For years, investors viewed Apple (AAPL) as a hardware powerhouse driven by blockbuster iPhone cycles. But increasingly, Wall Street believes the company’s future earnings engine may come not from devices alone, but from the rapidly expanding ecosystem wrapped around them. That shift is now at the center of a bullish new thesis from Evercore ISI, whose analysts argue Apple’s high-margin Services business could help propel earnings per share to as high as $13 over time.

The firm recently raised its price target on Apple stock to $365 while maintaining an “Outperform” rating, citing the company’s growing ability to monetize its massive installed base of more than 2.5 billion active devices through subscriptions, payments, cloud services, advertising, licensing, and artificial intelligence (AI)-driven offerings. Evercore believes investors remain too focused on near-term iPhone demand fluctuations while underestimating the long-term earnings power embedded within Apple’s Services segment.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The bullish argument stems from the fact that services revenue carries substantially higher margins than hardware. As recurring revenue streams like iCloud, Apple Music, AppleCare, Apple Pay, and App Store monetization continue to scale, Apple’s profitability could expand even if overall device unit growth moderates. Evercore estimates the company can sustain EPS growth driven by this mix shift toward Services, premium device pricing, and future AI monetization opportunities.

Does this shift make the stock an attractive buy now?

About Apple Stock

Based in California, Apple stands as a forward-looking company and a worldwide leader in hardware, software, and services. Its portfolio spans iconic devices like the iPhone, iPad, Mac, and Apple Watch, alongside widely used platforms such as the App Store, iCloud, Apple Music, and Apple TV+. The company currently boasts a market cap of $4.4 trillion and a Magnificent Seven status.

