In a world of AI investments focused only on chipmakers, companies like Marvell Technology (MRVL) stand out. Marvell doesn’t just design chips. It builds the underlying technology — like high-speed networking and storage controllers — that helps data move quickly and efficiently inside AI data centers. More importantly, Marvell is starting to check multiple boxes that long-term investors typically look for in a winning AI infrastructure play. MRVL stock is up 93% year-to-date (YTD), sharply outperforming the broader market’s gain of 5% so far this year.

Here are three key reasons why Marvell looks like a compelling AI stock to buy now.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Marvell Is Powering the Data Flow Behind AI’s Growth

Marvell’s key position in the AI value chain is showing up in the numbers. In fiscal 2026, the company generated $8.2 billion in revenue, an increase of 42% year-over-year (YOY). Interestingly, more than $6 billion of that revenue came from data-center business alone, which grew 46% YOY. This growth is not coming just from chips, but from high-performance networking technology that cloud companies rely on.

In terms of technology, Marvell is already one step ahead. While the industry expands into 800G speeds, Marvell is already moving into 1.6T solutions, with production starting in the fourth quarter of calendar year 2026. Management emphasized that there is strong early demand from customers, with the interconnect business expected to grow more than 50% in fiscal 2027, up from an earlier estimate of 30%. As data needs grow faster than ever, companies are willing to pay for reliable, high-speed connectivity, giving Marvell essential pricing power in this highly competitive market. This is why Marvell is confidently raising its own revenue targets.

Organic Growth Is Driving Repeated Revenue Upgrades

Marvell keeps raising its own forecasts as demand continues to surpass expectations. In Q4 fiscal 2026, revenue jumped 22% YOY to $2.22 billion, while adjusted EPS hit $0.80, beating guidance by $0.10. Marvell initially projected fiscal 2027 revenue of roughly $9.5 billion, then later raised its guidance to $10 billion. Now, the firm expects fiscal 2027 revenue to reach $11 billion, which would mark 34% YOY growth. Impressively, this growth is also entirely organic, as the recently acquired Celestial AI and XConn businesses are not expected to contribute meaningfully until fiscal 2028.

Simply put, Marvell’s core business alone is outperforming expectations. For fiscal 2028, the company is targeting $15 billion in revenue, with growth close to 40% and adjusted EPS exceeding $5 per share. The Celestial AI and XConn acquisitions are expected to contribute $250 million to total revenue in fiscal 2028.

Looking beyond 2028, the Amazon (AMZN) and Anthropic mega deal could be advantageous for Marvell. Amazon is investing up to $25 billion in Anthropic, while Anthropic has committed to spending more than $100 billion on AWS infrastructure over the next decade. This deal is less about AI models and more about a massive, long-term buildout of cloud infrastructure. As Anthropic commits to spending billions on AWS, Amazon will scale its custom AI chips like Trainium. But Amazon doesn’t build Trainium chips alone — it partners with Marvell on custom AI silicon development. Accordingly, Marvell stands to benefit from this deal over the next 10 years.

Growing Aggressively Without Breaking Financial Discipline

High-growth semiconductor stories often come with messy balance sheets or aggressive spending. But Marvell is doing the opposite. It is scaling aggressively while staying financially controlled and still rewarding shareholders.

Marvell ended fiscal 2026 with cash and equivalents of $2.63 billion as well as a manageable debt-to-equity ratio of 0.31. The company also returned $2.24 billion to shareholders through buybacks and dividends, up by roughly $1.3 billion from fiscal 2025. Instead of hoarding cash, the firm is confident enough in its growth strategies to return capital while investing aggressively.

The Bottom Line on MRVL Stock

Marvell isn’t the loudest name in AI. But it sits in a part of the semiconductor manufacturing process where it becomes more valuable as AI scales. The cherry on top is that MRVL is both a growth stock and an income stock. Down about 4% from its 52-week high of $170.84, Marvell stock is a solid buy on the dip now.

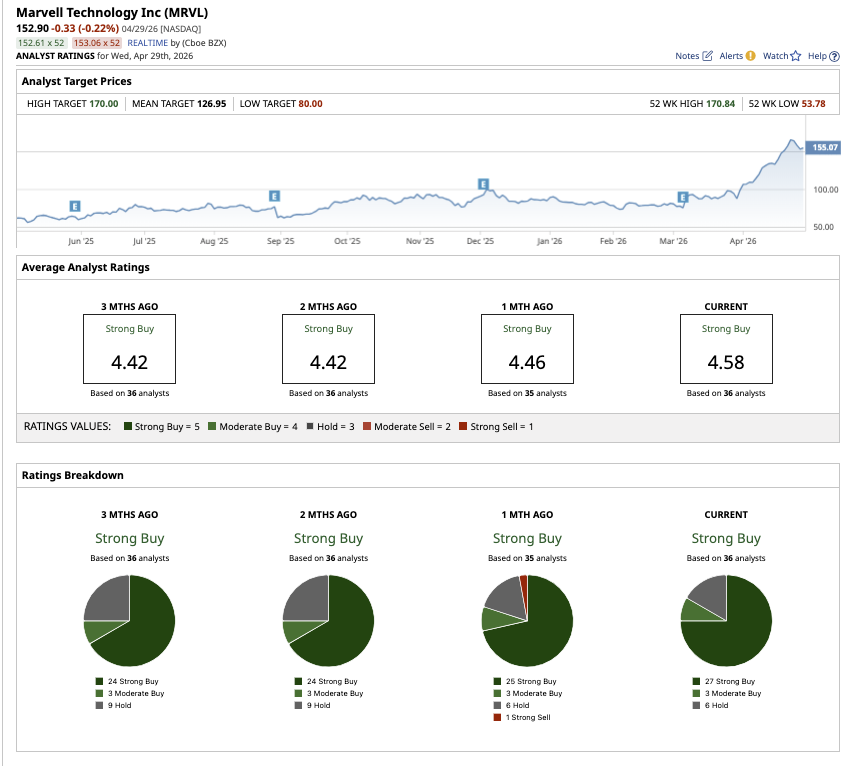

Overall, analysts remain strongly bullish about MRVL stock. Out of the 36 analysts covering shares, 27 have a “Strong Buy,” three have a “Moderate Buy” recommendation, and six suggest a “Hold” rating. Marvell stock has surpassed its average price target of $126.95. However, the high target price of $170 implies potential upside of 4% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

AutoZone Stock Is Up 3,500% Over the Past 20 Years — But It Owes $8 Billion More Than It Owns. Should the Company Still Exist? As Data Center Demand Grows, Susquehanna Says You Should Buy AMD Stock Before May 5 Bloom Energy Is Now a Data Center Stock. Buy Its Shares Now. 3 Reasons Why Marvell Stock is a Buy Now