Digital payments platform giant PayPal (PYPL) is contemplating making Venmo a standalone business unit. Venmo, with about 100 million users, is one of the biggest peer-to-peer payment networks in the United States. Consequently, as voices around a potential takeover of PayPal gather steam, the management is looking to extract the maximum value from one of its most valuable businesses.

According to the CNBC report, which broke the news, PayPal is searching for a digital banking executive who will head the Venmo segment.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About PayPal

Founded in 1998, PayPal's operations are simple. It provides a platform to allow customers to send/receive money digitally while also allowing merchants to accept payments online and offline. Its simplicity and reliability have led to it now operating in more than 200 countries and a total market cap of $45.8 billion.

However, a company that had Silicon Valley legends like Elon Musk and Peter Thiel in its founding has seen its shares lag in the last five years. Missed earnings and management upheavals over the years have seen its share price decline by close to 81% in the same period. In the relatively shorter term, PYPL stock is down 23% over the past year.

Now, as the present CEO, Enrique Lores, looks to arrest this decline, is PYPL stock worth owning? Let's find out.

www.barchart.com

www.barchart.com Q4 Miss Should Not Be Worrying

An objective look at PayPal's numbers would reveal why rivals are eyeing the San Jose, CA-based company. This is because even though its most recent results for Q4 2025 missed Street estimates on both the revenue and earnings front, PayPal remains a formidable player in the domain of digital payments, with decent growth rates.

For instance, over the past 10 years, PayPal's revenue and earnings have clocked CAGRs of 13.62% and 15.60%, respectively.

Moreover, in Q4, both revenue and earnings improved from the previous year. Net revenues increased by 4% year-over-year (YoY) to $8.7 billion, while total payment volumes rose by 9% over the same period to $475.1 billion. Along with this, payment transactions saw an uptick of 2%, to 6.8 billion. Overall, active accounts saw a growth of 1.1% over the past year to 439 million.

With all these key operating metrics growing, earnings rose 3% from the prior year to $1.23 per share. Although it missed the consensus estimate of $1.29 per share, this was just the second instance in the past nine quarters.

Net cash from operating activities for the quarter stood at $2.4 billion, unchanged from the previous year, as PayPal closed the year with a cash balance of about $8 billion. The company had no short-term debt on its books, alleviating any liquidity concerns.

Additionally, the company continued to buy back its own shares. In Q4 2025, PayPal bought shares worth $1.5 billion while declaring a dividend of $0.14 per share, paid to shareholders on March 25.

Notably, PYPL stock also continues to trade at undervalued levels currently. Its forward P/E, P/S, and P/CF of 9.61, 1.34, and 6.67 are all below the sector medians of 10.42, 2.88, and 11.52, respectively.

Why Is PayPal Struggling?

So, even amid strong numbers, a high brand recall value, and valuations that do not pinch, what is ailing PayPal? Well, there are a few reasons.

Notably, PayPal is navigating a more complicated competitive landscape than its market position alone might suggest. Lateral threats are multiplying, and the emergence of agentic AI in the shopping experience introduces a potentially disruptive force that could redefine where trust is established in the online transaction process. The concern is not purely theoretical, either, as branded checkout, the segment that commands the highest take rate within the business, is already showing signs of strain. Layer on top of that the broader trend toward commodification in payments, and the situation is ripe for a cap on growth rates.

The financial consequences are already reflected in the numbers. Flat momentum in branded checkout, combined with stronger growth in lower-margin business lines such as Enterprise Payments, Venmo, and debit card adoption, has pulled the overall transaction take rate down from 1.73% in Q4 2024 to 1.65% in Q4 2025. In response, the company has outlined a set of initiatives aimed at shoring up its branded checkout performance.

The primary focus falls on the roughly 25% of that segment represented by strategic large merchants, with plans to improve the experience through biometric authentication and passkey adoption, better positioning of the checkout button, and the introduction of enhanced rewards and loyalty features. The approach, however, reads as cautious at best, and the absence of any substantive discussion around AI as a tool for making the checkout experience more engaging and immersive was a notable omission.

That said, the broader picture is not all doom and gloom.

PayPal continues to hold a commanding position in global online payments, accounting for nearly half of the market as of 2026, a level of dominance that does not erode overnight. The aforementioned Venmo, which has been a consistent source of positive momentum, delivered revenue growth of 20% on a YoY basis in Q4 2025, with active accounts reaching 67 million and average revenue per active account climbing 14%. Total payment volume through the platform rose 13%, extending its streak of consecutive quarters with double-digit growth to five.

The BNPL offering added further substance to the growth narrative, generating more than $40 billion in total payment volume across 2025, representing YoY growth in excess of 20%. There is also a meaningful halo effect attached to its presence in the checkout flow, with data showing that the availability of the BNPL option lifts branded checkout volume by 10%. Taken together, these figures suggest that while the headwinds are real, the underlying business retains enough structural strength to keep the growth story alive.