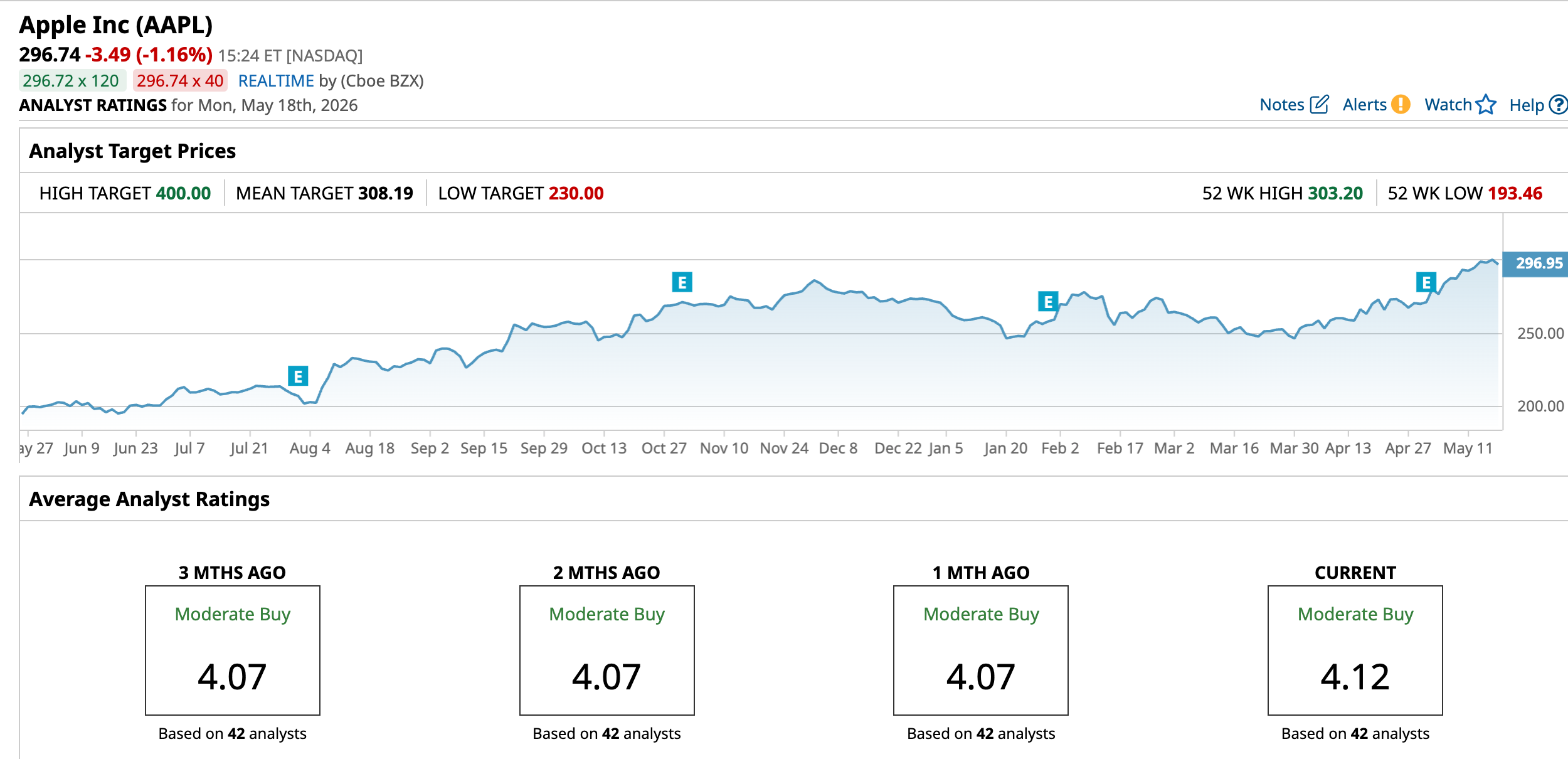

Shares of Apple have delivered a strong performance over the past year, reflecting renewed investor optimism around the company’s Services expansion, AI monetization opportunities, and resilient ecosystem strength. The stock closed at $300.23 on May 15, with a fresh 52-week high during the session of $303.20.

Year-to-date (YTD), Apple stock has gained 9.31%. Over the past 12 months, the stock has surged 40.67%, driven by accelerating earnings growth, expanding high-margin Services revenue, and growing enthusiasm surrounding Apple’s AI roadmap.

The rally pushed Apple’s market value to the $4.4 trillion mark, reinforcing its position as one of the world’s most valuable companies. Importantly, the stock’s breakout to a new 52-week high on May 15 signals continued bullish momentum as Wall Street increasingly focuses on Apple’s long-term earnings power rather than near-term iPhone upgrade cycles.

www.barchart.com

www.barchart.com The stock trades at a premium at 34.11 times forward earnings, compared to the sector median and its historical average.

Q2 Results Exceeded Expectations

AAPL reported exceptionally strong fiscal second-quarter 2026 results on April 30, delivering record March-quarter revenue, earnings, and iPhone sales as accelerating Services growth and strong demand for the iPhone 17 lineup boosted profitability across the business.

The company generated revenue of $111.2 billion during the quarter ended March 28, representing a 17% year-over-year (YOY) increase, while earnings per share climbed 22% YOY to $2.01, exceeding expectations. Net income rose to $29.6 billion compared with $24.8 billion a year earlier.

Operational performance remained strong across nearly every business segment. iPhone revenue surged 22% YOY to $57 billion, driven by robust global demand for the iPhone 17 family and record upgrade activity. Management noted that iPhone achieved March-quarter revenue records.

Services revenue reached a new all-time high of $31 billion, increasing 16% YOY as App Store, cloud, subscriptions, payments, advertising, and media businesses continued to expand. Importantly, Services now account for a significant portion of total company revenue, highlighting Apple’s increasing transition toward recurring high-margin revenue streams.

The Mac business generated $8.4 billion in revenue, up 6% YOY, while iPad revenue rose 8% YOY to $6.9 billion, and Wearables, Home and Accessories revenue increased 5% to $7.9 billion.

Profitability improved meaningfully during the quarter despite ongoing supply-chain and memory-cost pressures. Gross margin expanded to 49.3%. Moreover, services gross margin reached an exceptionally strong 76.7%, while Products gross margin stood at 38.7%.

Geographically, Apple delivered double-digit growth across every major region, including a sharp rebound in Greater China and continued acceleration in emerging markets such as India and Mexico.

Furthermore, management issued bullish guidance for fiscal third quarter 2026, forecasting revenue growth of approximately 14% to 17% YOY despite ongoing supply constraints tied to advanced semiconductor availability and rising memory costs.

Apple also projected gross margins between 47.5% and 48.5% while expecting Services revenue growth to remain comparable to Q2 levels. The guidance signaled confidence that strong ecosystem demand, AI-driven device adoption, and continued Services expansion will continue supporting earnings growth through the remainder of 2026.

In addition, the consensus estimate of $8.74 for fiscal 2026 indicates an increase of 17.2% YOY, before improving by around 9.2% annually to $9.54 in fiscal 2027.

What Do Analysts Expect for Apple Stock?

