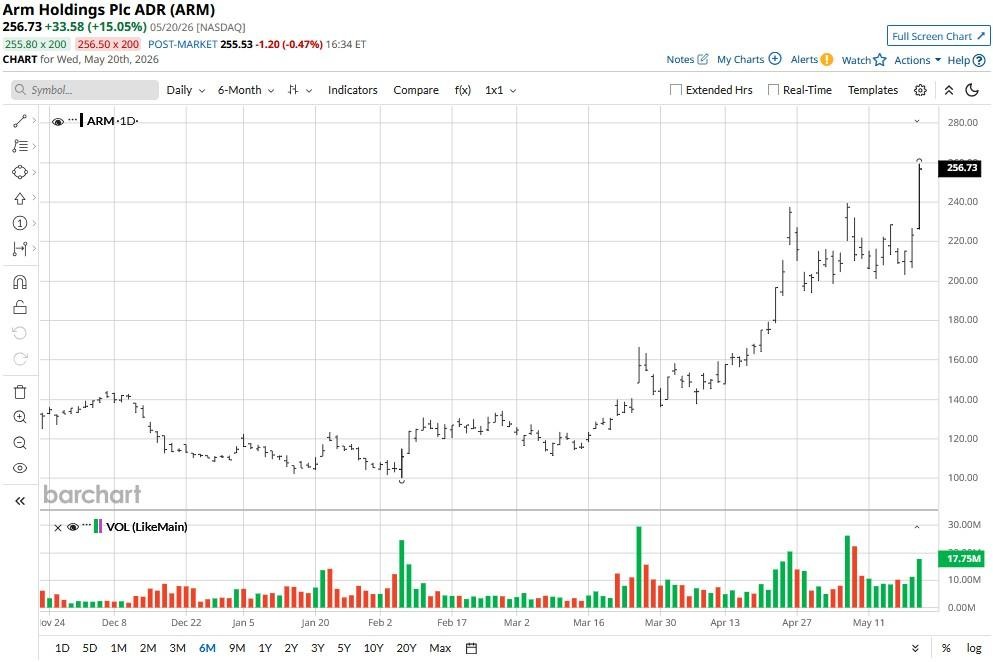

Arm Holdings (ARM) shares rallied on Wednesday after Bernstein initiated coverage on the British chip designer with an “Outperform” rating and a rather bold $300 price target.

The upward momentum drove ARM’s relative strength index (RSI) into the late 60s, signaling the stock is now approaching overbought territory, which often triggers a near-term pullback.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Arm stock’s performance in 2026 has been nothing short of blockbuster. As of writing, it’s trading up more than 120% year-to-date.

www.barchart.com

www.barchart.comWhat Prompted the Bullish Note on Arm Stock?

Bernstein analyst David Dai framed Arm as being at the center of a CPU renaissance, arguing that the structural transition from traditional LLMs to fully autonomous AI agents requires dramatically higher localized computing intelligence that plays directly into Arm’s architectural strengths.

The company’s quarterly results provided the fundamental catalyst for this rerating. Arm reported $1.49 billion in revenue, with licensing sales growing 29% year-over-year.

Most importantly, data center royalty revenue more than doubled year over year, underscoring its successful penetration into the lucrative server market – and making ARM shares more attractive to own in 2026.

Here’s Why ARM Shares Aren’t Out of Juice Just Yet

The bull case on Arm shares centers on the company’s transition from a pure intellectual property licensor into what Dai characterizes as an indispensable component of the hyperscaler ecosystem.

Major cloud providers, including Alphabet's (GOOG) (GOOGL) Google, Microsoft (MSFT), and Meta Platforms (META), are consistently choosing custom Arm-based silicon over traditional x86 architecture to optimize thermal efficiency as well as computing density.

Arm’s launch of its own AGI processor for data centers has transformed the narrative from royalty collector to artificial intelligence infrastructure principal.

Customer commitments for that CPU jumped from $1 billion to over $2 billion across fiscal years 2027 and 2028 in just six weeks, providing a multi-billion-dollar backlog that de-risks near-term revenue projections.

Bernstein highlighted that data center chips command materially higher royalty rates per unit than legacy mobile processors, meaning the mix shift should drive exponential operating leverage as these premium deployments reach scale.

How Wall Street Recommends Playing Arm Holdings

Note that Bernstein isn’t the only Wall Street firm keeping bullish on ARM stock for the next 12 months.

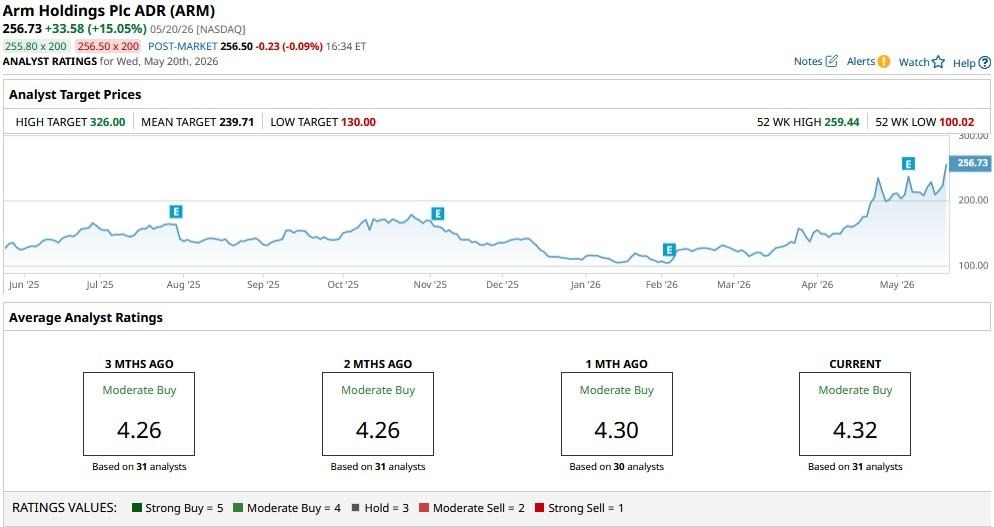

The consensus rating on Arm Holdings sits at “Moderate Buy” with price objectives as high as $326, indicating potential upside of nearly 30% from here.

www.barchart.com

www.barchart.comThis article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Arm Surges on New $300 Price Target: ARM Stock Is at the ‘Center of the Renaissance’ in CPUs Massive Layoffs at Meta Platforms Are Now Underway. What That Means for META Stock. Stifel Just Raised Its Price Target on Palo Alto Networks. Here's Why. BBBY Stock Alert: Why Bed Bath & Beyond Is Rising After a Social Media Post