Visa (V) is the world’s preeminent digital payments technology platform, connecting consumers, merchants, and financial institutions across more than 200 countries. Visa has evolved from a traditional credit card provider into a sophisticated "network of networks." Today, the company facilitates over $15 trillion in annual volume through its secure global network, VisaNet. By pioneering “Agentic Commerce,” where AI agents autonomously handle transactions, and expanding into stablecoin settlements and B2B money movement, Visa remains the critical infrastructure powering the shift from physical cash to a seamless, digital-first global economy.

Founded in 1958, headquartered in San Francisco, California.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Visa Stock Recovers

Visa stock has demonstrated resilient growth, recently recovering from early-year volatility to challenge. Over the past year, the shares have been down roughly 5% but have recovered with a 10% gain in their last month, driven by strong double-digit revenue growth and a record-breaking capital return strategy. Despite navigating regulatory headwinds and shifting interest rate expectations, Visa’s consistent earnings power continues to attract long-term investors who view the company as a foundational blue-chip holding in the digital payments sector.

Compared to the S&P 500 Financials Index ($SRFI), Visa has underperformed over the trailing 12 months, while the index has gained 7%. However, in the short term, the stock has outperformed the sector’s 8% growth in the month.

www.barchart.com

www.barchart.com Visa Strong Results

Visa delivered a stunning performance for its second fiscal quarter, reporting net revenue of $11.2 billion, a staggering 17% increase year-over-year (YoY). The company posted a non-GAAP EPS of $3.17, surpassing the analyst consensus of $3.14.

Growth was broad-based, with Data Processing revenue surging 18% to $5.5 billion and Service revenue climbing 13% to $5.0 billion. Key operational drivers remained robust: payment volume increased 9%, cross-border volume excluding intra-Europe rose 11%, and processed transactions grew 9% to nearly 70 billion. Notably, Visa returned a record $9.2 billion to shareholders this quarter through dividends and $7.9 billion in stock buybacks.

Management raised its outlook for the remainder of fiscal 2026, anticipating low double-digit growth in adjusted net revenue and earnings per share. CEO Ryan McInerney highlighted the global expansion of the "Agentic Ready" program, which prepares the ecosystem for AI-initiated payments. Despite a $4.2 billion client incentive hit and ongoing litigation provisions, the company's focus on value-added services and tokenization, which has now reached 5 billion credentials, positions it to capture the next wave of autonomous, agent-led commerce through 2027.

$20 Billion Share Buyback

During its second-quarter results report, Visa’s board of directors provided a massive vote of confidence in the company’s future by authorizing a new $20 billion multi-year share repurchase program. This move is particularly significant as it comes on the heels of a record-breaking quarter where Visa already returned $9.2 billion to shareholders, including $7.9 billion in direct stock buybacks.

This new authorization allows the company to potentially retire up to 3.6% of its outstanding shares, creating a powerful structural tailwind for earnings per share growth regardless of broader market volatility.

For investors, this $20 billion commitment serves as a "safety net" and a growth engine combined. By aggressively reducing the share count, Visa is effectively concentrating its future profits into fewer hands. This massive buyback program underscores Visa's exceptional ability to generate free cash flow, $2.6 billion in Q2 alone, and its commitment to returning that value to those who hold the stock.

Should You Buy V Stock?

