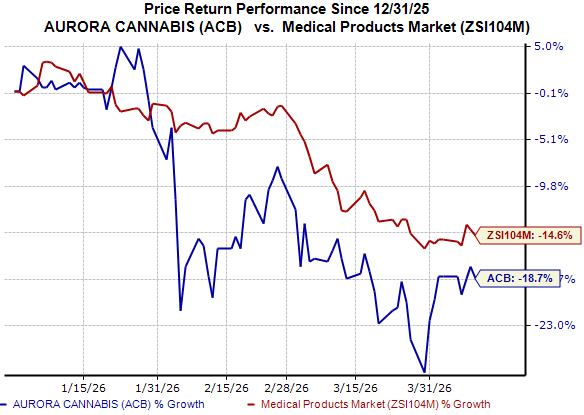

Shares of Aurora Cannabis ACB have lost 19% year to date compared with the industry‘s 15% decline, as shown in the chart below.

Image Source: Zacks Investment Research

The underperformance reflects a mix of sector-wide pressures and company-specific positioning. While intensifying competition in Canada’s mature cannabis market continues to weigh on Aurora Cannabis’ growth prospects, its limited presence in the United States has also constrained its ability to capitalize on recent cannabis-related policy momentum.

Let’s delve into the company’s fundamentals to better assess the stock following the decline.

Medical Cannabis Remains Aurora Cannabis’ Core Growth Engine

Aurora Cannabis continues to anchor its growth strategy around global medical cannabis, which remains the primary driver of both revenue and profitability. The segment has delivered consistent momentum, supported by strong demand across key international markets and a disciplined focus on higher-margin products.

For the nine months of fiscal 2026 (year ended March 2026), medical cannabis revenues increased about 20% year over year to C$211.5 million, accounting for nearly 75% of total sales. Growth was driven by increasing contributions from international markets, such as Germany, Australia and Poland, alongside steady demand in Canada from both insurance-covered and self-paying patients.

The strength of this segment is also evident in its margin profile. Higher-margin international sales, favorable product mix and ongoing production efficiencies have supported margin expansion through most of the fiscal year, with profitability levels stabilizing in the most recent quarter. This has translated into meaningful operating leverage, with adjusted EBITDA rising 35% year over year to about C$45 million for the nine months ended December 2025.

Aurora Cannabis’ latest updates further reinforce this trajectory. Management continues to prioritize international medical markets, where regulatory frameworks, pricing stability and demand visibility are more favorable compared to the recreational segment. The company is actively aligning its operations and capital allocation toward these markets, while streamlining lower-return activities to enhance overall profitability.

Aurora Cannabis expects global medical cannabis to remain its primary growth engine. The company expects fiscal 2026 medical cannabis revenues to be in the range of C$269-C$281 million, representing 10-15% year-over-year growth, supported by continued international expansion, new product launches and scaling in key European markets. Adjusted EBITDA is expected to reach C$52-C$57 million, with the company maintaining positive free cash flow as efficiencies improve.

ACB’s Consumer Cannabis Takes a Back Seat

Aurora Cannabis’ consumer cannabis business continues to weaken, reflecting structural challenges in Canada’s oversupplied adult-use market. Persistent price compression and aggressive competition have eroded both revenue potential and margins, making the segment increasingly unattractive relative to the company’s medical operations.

As a result, Aurora is now actively repositioning away from this segment. The company is scaling back participation in lower-margin consumer markets in Canada and redirecting capital and operational focus toward its higher-margin global medical cannabis platform. This shift highlights ACB’s effort to prioritize segments with stronger pricing power, more predictable demand and better long-term returns.

The strategic pullback is also expected to streamline Aurora’s cost structure. Management has indicated that reducing exposure to consumer cannabis should lower sales and marketing expenses and support consolidated margin expansion over time. However, the transition is not without near-term friction, with one-time costs expected to impact cash flow in the fourth quarter of fiscal 2026.

Intensifying Competition

Aurora Cannabis operates in an increasingly competitive global cannabis market, facing established players, such as Curaleaf Holdings CURLF and Tilray Brands TLRY. With most Canadian and international cannabis producers targeting a limited set of high-growth markets, competitive intensity remains elevated and could constrain ACB’s ability to sustain outsized market share gains.

This pressure is particularly pronounced in international markets, such as Europe, where Aurora Cannabis is focusing on its expansion strategy. Peers like Curaleaf and Tilray are also scaling their presence in these regions, increasing competition in the very markets expected to drive the company’s future growth. As a result, while international expansion offers meaningful opportunities, it also introduces execution risk and may limit pricing power over time.

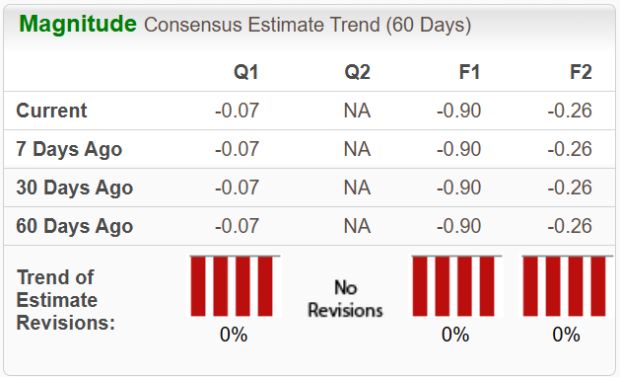

ACB Valuation Estimates

Estimate movements for fiscal 2026 and 2027 have remained unchanged over the past 60 days.

Image Source: Zacks Investment Research

How to Play ACB Stock?

Aurora Cannabis has made meaningful progress in repositioning its business, with medical cannabis emerging as a key growth driver and profitability improving. The company’s expanding footprint in international markets provides a pathway to offset structural challenges in Canada’s mature recreational market.

However, the investment case remains balanced. Persistent pricing pressure, ongoing weakness in the consumer cannabis segment and restructuring-related costs continue to weigh on near-term visibility. At the same time, rising competition in international markets could limit Aurora’s ability to fully capitalize on its medical cannabis momentum. Consistent earnings estimates suggest that the recent strategic progress is not yet translating into upward revisions, indicating limited near-term upside potential.

ACB currently carries a Zacks Rank #3 (Hold), which suggests that investors may be better off waiting for clearer signs of sustained earnings growth or improved industry conditions before building meaningful positions.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power , you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tilray Brands, Inc. (TLRY): Free Stock Analysis Report

Aurora Cannabis Inc. (ACB): Free Stock Analysis Report

Curaleaf Holdings, Inc. (CURLF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).