In the tech boom of 2026, AI and chip stocks have been on a strong run. Companies like Nvidia (NVDA) and Meta Platforms (META) are seeing huge demand tied to AI. Even Tesla (TSLA) is getting attention for its chip work.

Arm Holdings (ARM) has also been a big winner amid these giants. That’s why ARM stock recently caught attention when Taiwan Semiconductor (TSM) sold its remaining stake in the company. On April 29, Taiwan Semiconductor said that it sold about 1.11 million shares worth around $231 million over two days. On the surface, that might sound like bad news, but the market didn’t see it that way.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

ARM stock barely reacted. In fact, shares moved about 1.5% higher after the news. Investors seem to think this was just routine portfolio management. Taiwan Semiconductor bought the shares before Arm’s intial public offering (IPO), and the two companies still work closely together.

More importantly, nothing changed in Arm's business. The sale was small compared to Arm's overall value, and its growth story in AI and chips remains the same. That’s likely why investors don't seem to be worrying much about the move.

How Is Arm Holdings Stock Performing?

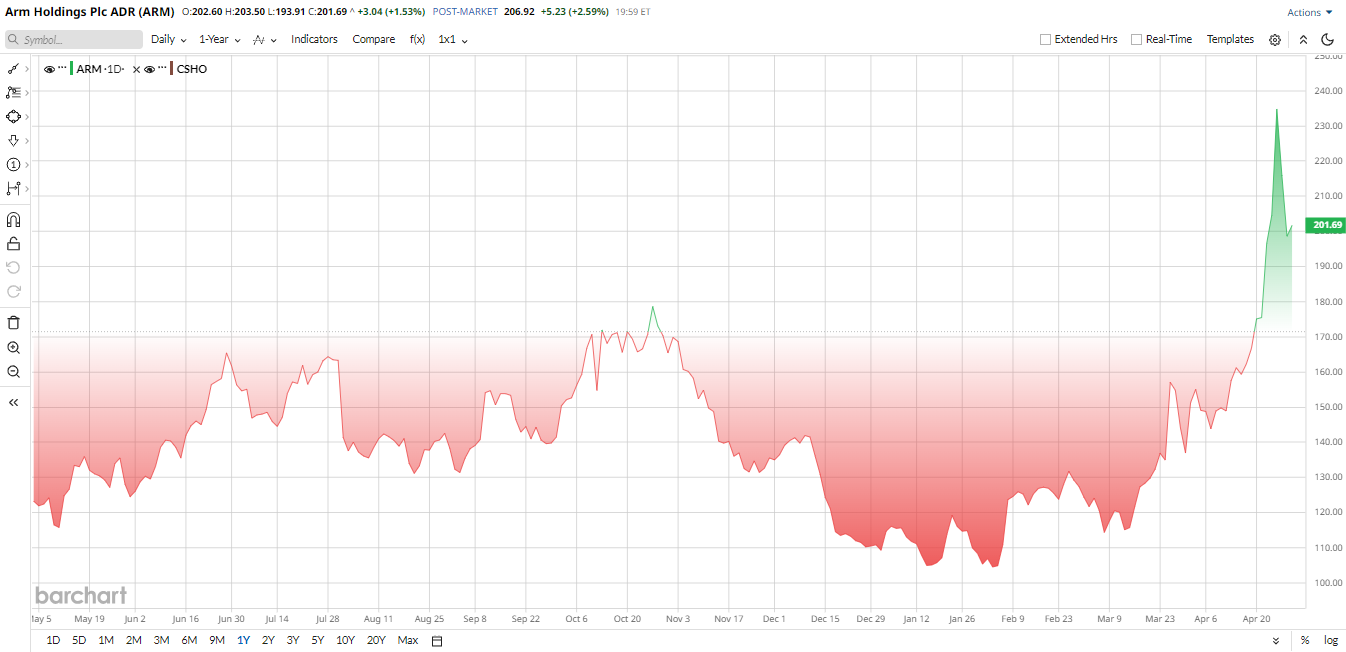

ARM stock has ripped higher over the past year, climbing roughly 83% in the past 52 weeks. In 2026 so far, shares have surged 93%. While last year saw a dip, this year’s rally has been steep, showing booming AI tailwinds, big licensing agreements, and optimism on new chip projects.

After the strong run, analysts warn that Arm that isn’t a bargain. Valuation metrics indicate a very expensive stock. The price-to-book ratio is 28.5 times, significantly higher than the sector median of 4.3 times, suggesting premium pricing. Similarly, the price-to-sales (P/S) ratio is 48.2 times, outpacing the sector median and reflecting a stretched valuation.

Still, while the valuation could be hard to justify with cold math, growth remains stellar with high double-digit revenue gains and near-unmatched profit margins.

www.barchart.com

www.barchart.com Arm Delivers Record Quarter on AI Strength

Arm Holdings just put up a strong quarter, and it’s clear the AI wave is helping.