In addition to Evercore, Bernstein SocGen Group also raised its price target on AAPL to $350 from $340 while reiterating an “Outperform” rating following Apple’s strong fiscal second-quarter results and upbeat guidance.

Also, Goldman Sachs maintained a “Buy’ rating and $340 price target on AAPL this month.

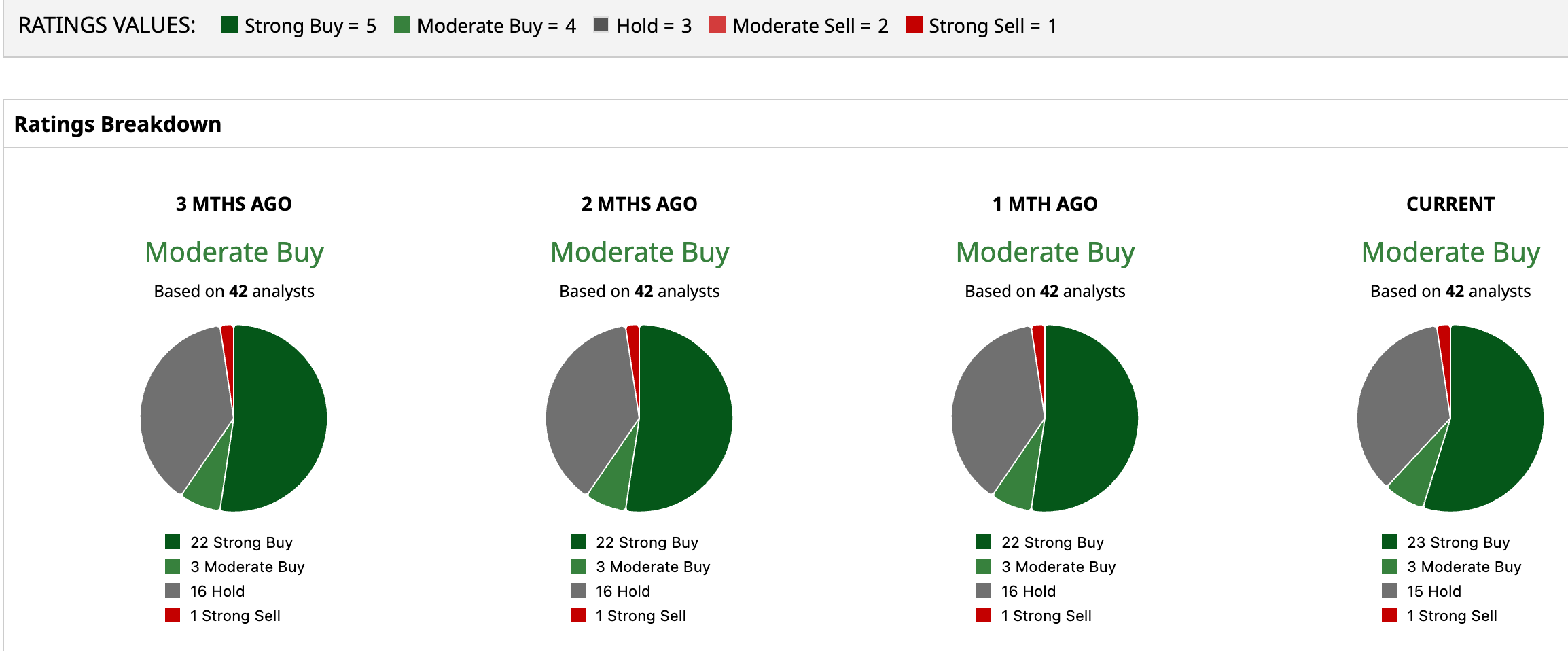

Overall, Apple stock has a consensus “Moderate Buy” rating. Out of 42 analysts covering the tech giant, 23 recommend a “Strong Buy,” three give a “Moderate Buy,” 15 analysts stay cautious with a “Hold” rating, and one has a “Strong Sell” rating.

While the average analyst price target of $308.19 suggests an upside of 3.85%, the Street-high target price of $400 suggests as much as 34.8% upside ahead.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Lumentum Stock Is Up 163% in 2026. Tiger Global Added a New Stake in Q1. Regeneron Sinks 10% on Failed Phase 3 Melanoma Trial. What Comes Next for REGN Stock. How Services Could Help Generate $13 in Earnings Per Share for Apple Stock NextEra Energy to Buy Dominion in $67 Million Deal. What It Means for D Stock.