The Travelers Companies, Inc. TRV has delivered solid financial performance over the past year, supported by consistent revenue growth. In 2025, the company generated approximately $48.8 billion in revenues, reflecting a 5.2% year-over-year increase, following a stronger 12.2% growth in 2024.

Net written premiums remain a key growth driver for TRV, up 2.4% in 2025 after a stronger 7.8% increase in 2024. This continued growth indicates that the company is still expanding its core insurance business. Strong customer retention, higher renewal pricing and increased new business in segments like auto and homeowners insurance are encouraging signs. A hard market leads to higher pricing, which, coupled with prudent underwriting standards, should continue to drive premiums higher and ensure sustained profitability. However, the slower pace of growth suggests that the company is moving into a more stable phase rather than a high-growth period.

Investment income is another major strength. It grew 10.3% in 2025 and 22.9% in 2024, providing an important boost to overall performance. With around $100 billion invested largely in fixed income assets, TRV benefits from stable and predictable returns. TRV now expects fixed income NII for 2026, including earnings from short-term securities, to be $3.3 billion with about $800 million in the first quarter and growing to about $870 million in the fourth quarter.

As an insurance company, TRV remains exposed to risks such as natural disasters, interest rate fluctuations, and pricing competition, all of which can impact performance. Overall, TRV’s revenue growth appears reliable but moderate, supported by steady customer retention, strong fundamentals, and consistent investment income rather than rapid expansion.

What About TRV’s Competitors?

TRV closely competes with large firms like The Progressive Corporation PGR and The Allstate Corporation ALL.

The Progressive continues to benefit from strong underlying drivers, as net premiums earned rose 15.3% year over year in 2025 and net investment income increased 26.5% over the same period. PGR has consistently maintained high policyholder retention, particularly in its core auto insurance segment. This ensures a stable and recurring revenue base without relying heavily on new customer acquisition.

The Allstate’s revenue growth is supported by steady premium increases, along with disciplined pricing and selective acquisitions. In 2025, ALL reported revenues of $67.7 billion, marking a 5.6% year-over-year increase. Net premiums earned grew 7.3% year over year in 2025. Net investment income is rising, providing further support to overall revenue stability and growth.

TRV’s Price Performance

Shares of Travelers have gained 20.7% in the past 12 months, outperforming the industry’s 7.9% decline.

Image Source: Zacks Investment Research

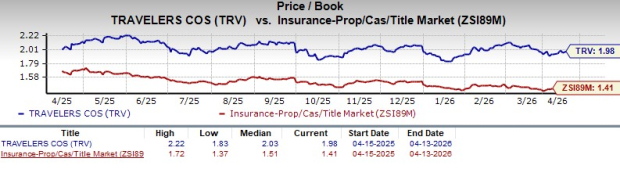

Valuation of TRV

TRV trades at a price-to-book ratio of 1.98, above the industry average of 1.41. It carries a Value Score of A.

Image Source: Zacks Investment Research

Estimates for TRV

The consensus estimate for earnings indicates 1.27% year-over-year decline in 2026, followed by a 3.08% growth in 2027. Over the past 30 days, estimates have seen five upward and two downward revisions. The consensus estimate for revenues projects year-over-year growth of 2.6% in 2026 and 2.8% in 2027.

Travelers currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Travelers Companies, Inc. (TRV): Free Stock Analysis Report

The Allstate Corporation (ALL): Free Stock Analysis Report

The Progressive Corporation (PGR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).