For the period ended Dec. 31, 2025, revenue climbed 26% year-over-year (YOY) to about $1.24 billion. A big part of that came from royalties, which brought in around $737 million. Licensing added another $505 million. Both of these figures grew at a healthy mid-20% pace.

On the bottom line, things were a bit mixed. Net profit slipped slightly to $223 million. But looking at adjusted numbers, profit actually rose 10% to $457 million. Non-GAAP EPS came in at $0.43, beating expectations and climbing 10% from last year.

Cash is still in a good spot. Arm generated about $169 million in free cash flow and ended the quarter with roughly $3.54 billion in cash and short-term investments.

CEO Rene Haas said demand for AI is driving growth across cloud, edge, and industrial markets, and that showed up in the numbers. Looking ahead, the company expects about $1.47 billion in revenue next quarter, give or take $50 million, and around $0.58 per share in earnings. That suggests growth is still running strong.

For the full year, Wall Street is looking for roughly $4.85 billion in revenue and around $0.85 per share in earnings. So yes, Arm is riding the AI boom, but a lot of that optimism may already be baked into ARM stock

New AI Chips and Partnerships

Beyond earnings, Arm has been busy with major tech initiatives in 2026. The biggest splash was the “Arm AGI CPU,” Arm’s first in-house AI chip for data centers. In late March, the company announced partnerships with Meta and OpenAI to develop this new chip.

The idea is to handle power and memory limits in giant AI servers. “The biggest reason we’re doing this is that our partners have asked for it,” said Haas. In short, Arm is pivoting from just licensing designs to actually selling chips for AI systems.

Moreover, Arm also continues to roll out updates to its designs, the recent Armv9 and Compute Subsystem technologies, and expand in fields like automotive AI and telecom infrastructure.

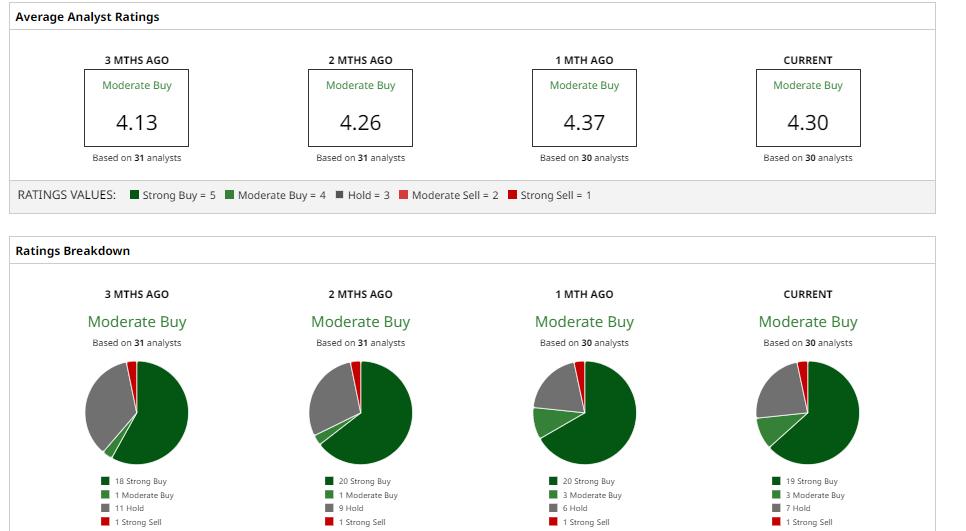

What Do Analysts Say About ARM Stock?

Wall Street’s view on Arm Holdings is a bit mixed right now. On the one hand, some analysts are still very bullish. Wells Fargo recently kept its “Overweight” rating and raised its price target to $220 from $175, pointing out that ARM stock has jumped significantly since earnings and saying that the AI trend supports long-term growth. Other firms also remain positive. Mizuho raised its target to $230, while UBS has a $175 price target, highlighting Arm’s growing role in AI and data centers.

But not everyone is as confident. Morgan Stanley has an “Equal Weight" rating on ARM stock. The firm's concern is that Arm is moving more into selling chips, which could bring execution risks in the near term.

Overall, based on 30 analysts with coverage, ARM stock has a “Moderate Buy” consensus rating with an average price target of $180.67. That suggests potential downside of around 15% from current levels. Meanwhile, the Street-high price target of $240 suggests potential upside of 14% from here.

For investors, the bottom line is that, even after Taiwan Semiconductor's stake sale, Arm remains strong. The company is clearly benefiting from AI demand and new growth areas, but ARM stock is already priced for big expectations. What happens next will depend on execution, especially around the firm's AI strategy and upcoming earnings.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

FS KKR Corp, a Private Credit Fund, Sports a 16.6% Yield - Is FSK A Value Buy? Taiwan Semi Just Dumped Its Stake in ARM Stock. Why Investors Don’t Seem to Care. Amazon Stock Forecast: Could AI and Chips Make AMZN a $4 Trillion Company? Option Volatility And Earnings Report For May 4 - 8