Vertiv VRT and Teradyne TER are major players in the AI and data center infrastructure markets. While Vertiv provides critical digital infrastructure like cooling and power for data centers, Teradyne supplies semiconductor testing equipment essential for AI hardware growth.

According to International Data Corporation (IDC), spending on AI infrastructure is expected to surpass $758 billion by 2029, with 94.3% of the spending allocated to servers equipped with embedded accelerators. IDC expects momentum in AI investment to continue in 2026, driven by strong spending from hyperscalers and cloud service providers. According to Gartner, global AI spending is expected to exceed $2.52 trillion in 2026, up from around $1.76 trillion in 2025, representing roughly 44% year-over-year growth. Both Vertiv and Teradyne are expected to benefit from this rapid growth pace.

So, Vertiv or Teradyne — Which of these AI Infrastructure stocks has the greater upside potential? Let’s find out.

The Case for VRT Stock

Vertiv is benefiting from the robust demand for AI-driven infrastructure, which is driving significant growth in the data center market. The company’s extensive product portfolio, which spans thermal systems, liquid cooling, UPS, switchgear, busbars and modular solutions, has been noteworthy. In the trailing 12 months, organic orders grew approximately 81%, with a book-to-bill of 2.9 times for the fourth quarter of 2025, indicating a strong prospect.

Vertiv’s expanding portfolio has been noteworthy. In the fourth quarter of 2025, organic orders rose approximately 252% year over year, with the backlog increasing to $15.0 billion, up 109% compared with the fourth quarter of 2024 and 57% sequentially. This growth is primarily driven by the rapid adoption of AI and the increasing need for data centers to support the digital transformation.

Vertiv’s partnership with NVIDIA has been a key catalyst. In March 2026, Vertiv announced its partnership with NVIDIA to improve the combined physical infrastructure for AI factories. This will be done through DSX SimReady digital power and cooling assets, standardized 12.5MW modular building blocks Vertiv OneCore and system-level designs that integrate power, cooling and controls. The goal is to reduce deployment complexity, speed up readiness, improve scalability and enable digitally validated, high-performance AI infrastructure from the grid to the chip level.

Vertiv’s efforts to strengthen support for rapidly growing AI and high-density data center demand have been a major driver of growth. For first-quarter 2026, revenues are expected to be between $2.5 billion and $2.7 billion. Organic net sales are expected to increase in the 18% to 26% range.

The Case for TER Stock

Teradyne is benefiting from the surging demand for AI infrastructure, which has become a major growth driver for the company. In the fourth quarter of 2025, the company highlighted that AI-driven applications accounted for more than 60% of its revenue, up from 40% to 50% in the third quarter of 2025. This trend is expected to continue, with AI applications projected to drive up to 70% of revenues in the first quarter of 2026. The company’s focus on AI is driving robust growth across its semiconductor test and robotics divisions.

Teradyne’s acquisitions have played a crucial role in its success. The integration of Quantifi Photonics into its Product Test Group has expanded its capabilities in silicon photonics device testing, aligning with the growing demand for AI data center infrastructure.

Teradyne anticipates robust year-over-year growth in 2026 in the semiconductor test market, driven by AI compute and memory demand, as well as a moderate recovery in auto/industrial applications. The robotics segment is also expected to benefit from the increasing adoption of physical AI and advanced robotics in e-commerce and logistics.

Teradyne’s expanding portfolio and strong demand for AI-related applications are expected to drive the company’s top-line growth. For the first quarter of 2026, Teradyne expects revenues between $1,150 million and $1,250 million.

Price Performance and Valuation of VRT and TER

In the year-to-date period, Vertiv’s shares have gained 73.4%, and Teradyne’s shares have skyrocketed 85.1%. The outperformance in Teradyne can be attributed to strong AI-related demand, which is driving significant investments in cloud AI build-out as customers accelerate production of a wide range of AI accelerators, networking, memory and power devices.

Despite VRT’s expanding portfolio and clientele, the company is facing challenges in specific regions that have tempered overall performance. While the Americas showed exceptional growth, APAC faced headwinds due to muted demand in China, and EMEA experienced softness in sales despite improving market sentiment.

VRT and Teradyne Stock Performance

Image Source: Zacks Investment Research

Valuation-wise, Vertiv and Teradyne shares are currently overvalued as suggested by a Value Score of F.

In terms of trailing 12-month Price/Sales, Vertiv shares are trading at 7.37X, lower than Teradyne’s 13.06X.

VRT and Teradyne Valuation

Image Source: Zacks Investment Research

How Do Earnings Estimates Compare for VRT & TER?

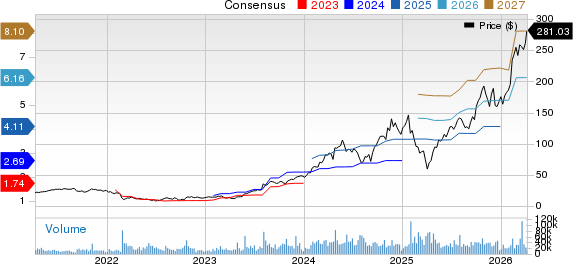

The Zacks Consensus Estimate for Vertiv’s 2026 earnings is currently pegged at $6.16 per share, which has increased by a penny over the past 30 days. This implies a 46.67% year-over-year rise.

Vertiv Holdings Co. Price and Consensus

Vertiv Holdings Co. price-consensus-chart | Vertiv Holdings Co. Quote

The Zacks Consensus Estimate for Teradyne’s 2026 earnings is currently pegged at $6.07 per share, which has remained unchanged over the past 30 days. This indicates a 53.28% year-over-year rise.

Teradyne, Inc. Price and Consensus

Teradyne, Inc. price-consensus-chart | Teradyne, Inc. Quote

Conclusion

While both Vertiv and Teradyne stand to benefit from the booming AI Infrastructure boom, Vertiv may offer greater upside potential due to its strong portfolio and rich partner base, which are driving order growth.

Despite Teradyne’s robust and diversified portfolio, uncertainty in Mobile TAM and inventory write-downs on legacy products remains a concern.

Both Vertiv and Teradyne carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Teradyne, Inc. (TER): Free Stock Analysis Report

Vertiv Holdings Co. (VRT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).