On its first-quarter 2026 conference call held on May 5, Pfizer PFE CEO Albert Bourla said the company expects a high single-digit 5-year revenue CAGR starting from 2029. In 2025, Pfizer’s revenues fell 2% to $62.6 billion due to a decline in revenues from its COVID-19 products, BioNTech BNTX-partnered Comirnaty and Paxlovid. In 2026, Pfizer expects total revenues to be between $59.5 billion and $62.5 billion. The range represents a decline from 2025 revenues due to lower revenues from COVID products and a loss of revenues from the upcoming patent cliff.

Pfizer expects a significant negative impact on revenues from loss of exclusivity (“LOE”) in the 2026-2030 period as several of its key products, including Bristol-Myers BMY-partnered Eliquis, Ibrance, Xeljanz and Xtandi, face patent expirations. The LOE cliff is expected to hurt sales by approximately $1.5 billion in 2026.

With Pfizer’s 2026 sales guidance pointing to only modest growth, investors may question how the company expects to return to high single-digit revenue growth beginning in 2029.

Pfizer expects the growth to be driven by its advancing R&D pipeline and the continued progress of new and acquired products. Pfizer's recently launched and acquired products delivered revenues of $3.1 billion in the first quarter, rising 22% on a year-over-year basis. In 2026, Pfizer expects its recently launched and acquired products to record continued double-digit growth.

Pfizer’s key recent product launches contributing to sales growth include the RSV vaccine, Abrysvo and Elrexfio, a BCMA-CD3-targeted bispecific antibody for relapsed or refractory multiple myeloma, among others. Key products added through recent acquisitions that are supporting top-line growth include Nurtec ODT and Padcev. While Nurtec was added through Pfizer’s 2022 acquisition of Biohaven, Padcev came through the acquisition of Seagen in 2023.

Pfizer has also strengthened its R&D pipeline, which includes both internally discovered programs as well as innovative candidates added through acquisitions. The November 2025 acquisition of obesity drugmaker, Metsera, has added four novel clinical-stage incretin and amylin programs, which are expected to generate billions of dollars in peak sales. Pfizer is on track to start 20 pivotal studies in 2026, including 10 pivotal studies for the ultra-long-acting obesity candidates added from the Metsera acquisition and four for PF-08634404, a dual PD-1/VEGF inhibitor in-licensed from Chinese biotech 3SBio in 2025.

The company also expects its recent patent settlement agreements related to its key drug, Vyndamax, to significantly improve its post-2028 growth outlook and strengthen confidence in achieving its targeted high single-digit revenue CAGR after 2029.

In April, Pfizer reached settlement agreements with Dexcel Pharma, Hikma Pharmaceuticals and Cipla Ltd in patent litigation related to Vyndamax, extending the drug’s effective U.S. patent expiry date to June 1, 2031, subject to other ongoing litigation. The settlement is expected to help Pfizer maintain relatively stable U.S. revenues from Vyndamax from 2028 through mid-2031, instead of the previously anticipated decline beginning in 2029.

Pfizer expects its recently launched and acquired products, along with a strengthening pipeline, to help revive top-line growth toward the end of the decade. At the same time, while managing near-term LOE headwinds, the company is working to build a foundation for sustainable long-term value creation.

PFE’s Price Performance, Valuation and Estimates

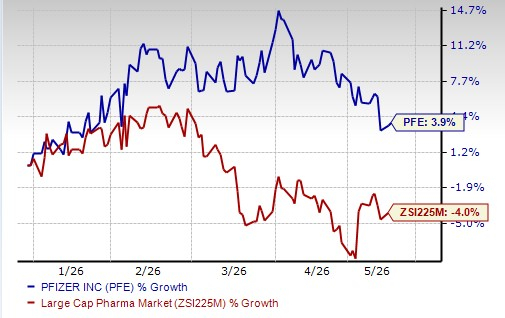

Pfizer’s stock has risen 3.9% so far this year against a decline of 4.0% for the industry.

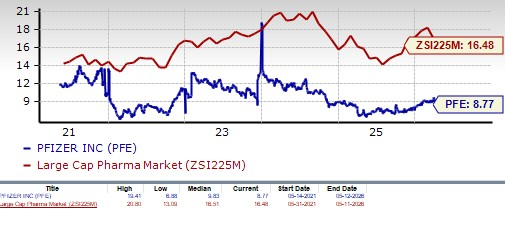

From a valuation standpoint, Pfizer appears attractive relative to the industry and is trading below its five-year mean. Going by the price/earnings ratio, Pfizer’s shares currently trade at 8.77 forward earnings, significantly lower than 16.48 for the industry as well as the stock’s five-year mean of 9.83.

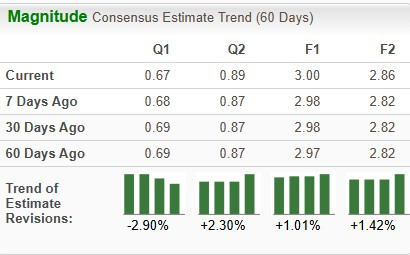

The Zacks Consensus Estimate for 2026 earnings per share has risen from $2.98 to $3.00, while that for 2027 has risen from $2.82 to $2.86 over the past 30 days.

Pfizer has a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bristol Myers Squibb Company (BMY): Free Stock Analysis Report

Pfizer Inc. (PFE): Free Stock Analysis Report

BioNTech SE Sponsored ADR (BNTX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).