Analyst Opinion on PYPL Stock

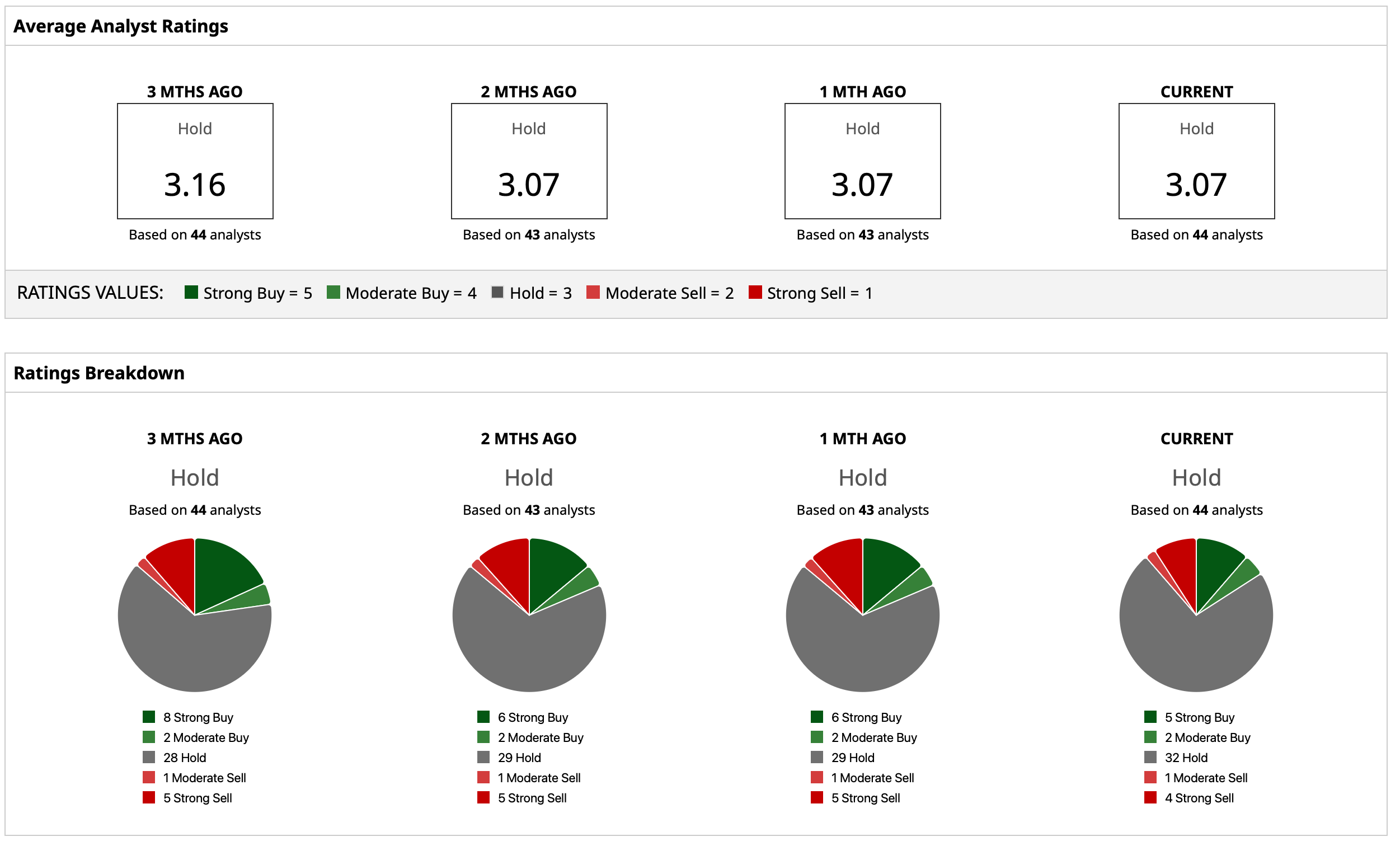

Thus, analysts have deemed PYPL stock a consensus “Hold,” with a mean target price of $51.26, which indicates limited upside potential from current levels. Out of 44 analysts covering the stock, five have a “Strong Buy” rating, two have a “Moderate Buy” rating, 32 have a “Hold” rating, one has a “Moderate Sell” rating, and four have a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

As PayPal Plans to Make Venmo a Standalone Business Unit, Should You Buy, Sell, or Hold PYPL Stock? Dear Unity Software Stock Fans, Mark Your Calendars for May 7 Eli Lilly Stock Popped on Earnings. America Can’t Get Enough of Its GLP-1s. These 3 Charts Look Like Thoroughbreds: Get Derby-Ready With My Racetrack-to-SPY Roadmap