CION Investment Corp. CION is moving through 2026 in a private-credit market that is active, but not easy. Competition is keeping spreads tight at the same time leverage is rising and lender protections are loosening. That mix can lift activity while still limiting incremental returns.

Against that backdrop, investors will likely focus on how CION converts better deal flow into durable income and net asset value, without letting credit costs or funding constraints erode the math.

CION Sees Private Credit Competition Keep Spreads Tight

Private credit remains intensely competitive, and that is showing up in tighter spreads, elevated leverage, and looser lender protections. Management has also pointed to a disconnect between new-issue and secondary conditions, with new-issue pricing influenced by heavy fundraising that can keep spreads compressed.

For company like CION, this structure can restrain portfolio expansion and incremental returns even when headline deal flow improves. Maintaining discipline around pricing, structure, and documentation can be a necessary defence, but it can also moderate near-term growth and returns on equity in a market where borrowers have more negotiating leverage.

CION Investment M&A Activity Lifts Deal Flow

Deal activity has been improving as the mergers and acquisitions (M&As) backdrop strengthens and macroeconomic clarity improves following earlier tariff-related uncertainty. As market sentiment recovered, transaction activity began to accelerate, setting a more constructive environment for middle-market lending.

CION’s first-quarter 2026 activity provides tangible evidence of a more active lending backdrop. New investment commitments were $69 million, with $54 million funded, and net funded investment activity increased by $28 million. If that momentum continues, originations can rise and support total investment income, even if pricing remains competitive.

CION Balancing Growth With Risk Ratings and Non-Accruals

CION is pairing growth ambitions with a defensive posture. The portfolio remains heavily first-lien, with 80.8% in senior secured first-lien investments. Importantly, about 98% of the portfolio is risk rated 3 or better, suggesting management has been selective about underwriting quality while competing for deals.

The key watch item is non-accrual behavior, given the recent pattern of volatility. Non-accruals declined modestly in first-quarter 2026, but they rose sharply across the second, third, and fourth quarters of 2025. In first-quarter 2026, non-accruals were 1.53% of fair value and 5.35% at amortized cost, compared with 1.78% and 4.32% in the fourth quarter of 2025. In a market with tighter spreads and higher leverage, preserving credit quality is central to protecting dividend coverage and net asset value.

CION Investment Leverage Plans and Funding Mix

In a competitive market, funding structure can shape flexibility as much as origination volume. CION’s debt mix has been weighted toward unsecured borrowings, with 75% unsecured and 25% bank debt, alongside net debt-to-equity leverage of 1.62x. The company also reported $106 million in available liquidity in the first quarter.

Management has stated an intent to reduce leverage over the next few quarters. If achieved through repayments and refinancing activity, that could improve balance-sheet capacity for new investments and capital returns. With CION already paying monthly base distributions starting January 2026 and executing share repurchases, incremental balance-sheet flexibility could matter if spreads stay tight and underwriting standards remain contested.

CION Macro and Regulatory Limits on Capital Access

Even with a healthier origination environment, capital access is not guaranteed. Regulatory constraints amid a challenging macro backdrop may limit CION’s accessibility to capital markets and raise funding costs. Those pressures can cap growth by making incremental liabilities more expensive, reducing the economic benefit of new originations in a compressed-spread market.

This is also where scale and market access can influence competitive dynamics. Larger business development company peers such as Ares Capital Corporation ARCC and Main Street Capital Corporation MAIN remain prominent participants in middle-market credit, and intense competition across platforms can reinforce the tight-spread reality for lenders seeking attractive risk-adjusted returns.

CION Scenarios for Income and NAV in 2026

In 2026, the range of outcomes for CION’s income and net asset value will likely hinge on whether stronger deal flow can overcome a still-competitive pricing backdrop.

In an upside case, originations keep rising as transaction activity improves and funding converts into earning assets. If the company sustains its recent expense discipline, including lower advisory and incentive fees, incremental volume can translate more cleanly into steadier net investment income.

The downside case is centered on credit. If non-accruals move higher again, credit marks could pressure net asset value, especially if borrower cash flows soften or spreads fail to compensate for added risk. A renewed increase in non-accruals would likely lift credit costs and test dividend coverage, while broader credit headlines could weigh on secondary marks and exit timing.

For investors, the checklist stays straightforward: the trajectory of total investment income, the direction of non-accruals, and whether the declining expense trend holds, particularly the advisory and incentive fee components that have been supporting lower costs.

CION carries a Zacks Rank #3 (Hold). A base case aligns with that profile, where tight spreads limit incremental returns, but disciplined underwriting and balance-sheet management help stabilize income and net asset value. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

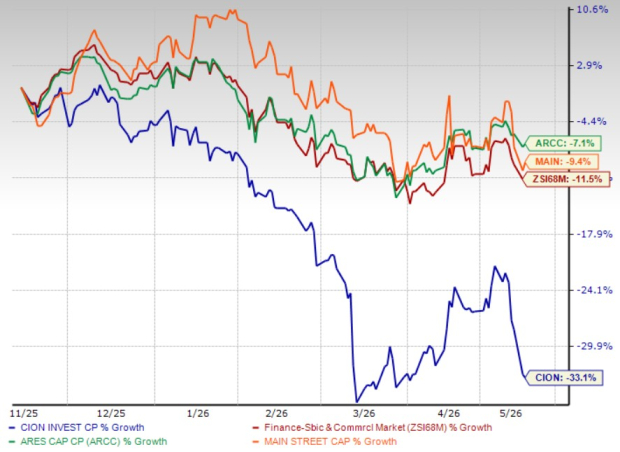

Over the past six months, CION shares fell 33.1% compared with the industry’s decline of 11.5%. Its peers, Ares Capital and Main Street Capital declined 7.1% and 9.4%, respectively.

Price Performance

Image Source: Zacks Investment Research

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ares Capital Corporation (ARCC): Free Stock Analysis Report

Main Street Capital Corporation (MAIN): Free Stock Analysis Report

CION Investment Corporation (CION): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).