OptimizeRx OPRX is trading at a forward 12-month price-to-sales ratio of 1.09, a discount compared with the Zacks Computer Software industry’s 7.13 and the Zacks Computer & Technology sector’s 6.38.

Image Source: Zacks Investment Research

The stock also appears to be lucratively discounted compared to its peers, such as Omnicell OMCL, Doximity DOCS, and Veeva Systems VEEV, with forward 12-month P/S ratios of 1.37, 6.46 and 7.46, respectively. Omnicell develops comprehensive automation solutions for medication management, including dispensing systems, pharmacy storage and packaging, bedside tools, order management, decision support and web-based procurement.

Doximity is a top-tier U.S. medical network, used by more than 85% of physicians and a majority of NPs and PAs. It offers a HIPAA-compliant platform with marketing, hiring and workflow tools like telehealth, messaging and AI support. Most of its revenue comes from subscriptions. Veeva Systems provides cloud software and data solutions for life sciences, including Veeva CRM, Vault, Network and data services. Its flagship Veeva CRM runs on Salesforce’s SaaS platform.

Valuation gaps often spark investor interest, especially when they appear in sectors with strong long-term tailwinds. OptimizeRx, a digital health platform that connects pharmaceutical companies with patients and healthcare providers, is currently trading at a discounted valuation.

The big question is whether this discount signals an opportunity or a warning? Let’s find out.

OPRX’s Strategic Positioning in Healthcare and AI

At its core, OptimizeRx operates in a rapidly evolving space. The healthcare industry is increasingly shifting toward digital engagement, with pharmaceutical companies seeking more targeted, data-driven ways to reach both physicians and patients. Its platform provides value by enhancing brand visibility at the point of care, reducing prescription abandonment, improving interoperability across healthcare systems and supporting the adoption of specialty medications.

Looking ahead, AI is expected to further strengthen the company’s value proposition. Management believes AI will redirect pharmaceutical marketing budgets from content creation to targeted execution and reach, areas where OptimizeRx already excels. This positions the company to capture a larger share of marketing spend, deliver higher ROI for clients and deepen integration within healthcare workflows.

OptimizeRx is seeing strong traction with its DAAP platform, as initial pilots evolve into scaled, multi-brand engagements. A leading pharma client expanded its investment in 2025 to support multiple oncology brands, driving solid revenue growth, while a flagship med tech client progressed from point-of-care marketing to full DAAP adoption after strong script gains. By enabling precise, timely outreach to high-value prescribers, DAAP has become a key differentiator, helping clients scale across brands and channels. This recurring model, moving from targeted engagement to platform-wide adoption, is driving larger investments and stronger ROI across both pharma and med tech customers.

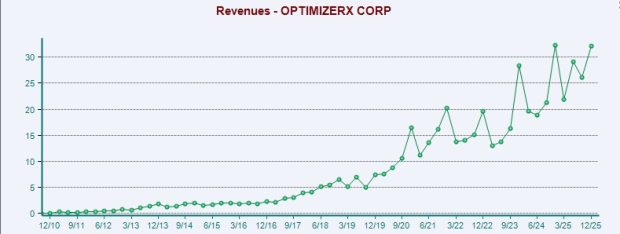

Image Source: Zacks Investment Research

OptimizeRx reported full-year 2025 revenue of $109.4 million, a 19% increase year over year, driven by strong execution and a scalable operating model. Growth was fueled by both large clients and an expanding base of mid-tier and long-tail life sciences customers, a segment with substantial growth potential. Improved product mix, partner strategy and cost optimization following the Medicx acquisition boosted margins, more than doubling adjusted EBITDA and free cash flow.

Another highlight in 2025 was its strong cash generation, with operating cash flow rising to $18.7 million from $4.9 million in 2024 and cash balance increasing to $23.4 million from $13.4 million. This improved liquidity gives OPRX flexibility to invest in growth, navigate macro uncertainty and potentially return capital to shareholders, while reinforcing its shift toward a more sustainable, self-funded growth model.

