Adobe’s ADBE prospects in fiscal 2026 and beyond will depend much on the success of its ongoing and future AI initiatives. The latest Firefly AI Assistant, powered by its creative agent, is designed to help creators by reducing manual effort and speeding up the creative process. This new tool is a part of Adobe’s ongoing AI push to advance its footprint among business, creative and marketing professionals amid intensifying competition. Let’s dig deep to find out how Adobe’s AI push is gaining traction.

Adobe’s Firefly AI Assistant to Smoothen Up Creative Process

Adobe’s Firefly AI Assistant helps creators to edit their work through descriptive prompts. Adobe management touts this development as a “fundamental shift in how creative work is done” as its approach to agentic creativity continues to put creators in control. The new Firefly AI Assistant tool will handle the orchestration and execution of the vision, judgement and creative direction provided by the user. Firefly AI Assistant includes features such as a unified conversational interface, context awareness across sessions, and integration with Frame.io for streamlined feedback and revisions.

Adobe is also expanding Firefly’s capabilities with advanced video and image editing tools, including enhanced audio, color adjustments, and precision editing features like Precision Flow and AI Markup. Additionally, Firefly now integrates more than 30 leading AI models, offering creators greater flexibility. Overall, Adobe aims to redefine creative workflows by combining speed, control, and AI-powered assistance in one platform.

The latest tool is expected to drive up the Creative and Marketing Professionals segment. In the first quarter of fiscal 2026, segment revenues increased 12% year over year (11% in constant currency) to $4.39 billion, driven by the Creative Cloud Pro offering, higher subscription penetration among professionals and teams and increased usage across design, video and photo workflows. Creative freemium MAUs crossed 80 million, growing more than 50% year over year and include web and mobile versions of Firefly, Express, Premiere Pro, Photoshop and Lightroom. Adobe expects Creative and Marketing Professionals subscription revenues between $4.41 billion and $4.44 billion for the second quarter of fiscal 2026.

Adobe Faces Multiple Challenges: Will AI Push Deliver?

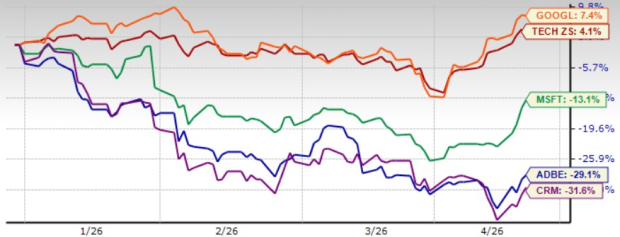

Adobe shares have plunged 29.1% year to date. The company has been playing a catch-up role in the AI domain, not only against established players like Microsoft MSFT, Alphabet GOOGL, and Salesforce CRM but also from AI-native companies like OpenAI, Midjourney, and Canva. The departure announcement of long-term CEO Shantanu Narayan has added to the investor risk in a challenging macroeconomic and geopolitical environment. This, along with rising monthly active users (MAUs) of new AI-first offerings (Acrobat Studio with Adobe Express, Firefly and GenStudio), is expected to hurt annualized recurring revenue (ARR). Adobe targets ARR growth of 10.2% for fiscal 2026, which is a decline from 10.9% reported in fiscal 2025.

Year to date, ADBE shares have underperformed the Zacks Computer and Technology sector’s appreciation of 4.1%. Shares of Salesforce and Microsoft have dropped 13.1% and 31.6%, respectively, while Alphabet has returned 7.4% over the same time frame. Adobe’s AI-related revenues are minuscule compared with Microsoft, Alphabet and Salesforce. Microsoft’s Intelligent Cloud revenues are benefiting from growth in Azure AI services and a rise in the AI Copilot business. Alphabet’s focus on infusing AI heavily across its offerings, including Search and Google Cloud, has been a major growth driver. Salesforce’s strategy of continuous expansion of generative AI offerings is helping it tap growth opportunities.

ADBE Stock’s Price Performance

Image Source: Zacks Investment Research

Nevertheless, Adobe’s AI push is gaining traction. The company’s business professionals and consumer business are benefiting from solutions like PDF Spaces and Acrobat AI Assistant. Acrobat and Express integrations are empowering users to turn content they are consuming into generated presentations, infographics, audio summaries and more. Adobe is benefiting from an expanding partner base and integrations with leading AI ecosystems, including Amazon Web Services, Azure, Google Gemini, Microsoft CoPilot and OpenAI. Adobe has launched Acrobat and Express for ChatGPT and expects to see similar integrations into Copilot, Claude and Gemini.

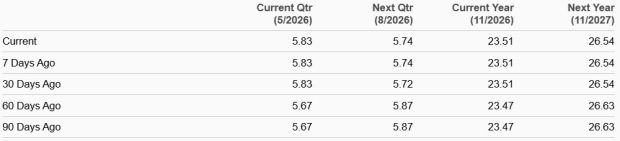

Adobe’s Earnings Estimate Revision Trend Steady

For the second quarter of fiscal 2026, Adobe expects total revenues between $6.43 billion and $6.48 billion. The Zacks Consensus Estimate for revenues is currently pegged at $6.46 billion, indicating 9.9% growth from the figure reported in the year-ago quarter.

Consensus Estimate Trend

Image Source: Zacks Investment Research

Adobe expects fiscal second-quarter non-GAAP earnings between $5.85 and $5.90 per share. The consensus estimate for earnings is currently pegged at $5.83 per share, unchanged over the past 30 days, indicating 15.2% growth from the figure reported in the year-ago quarter.

Adobe Inc. Price and Consensus

Adobe Inc. price-consensus-chart | Adobe Inc. Quote

Here’s Why Adobe Shares Are a Hold Now

Adobe has a Value Score of B, which suggests the stock is trading at a discount. In terms of price/earnings (P/E), Adobe shares are trading at 10.07X lower than the broader sector’s 24.07X, Microsoft’s 22.83X, Alphabet’s 27.8X and Salesforce’s 13.47X.

ADBE’s Valuation

Image Source: Zacks Investment Research

Adobe’s continuing AI integration into its solutions, an innovative portfolio and rich partner base, along with a cheap valuation, are positives for investors already holding the stock. However, AI-related disruption, softer ARR growth, headwinds related to the CEO transition, and stiff competition make the stock a risky bet in the near term for prospective investors.

ADBE currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Salesforce, Inc. (CRM): Free Stock Analysis Report

Adobe Inc. (ADBE): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).