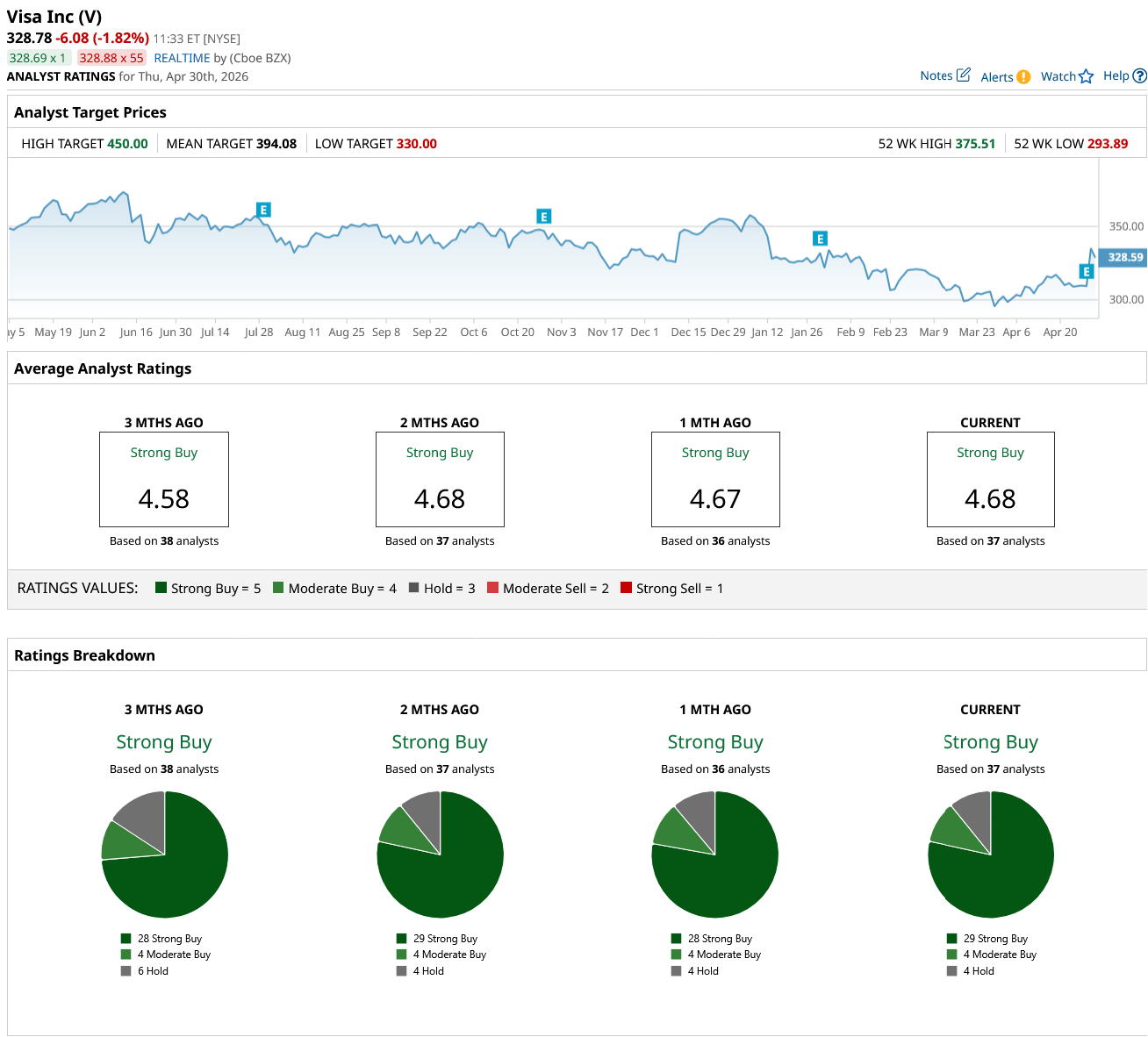

Visa remains a cornerstone of growth-oriented portfolios, bolstered by its massive $20 billion share buyback authorization, which signals immense management confidence. The stock currently maintains a consensus "Strong Buy" rating with a mean price target of $394.08, implying a significant 20% upside. Of the 37 analysts covering the stock, 29 have issued "Strong Buy" ratings, compared to only four "Hold" and four "Moderate Sell" ratings.

With its dominant "toll-booth" model and aggressive capital returns, Visa offers a compelling blend of defensive stability and double-digit earnings potential.

www.barchart.com

www.barchart.com On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A $20 Billion Reason to Buy Dividend-Paying Visa Stock Now SanDisk Stock Just Hit New Record Highs With Wall Street GLP-1 Sales Continue to Lift Eli Lilly. Does That Make LLY Stock a Buy? Western Digital Stock Has More Than Doubled YTD, but Bank of America Still Thinks You Should Buy Ahead of Earnings