Disney (DIS) released its fiscal Q2 2026 earnings yesterday, May 6, before the markets opened. It was the first earnings report under the incoming CEO Josh D’Amaro, who took over the baton from Bob Iger. The earnings came in ahead of estimates, and DIS stock rose over 7.5% yesterday. In the shareholder letter, D’Amaro listed a long-term vision of Disney alongside providing guidance for the current and the next fiscal year.

www.barchart.com

www.barchart.com Disney’s Turnaround Is a Work In Progress

This is the second leadership change at Disney in less than four years. In November 2022, Disney appointed Bob Iger as the CEO, who returned from retirement to lead the company again. While the news triggered an initial buying spree in DIS, the stock continued to underperform under his watch.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

To be sure, Iger handed over Disney in a much better position to his successor than he inherited in 2022. Among others, Disney chased streaming profitability under Iger while giving up the company’s obsession with subscriber growth. He also aggressively cut costs and put creativity at the core of Disney’s business, while shifting the focus from quantity to quality in the movie business. Thanks to these efforts, Disney’s streaming business has turned profitable, and the company was the top-grossing studio in 2024 and 2025.

D’Amaro Lays Out His Vision for Disney

Now, D’Amaro has laid out his strategic vision for the company, which has three pillars, as follows:

Investing in IP: Disney would continue to invest in intellectual property (IP), which makes sense as strong IP has been the company’s core strength. The value of IP cannot be understated, given the kind of money Paramount Skydance (PSKY) is shelling out for Warner Bros. Discovery’s (WBD) assets—a deal Netflix (NFLX) walked away from. D’Amaro added that the company will focus on expanding Disney+ globally and pointed to the success of local originals. Increasing Engagement and Reach: D’Amaro intends to evolve Disney+ from a simple streaming service into a central hub for the entire company. The platform will act as the connective tissue between streaming, sports, video games, and the theme parks. In the letter, he said, “We are focused on making the platform more engaging, more personalized, and more central to how fans experience our brands.” He added that the company would also work towards increasing engagement and reach in areas that are currently not major revenue drivers, such as games. Better Monetization: D’Amaro listed improving monetization as the third pillar. The goal is to ensure that success in one area—such as a hit film—compounds into value elsewhere, whether that’s a new cruise ship theme, a video game expansion, or a themed land in a park. He also listed capital-light initiatives, such as the upcoming theme park in the UAE and a cruise ship in Japan, for which Disney has roped in local partners. D’Amaro sees artificial intelligence (AI) as a “meaningful long-term opportunity” that would play a role in five aspects of its business: “content creation and production, monetization, workforce productivity, guest and consumer experiences, and enterprise operations.” He, however, stressed that the company will implement AI “in a way that keeps human creativity at the center of everything we do.”DIS Stock Forecast

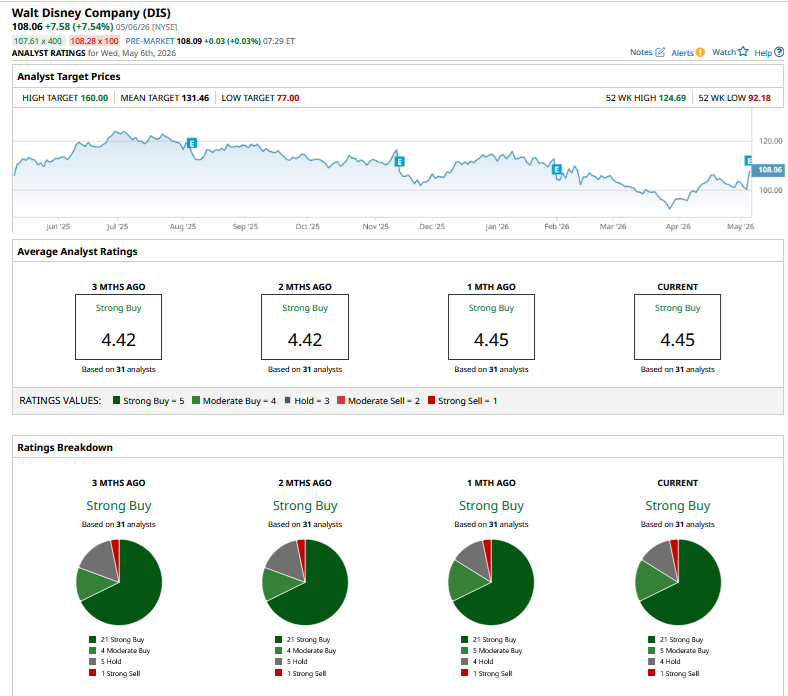

After Disney’s fiscal Q2 earnings release, Guggenheim raised the stock’s target price from $115 to $120, while Goldman Sachs raised its from $151 to $164. More brokerages might follow suit, and we should see target price revisions following an impressive earnings report. Currently, Disney has a consensus rating of "Strong Buy" from the 31 analysts polled by Barchart, while its mean target price is $131.46.

www.barchart.com

www.barchart.com Should You Buy Disney Stock?

In my previous article, I noted that while Disney faces some challenges, these appear priced in, and the stock appears to be a good buy. I remain bullish on Disney following the earnings report, given the short- and long-term forecasts D’Amaro outlined.

From a valuation perspective, Disney trades at a forward price-to-earnings (P/E) multiple of just over 15x, which I find quite attractive considering the 12% earnings growth that the company expects to deliver this fiscal year and “double-digit” growth in the next. Given the improvement in its streaming business, I believe Disney has the potential to deliver structural double-digit annualized earnings growth over the medium to long term.

Overall, I remain invested in DIS and continue to believe that the stock is currently underpriced by the market. The company faces some risks, such as the deterioration in global macros due to the spike in energy prices, immigration-related issues in the U.S., and the structural decline in linear TV. However, given the cheap valuations, Disney's risk-reward appears favorable at current prices.

On the date of publication, Mohit Oberoi had a position in: DIS , NFLX . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Josh D’Amaro Has a ‘Vision’ for Disney. That Makes DIS Stock a Buy Here. Palantir Stock: Bulls and Bears are Divided, But Its AI Growth Is Hard to Ignore BA Stock Alert: What to Expect as Boeing CEO Joins Trump on China Trip If You Want to Know How Much Inflation Has Really Hurt U.S. Consumers, Skip the CPI and Study Big Mac Burger Prices