West Pharmaceutical Services, Inc. WST is well-positioned for growth, backed by strong demand for HVPs, expanding GLP-1 drug programs and regulatory-driven Annex 1 conversions. However, tariff impacts, destocking in generics and execution challenges at constrained European facilities are concerning.

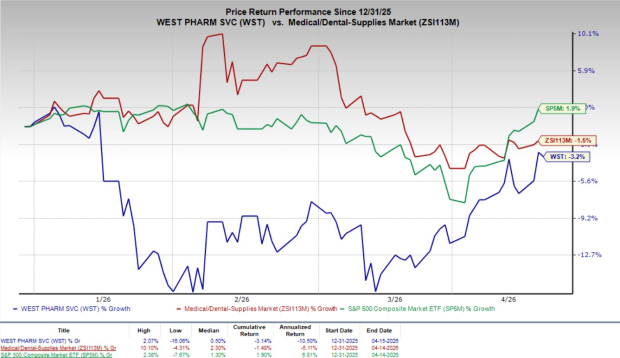

Shares of this Zacks Rank #3 (Hold) company have lost 3.2% year to date compared with the industry's 1.5% decline. The S&P 500 Index has risen 1.9% in the same time frame.

West Pharmaceutical, with a market capitalization of $19.31 billion, is a leading global manufacturer, engaged in the design and production of technologically advanced, high-quality, integrated containment and delivery systems for injectable drugs and healthcare products. Its earnings are anticipated to improve 11.9% over the next five years. The company delivered a trailing four-quarter average earnings surprise of 17.39%.

Image Source: Zacks Investment Research

Positive Factors Driving WST’s Prospects

Strong Demand for HVP Components: Strong demand for high-value product (HVP) components is expected to remain the primary growth engine for West Pharmaceutical. Demand continues to outpace supply, fueled by the rapid expansion of biologics, GLP-1 therapies and regulatory upgrades, such as Annex 1.

HVP components are projected to deliver high-single-digit to low-double-digit organic growth in 2026. Annex 1 conversions are driving hundreds of projects across global pharma partners, while HVP products generate margins two to three times higher than standard products. Management expects the HVP mix to rise 100 basis points annually, supporting higher profitability.

Exposure to GLP-1 Therapeutics: West Pharmaceutical is benefiting from rapid growth of GLP-1 therapies for diabetes and obesity. The market continues to expand, supported by both oral and injectable formats. Rather than replacing injectables, oral GLP-1 drugs are attracting new patients. Penetration remains in the early stages, with a low-single-digit adoption among eligible patients, leaving substantial room for growth. A variety of injectable delivery systems, including auto-injectors and multi-dose pens, are expected to coexist.

Upcoming launches of GLP-1 generics are speeding up in 2026, following patent expiries in March, with major launches active in India and expected soon in Brazil, China and Canada. Several pharmaceutical companies, such as Sun Pharma, Dr. Reddy’s and Zydus, are working to introduce lower-cost versions of leading GLP-1 generics such as semaglutide in India. These launches are expected to generate incremental business for WST.

Strong Cash Flow & Margin Expansion: The company’s strong cash flow generation and improving margins support its growth outlook. With capital expenditure expected to normalize at 6-8% of sales, West Pharmaceutical anticipates sustained cash flow, enabling continued investment in capacity expansion and innovation as demand for HVP components grows. Management expects more than 100 basis points of margin expansion in 2026, driven by a richer HVP mix and the divestiture of the SmartDose business, positioning the company for stronger profitability and earnings growth.

Key Challenges Facing WST

Operational Constraints & Execution Risks:West Pharmaceutical faces near-term operational challenges, particularly at a European HVP facility where hiring and training delays are constraining capacity. Management aims to resolve these issues over the next 12-18 months through network optimization and technology transfers, but execution risks remain. Any delays could disrupt supply, strain customer relationships and defer high-margin revenues. New manufacturing capacity, such as the Dublin facility, requires lengthy validation cycles, which may limit near-term utilization and introduce earnings volatility.

Industry Destocking & Demand Normalization:West Pharmaceutical continues to see destocking pressures in generics and, to a lesser extent, in biologics, which are impacting order volumes and clouding demand visibility. While normalization is expected over time, a prolonged destocking cycle could weigh on short-term growth. Easing post-pandemic demand in certain drug categories may reduce the urgency for capacity expansion, leading to moderate growth and limited near-term revenue visibility.

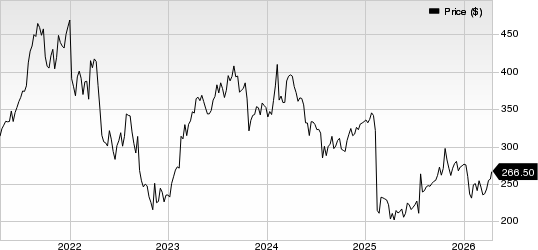

West Pharmaceutical Services, Inc. Price

West Pharmaceutical Services, Inc. price | West Pharmaceutical Services, Inc. Quote

Estimate Trend

WST has been witnessing a negative estimate revision for 2026. In the past 30 days, the Zacks Consensus Estimate for earnings has moved 0.13% south to $7.91 per share, implying a gain of 8.5% from the prior-year reported level. The consensus mark for revenues is pegged at $3.25 billion, indicating a 5.7% increase from the 2025 reported level.

Key Picks

Some better-ranked stocks from the broader medical space are Pacific Biosciences of California PACB, Phibro Animal Health PAHC and GE HealthCare Technologies GEHC.

Pacific Biosciences of California, currently sporting a Zacks Rank #1 (Strong Buy), reported a fourth-quarter 2025 adjusted loss of 12 cents per share, 36.8% narrower than the Zacks Consensus Estimate. Revenues of $44.6 million beat the Zacks Consensus Estimate by 9.4%. You can see the complete list of today’s Zacks #1 Rankstocks here.

PACB has an estimated earnings recession rate of 1.9% compared with the industry’s 12.9% rise. The company’s earnings beat estimates in the trailing four quarters, the average surprise being 27.7%.

Phibro Animal Health, currently carrying a Zacks Rank #2 (Buy), reported second-quarter fiscal 2026 adjusted earnings per share (EPS) of 87 cents, which surpassed the Zacks Consensus Estimate by 27.1%. Revenues of $373.9 million beat the Zacks Consensus Estimate by 4.7%.

PAHC has an estimated long-term earnings growth rate of 21.5% compared with the industry’s 12.1% rise. The company’s earnings beat estimates in the trailing four quarters, the average surprise being 20.1%.

GE HealthCare Technologies, currently carrying a Zacks Rank #2, reported fourth-quarter 2025 adjusted EPS of $1.44, which surpassed the Zacks Consensus Estimate by 0.7%. Revenues of $5.7 billion beat the Zacks Consensus Estimate by 1.9%.

GEHC has an estimated long-term earnings growth rate of 9.1% compared with the industry’s 12.1% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 7.5%.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

West Pharmaceutical Services, Inc. (WST): Free Stock Analysis Report

Pacific Biosciences of California, Inc. (PACB): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

GE HealthCare Technologies Inc. (GEHC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).