OPRX Navigating Emerging Headwinds

Despite the strong performance, management acknowledged potential near-term challenges. A key concern is market volatility driven by uncertainty around Most Favored Nation (MFN) pricing policies. This has led to more cautious customer spending, shorter contract durations and delayed discretionary investments. While these factors could create temporary pressure on growth, they do not appear to adversely impact the long-term demand for OptimizeRx’s platform, which remains strong.

Against this backdrop, OptimizeRx lowered its 2026 revenue forecast,citing shifting pharma spend and managed services drag, but signals recovery ahead and stronger EBITDA expectations. It expects 2026 revenues of $109-$114 million compared with the $118-$124 million provided at the end of the third quarter of 2025. Softness in contracted revenues, linked to a broader market shift away from managed services, is a major challenge. Management noted that the first half of 2025 saw $9 million higher managed services revenues, which are not expected to repeat this time around.

Amid macro uncertainty, the company is prioritizing margin stability and cash generation over aggressive expansion. It aims to sustain Rule of 40 performance, even in a challenging environment. OptimizeRx reiterated its focus on adjusted EBITDA, guiding $21-$25 million for 2026, higher than the previously mentioned $19-$22 million.

Furthermore, OptimizeRx announced a $10 million share repurchase program, effective March 2026 through March 2027, to be funded from existing cash reserves. The move signals management’s confidence in the company’s undervalued stock and aligns with its improving fundamentals and profitability.

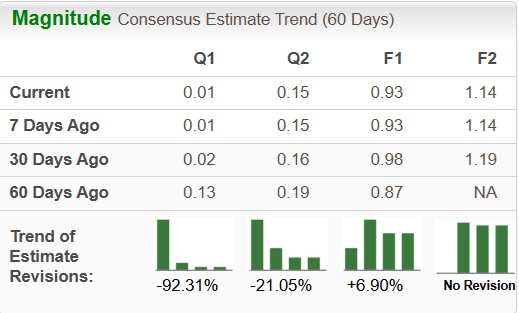

OPRX’s Estimate Revision Trend Favorable

OPRX’s estimates are currently on an upward trajectory. The Zacks Consensus Estimate for OPRX’s earnings for fiscal 2027 has been revised upward over the past 60 days.

Image Source: Zacks Investment Research

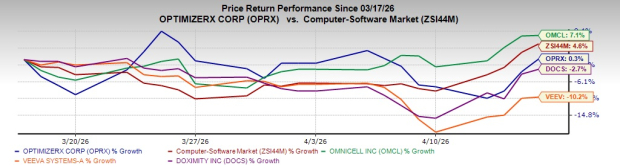

OPRX Price Performance

Shares of OptimizeRx have gained 0.3% in the past month compared with the Zacks Computer Software industry’s rise of 4.6%. The stock has outperformed DOCS and VEEV’s plunge of 2.7% and 10.2% in the same time frame. However, it lagged OMCL’s 7.1% rise.

Image Source: Zacks Investment Research

Investment Perspective: Buy OPRX Now

OptimizeRx is evolving into a profitable, cash-generating platform with durable competitive advantages. It operates at the intersection of healthcare, data and digital engagement, helping life sciences companies connect with healthcare professionals and patients more effectively. Given these tailwinds, a discounted valuation might seem surprising. Companies aligned with digital transformation trends command premium multiples. In OPRX’s case, however, the market appears to be pricing in a degree of uncertainty. Concerns around revenue consistency, execution and profitability have likely contributed to the lower valuation.

Ultimately, OPRX sits at the intersection of opportunity and uncertainty. The company benefits from strong industry tailwinds and a differentiated platform, but it must prove its ability to deliver consistent financial performance. For investors willing to accept some volatility and take a longer-term view, the current valuation could offer upside potential. More cautious investors, however, may prefer to wait for clearer signs of sustained growth and margin improvement.

Boasting a Zacks Rank #1 (Strong Buy) at present, OPRX seems to be a good bet. You can see the complete list of today’s Zacks #1 Rank stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Omnicell, Inc. (OMCL): Free Stock Analysis Report

OptimizeRx Corp. (OPRX): Free Stock Analysis Report

Veeva Systems Inc. (VEEV): Free Stock Analysis Report

Doximity, Inc. (DOCS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).