Analysts are upgrading their Intel Corp (INTC) price targets after its recent earnings results, and based on management's expectation of positive free cash flow this year. One way to play it is to sell short INTC out-of-the-money puts, which have high yields.

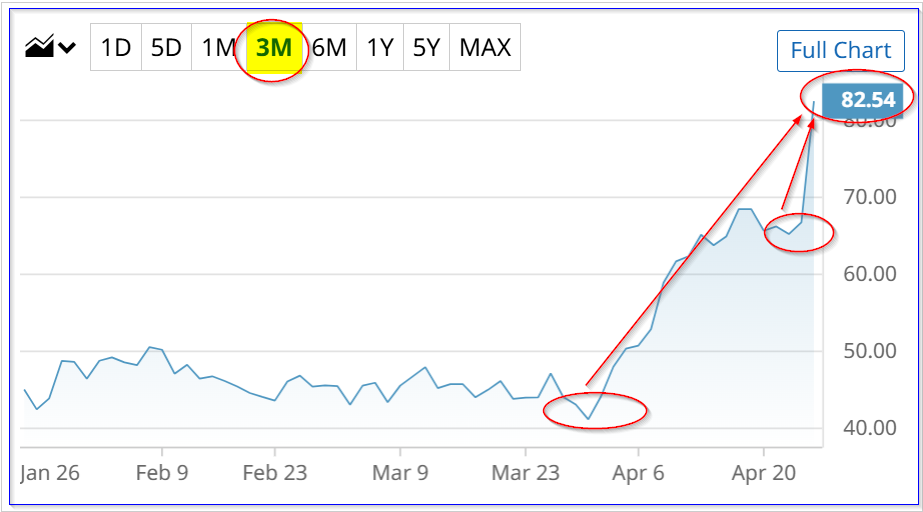

INTC closed at $82.54, up +23.60% after its Q1 earnings results the night before on April 23. Its price target could exceed $100 per share, as this article will show.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

INTC stock - last 3 months - Barchart - April 24, 2026

INTC stock - last 3 months - Barchart - April 24, 2026 Intel reported that its Q1 revenue rose 7.2% YoY. Moreover, adjusted earnings per share (EPS) were 29 cents compared to 15 cents in Q4 (up +93% QoQ) and just 13 cents a year ago (+123% YoY).

The growth was driven by high demand for its CPU products, which management said was continuing to outpace its growing supply. This is driven by investments in artificial intelligence by many of Intel's clients.

Moreover, despite recording a negative adjusted free cash flow (FCF) of $2.016 billion, management said it expects full-year FCF to be positive. In addition, the CFO indicated that Intel expects to retire $2.5 billion in debt as it comes due this year.

That allows analysts to forecast FCF going forward.

Strong FCF Outlook and Valuation

Analysts now project revenue will rise to $58.43 billion this year and $63.72 billion next year. Based on its expected FCF margin, it's possible to forecast Intel's FCF next year.

For example, if Intel makes positive FCF this year, it would need to generate at least $2.01 billion plus $2.5 billion (for debt payments) over the next 9 months. That works out to almost an 8% FCF margin:

$4.6 billion FCF / $58.43 billion revenue 2026 = 0.0787 = 7.87% FCF margin

So, assuming next year that 8% magin applies to analysts' revenue estimates, Intel could generate $5 billion in FCF:

0.08 x $63.72 billion 2027 revenue est. = $5.1 billion FCF

That could be why Intel stock has moved so much. Its valuation could be much higher.

For example, using a 1.0% FCF yield (i.e., assuming 100% of its FCF is paid out to shareholders and the market gives INTC a 1.0% dividend yield:

$5.1b / 0.01 = $510 billion market value

That is 22% higher than its present market cap of $415 billion, according to Yahoo! Finance. In other words, INTC's price target for the next year is 22% higher:

$82.54 x 1.22 = $100.70 per share

However, there's no guarantee INTC will reach this target price. After Friday's close, it may reverse. One way to play it, to set a lower price target, is to sell short out-of-the-money (OTM) put options.

That way, an investor can take advantage of high put option premiums and get paid while waiting to buy in at a lower breakeven point.

Shorting OTM INTC Puts

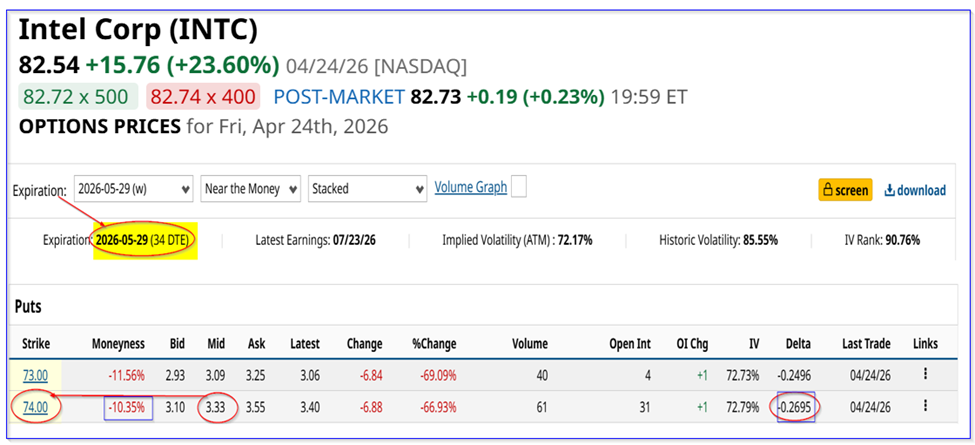

For example, the May 29 expiry period shows that a 10%+ lower put option contract has a midpoint premium with a 4.50% one-month yield. The premium is $3.33 at the midpoint, as of Friday, so an investor could make $333 after securing $7,400:

$333/$7,400 = 0.045 = 4.55

INTC puts expiring May 29 - Barchart - as of Friday, April 24

INTC puts expiring May 29 - Barchart - as of Friday, April 24 Moreover, for even more conservative investors, the $73.00 strike price put has a slightly lower yield, but the distance is 11.56% away from Friday's close:

$309/$7,300 = 0.0401 = 4.23%

That way, an investor who secures $7,300 or $7,400 can earn income while waiting to see if INTC drops 10-11%. There is just a 27% chance of it falling to $74.00, based on its delta ratio, and 25% at $73.00.

In any case, even if INTC drops, the actual breakeven is lower. Here are the breakeven points, if the account is assigned to buy shares at $73 or $74:

$74.00 - $3.33 = $70.67, i.e., -14.38% lower

$73.00 - 3.09 = $69.91, -15.3%

The point is, this is a great way to set a lower potential buy-in, and get paid while waiting. Given the volatility in INTC stock, this might be one way to play it.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Intel Could Still Be Undervalued Based on Strong Free Cash Flow Unusual Put Activity Is Flagging a Smart Trade Setup in This New Quantum Computing Stock Domino's Pizza Stock Could Be Cheap Ahead of Earnings Next Week 17 Unusually Active Call Options: Buy 3 for Under $300 and Big Potential Profits