Consumer discretionary stocks have been stuck in a tough place for a while now, and Nike is the poster child for that struggle. The last couple of months have been particularly brutal. Investors keep hearing the word "turnaround," but the scoreboard shows a stock down roughly 30% year-to-date (YTD) in 2026 and more than 64% over three years. The brand is iconic, the swoosh is everywhere, yet sales are sluggish, China remains weak, and profits keep shrinking. Into this messy picture lands the latest headline: Nike just announced it will cut roughly 1,400 jobs. That makes two rounds of layoffs in a single year. The news lands in late April with shares hovering near $45, and it raises a simple but uncomfortable question.

Is slimming down the org chart finally going to spark the recovery investors have been waiting for, or is this just another painful chapter in a story that is taking too long to turn the page?

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

www.barchart.com

www.barchart.com Nike’s Business Is Still Large, But Growth Is Uneven

The latest quarter showed both progress and pain. For the third quarter, Nike posted revenue of $11.279 billion, flat year-over-year (YOY) and down 3% on a currency-neutral basis. Nike Brand revenue rose 1%, wholesale revenue climbed 5%, and NIKE Direct revenue fell 4%. Converse was the weak spot, with sales down 35%.

The worse part is that Net income fell 35% to $520 million, and diluted EPS also dropped 35% to $0.35. Cash and short-term investments ended the quarter at $8.1 billion.

The cash flow picture was a little better over the first nine months of the fiscal year. Nike generated $1.231 billion of operating cash flow, while capital spending came to $546 million. That implies roughly $685 million of free cash flow for the quarter and about $2.9 billion on a nine month basis. The number is not flashy, but it still gives Nike room to keep funding the reset.

CEO Elliott Hill said, “The work is not finished, but the direction is clear.” CFO Matthew Friend added that “Win Now actions will continue to impact results over the balance of the calendar year.” That is the real message from the quarter. Nike sees progress, but it is still paying for the cleanup.

What Happened With the Latest Job Cuts

Nike’s newest layoff round adds another layer to that cleanup. Reuters reported that the company will cut about 1,400 jobs, or less than 2% of its global workforce, mainly in global operations and technology. It is the second round of layoffs this year, following earlier cuts tied to automation and restructuring.

And, Nike is consolidating tech operations in Oregon and India. Investors initially viewed the move as part of a leaner operating model, but it also underlines the amount of work that remains inside the business. The stock barely needs more bad news, yet Nike keeps showing that the turnaround still has a cost.

Management Is Still Pushing the Reset

Nike’s 2026 playbook is still focused on simplification. The company has pulled back promotions, pushed product innovation, and leaned harder into core sports like running. Reuters said the company expects China sales to fall 20% in the current quarter, which is a reminder that Greater China remains a major problem area. Additionally, Nike plans to resume full-year guidance at an investor day this fall, which shows that management is still not ready to promise a clean recovery path. The good news is that the company is acting. The bad news is that investors still have to wait for the results.

Additionally, Nike does not look cheap in the classic sense. Its trailing price-to-earnings ratio is about 29.48 times, which is well above the sector median of 15.82 times. That is a rich multiple for a business still in reset mode. On the other hand, the dividend yield of 3.67% is above the sector median of 2.4%, so income investors get some cushion while they wait. This is not a bargain bin stock. It is a brand stock that still needs to earn its premium.

What Do Analysts Think of NKE Stock?

