Its electric vehicle (EV) business took a sharp hit, with sales plunging nearly 70% year over year to just 6,860 units, following the withdrawal of federal tax incentives and persistently high EV price tags. Meanwhile, its crown jewel — the F-Series trucks — saw volumes drop 16% to 159,901 units. Management partly attributed this to production disruptions linked to last year’s aluminum plant fires, which constrained supply. Even hybrids, which had been a strong growth driver, saw sales fall nearly 20%. With the average new vehicle price hovering near $50,000 and financing costs still elevated, affordability remains a key headwind.

With Ford shares down 12% year to date, the market is clearly factoring in near-term headwinds. But the key question now is— does this represent a buy on dip opportunity, or is it better to stay on the sidelines, or even exit? Let’s take a closer look.

F Lags GM, Outperforms Industry & HMC

Challenges Grappling Ford

Ford is dealing with a series of operational and cost pressures that could keep near-term performance under strain. A key issue is the supply disruption caused by a fire at a Novelis aluminum plant. The impact already led to roughly $2 billion in losses last year, with another $1 billion expected this year. On top of that, Ford may incur $1.5–$2 billion in additional costs as it sources aluminum from alternative suppliers, adding further pressure on margins.

The company is also in the middle of reshaping its EV strategy, which isn’t coming cheap. It expects about $7 billion in special charges over the next two years, largely tied to strategy shifts and asset sales, with most of the cash impact likely in 2026.

Tariffs remain another drag. After a $2 billion hit last year, Ford still expects around $1 billion in tariff-related costs going forward, keeping cost pressures elevated.

Not All Doom & Gloom for Ford

Despite the near-term pressures, Ford still has a few strong levers working in its favor. Its commercial business, Ford Pro, continues to be a standout performer. Backed by solid order books and strong demand for Super Duty trucks, the segment is delivering healthy double-digit EBIT margins. Growth isn’t just coming from vehicles—software and services are playing a bigger role, with paid subscriptions rising 30% last year and profits from these streams expected to grow further this year.

Beyond autos, Ford is also building a presence in energy. Ford Energy is emerging as a strategic growth platform, with plans to invest $1.5 billion in 2026 and scale battery storage capacity significantly by 2027. This move not only diversifies revenues but also taps into a fast-growing, higher-margin market.

Financially, Ford remains on solid ground. It ended 2025 with about $50 billion in liquidity, including $29 billion in cash, giving it flexibility to navigate challenges while continuing to invest. Add to that a dividend yield of around 5%, and the stock still offers some income appeal.

Ford Valuation & Estimates Check

From a valuation perspective, Ford currently looks more attractive, especially on a price-to-sales basis. Ford trades at 0.26 forward sales, the same as Honda but better than General Motors’ 0.35. Ford currently carries a Value Score of A.

Ford P/S Vs. GM & HMC

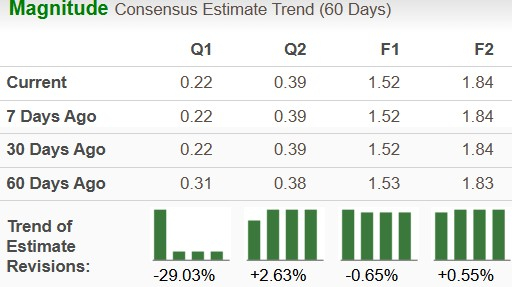

The Zacks Consensus Estimate for Ford’s 2026 sales and EPS implies year-over-year growth of 1% and 40%, respectively. The consensus mark for 2027 sales suggests a 1% year-over-year decline, while the EPS estimates point to 21% growth from projected 2026 levels. See how the EPS estimates have moved over the past 60 days.

Final Take

Ford is clearly navigating a tough phase, with weak deliveries, rising costs and multiple near-term headwinds limiting upside. While valuation looks inexpensive and businesses like Ford Pro and Energy offer long-term promise, the path to a meaningful recovery remains uneven and backloaded.

This doesn’t seem like a compelling entry point for new investors yet. However, the company’s strong liquidity, income appeal and strategic pivots provide enough cushion to avoid a bearish call. For existing investors, staying put makes sense, but new money is better off waiting for clearer signs of demand recovery.

Ford currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ford Motor Company (F): Free Stock Analysis Report

Honda Motor Co., Ltd. (HMC): Free Stock Analysis Report

General Motors Company (GM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).