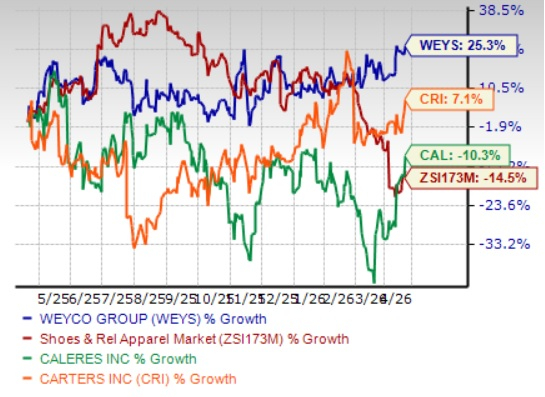

Weyco Group, Inc. WEYS shares have gained 25.3% in the past year against the industry’s 14.5% growth. The company has outperformed other industry players, including Carter's, Inc. CRI and Caleres, Inc. CAL. Shares of Carter’s have rallied 7.1%, while Caleres stock declined 10.3% in the same time frame. WEYS benefits from strong brand equity, diversified sourcing, expanding e-commerce channels, a broad distribution network, international presence and a robust, debt-free balance sheet supporting growth initiatives.

Image Source: Zacks Investment Research

A Key Look Into WEYS’ Business Operations

Weyco Group, a Wisconsin corporation founded in 1906 as Weyenberg Shoe Manufacturing Company and renamed in 1990, designs, markets, and distributes footwear for men, women, and children under brands like Florsheim, Nunn Bush, Stacy Adams, and BOGS. Its products include mid-priced leather dress shoes, casual footwear, and outdoor boots. The company sources finished goods mainly from China and India. Operations are divided into Wholesale (about 78% of 2025 sales), Retail (13%), and international businesses (9%), including Florsheim Australia. Wholesale products are sold through over 10,000 North American retailers, while Retail focuses on e-commerce and four U.S. stores. BOGS sales are seasonal, peaking in colder months.

Weyco’s Key Tailwinds

Weyco benefits from a strong portfolio of well-established footwear brands, including Florsheim, Nunn Bush, Stacy Adams, and BOGS, which provide significant brand equity and customer recognition. These brands span multiple categories such as dress, casual, and outdoor footwear, enabling the company to serve a wide range of consumer preferences. Its long operating history and ongoing focus on product design and innovation further reinforce its competitive position. Additionally, the company’s extensive distribution network — reaching more than 10,000 retail locations across North America — supports broad market penetration and consistent product visibility.

Another important strength lies in the company’s flexible and diversified sourcing model. By relying on over 80 third-party suppliers across multiple countries, Weyco can better manage costs and mitigate supply disruptions. The company has also been actively diversifying production away from China, improving supply chain resilience amid shifting trade dynamics. Management’s ability to maintain production flow and meet delivery schedules despite tariff-related disruptions highlights strong operational execution and adaptability in a challenging environment.

The growing contribution of e-commerce is a key positive factor for the company’s future growth. Weyco has been investing in its direct-to-consumer platforms, which are expected to play an increasingly important role as consumer purchasing behavior continues to shift online. This strategy allows the company to capture higher margins, strengthen customer relationships, and reduce dependence on traditional retail partners. With a relatively small brick-and-mortar footprint, the company is well-positioned to scale its digital operations efficiently while maintaining cost discipline.

Geographic diversification also supports the company’s long-term outlook. Beyond its core North American operations, Weyco operates internationally through businesses such as Florsheim Australia, which includes markets like Australia, South Africa, and New Zealand. These operations provide additional revenue streams and reduce reliance on any single region.

Finally, the company’s strong financial position enhances its strategic flexibility. Weyco maintains a solid balance sheet with substantial cash and marketable securities and no outstanding debt. This financial strength allows it to invest in growth initiatives, manage macroeconomic volatility, and return capital to shareholders through dividends and share repurchases.

Challenges Persist for WEYS’ Business

Weyco faces multiple headwinds that could pressure growth and margins, including heavy reliance on foreign sourcing, particularly from China and India, exposing it to supply chain disruptions, geopolitical risks, tariffs, and rising freight, labor, and material costs. Incremental tariffs and volatile trade policies have already increased product costs and compressed margins, while the company may be unable to fully pass these costs to consumers without hurting demand. The firm also operates in a highly competitive market with larger players, leading to pricing pressure and reduced profitability. Shifts in fashion trends toward casual footwear, changing retail dynamics including e-commerce disruption and declining foot traffic, and consolidation among retail partners further strain sales.

WEYS’ Valuation

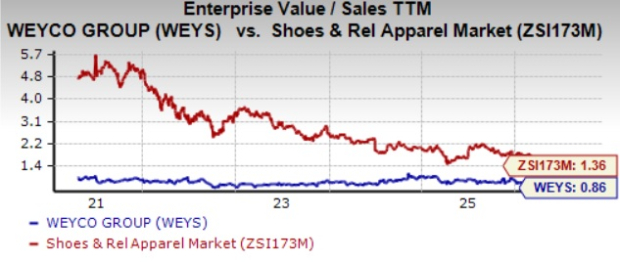

The company is cheaply priced compared with the industry average. Currently, WEYS is trading at 0.86X trailing 12-month EV/sales value, below the industry’s average of 1.36X. However, the metric remains higher than both the company’s peers, Carter’s (0.52X) and Caleres (0.16X).

Image Source: Zacks Investment Research

Conclusion

Despite challenges such as supply chain exposure, tariff pressures, and intense industry competition, Weyco's strong portfolio of established brands, diversified sourcing strategy, expanding e-commerce presence, geographic reach, and debt-free balance sheet position it to navigate challenges and deliver steady long-term value for investors.

Strong fundamentals, coupled with WEYS’ undervaluation compared to the industry average, present a lucrative opportunity for investors to add the stock to their portfolio.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Weyco Group, Inc. (WEYS): Free Stock Analysis Report

Carter's, Inc. (CRI): Free Stock Analysis Report

Caleres, Inc. (CAL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).