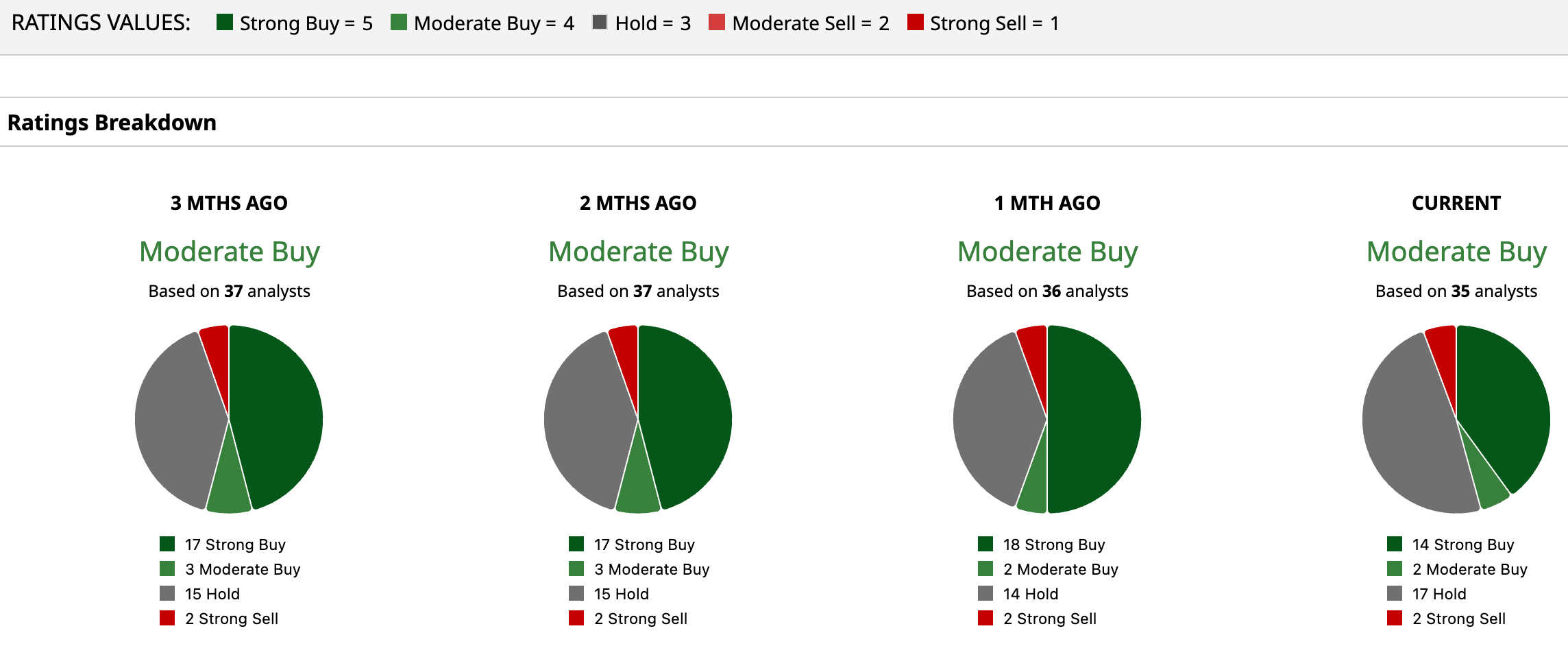

Wall Street is still split, but the stock carries a current “Moderate Buy” rating from 35 analysts, with an average recommendation of 3.74. Also, the mean target price is $61.57, which points to 37.4% upside from recent levels. That is a decent gap, but not an easy call.

The firm-level opinions show the divide clearly. Barclays cut its target to $67 but kept an “Overweight” rating, saying the China reset could take four quarters to get back to growth. JPMorgan stayed “Neutral” with a $52 target. Stifel cut its target to $56 and kept “Hold,” while Bank of America remained “Neutral” with a $55 target.

That mix says the Street still sees a turnaround but not a smooth one. The bulls are betting the brand heals faster than expected. The bears think the reset will keep dragging into 2026.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Investors Are Waiting for the Nike Stock Turnaround. Will the Latest 1,400 Job Cuts Be Enough? Newmont Is Golden: Why Record Gold Prices Make It a Must-Buy Dividend Stock Now The 3 Dividend Aristocrats Wall Street Calls a ‘Strong Buy’ With Up to 46% Upside Upcoming Foldable iPhones Make These 2 Chip Stocks a Buy Now, According to Barclays