Cisco Systems CSCO is benefiting from an accelerating demand for AI infrastructure and enterprise networking modernization, which drove fiscal third-quarter 2026 results. The company reported record quarterly revenues of $15.8 billion, up 12% year over year, while product revenues increased 17% year over year to $12.1 billion. Networking remained the primary growth engine, with networking product revenues rising 25%, fueled by AI infrastructure deployments and campus networking refresh cycles.

Cisco’s networking product orders grew more than 50% year over year in the fiscal third quarter, marking the seventh consecutive quarter of double-digit growth. Demand remained broad-based across service provider routing, data center switching, campus switching, wireless, enterprise routing and industrial IoT products. Enterprise product orders increased 18%, while service provider and cloud orders surged 105%, supported by triple-digit growth from five major hyperscalers. The telecom customers are also investing heavily in Cisco technology to prepare networks for AI-driven traffic growth.

The company is seeing particularly strong traction in AI infrastructure. AI infrastructure orders from hyperscalers reached $1.9 billion in the quarter compared with $600 million a year ago. It is noteworthy that fiscal 2026 AI infrastructure orders from hyperscalers are now expected to reach approximately $9 billion, significantly above the prior $5 billion target. The company highlighted strong adoption of Silicon One systems and Acacia optics, with the Acacia business on track to grow more than 200% year over year in fiscal 2026.

Cisco is also gaining from accelerating enterprise campus modernization trends. Campus networking orders rose more than 25% year over year, while wireless orders jumped over 40%. The company mentioned that Wi-Fi 7 products accounted for nearly half of the wireless mix during the quarter. Enterprises are upgrading networks to support AI inferencing, agentic AI applications and growing cybersecurity requirements, creating a multiyear refresh opportunity.

Cisco expects AI networking demand to remain strong across hyperscalers, enterprises and telecom customers. It is noteworthy that enterprise data center switching orders increased more than 40%, while Nexus switch orders tied to AI deployments rose almost 50% sequentially. With expanding adoption of Silicon One, AI-native networking products and secure infrastructure solutions, Cisco appears well positioned to benefit from the ongoing AI networking boom.

CSCO Faces Tough Competition in the Networking Domain

Cisco is facing stiff competition from Arista Networks ANET and Hewlett-Packard HPE in the networking domain.

Arista Networks holds a leadership position in 100-gigabit Ethernet switches and is increasingly gaining market traction in 200 and 400-gigabit high-performance switching products. ANET’s advanced cloud-native software and smart Wi-Fi solutions deliver intelligent application identification, automated troubleshooting and location services. These solutions efficiently support apps like Teams, Zoom and Google Meet. The Arista 2.0 strategy is resonating well with customers, as its modern networking platforms are foundational to the transformation from silos to data centers.

Hewlett Packard Enterprise views AI, Industrial Internet of Things (IoT) and distributed computing as the next major markets. The acquisition of Juniper Networks has elevated Hewlett Packard Enterprise’s competitive stance by expanding its networking domain in AI, cloud and hybrid solutions. Its multi-billion-dollar investment plan for expanding networking capabilities will diversify the business from the server and hardware storage markets and boost margins in the long run.

CSCO Share Price Performance, Valuation & Estimates

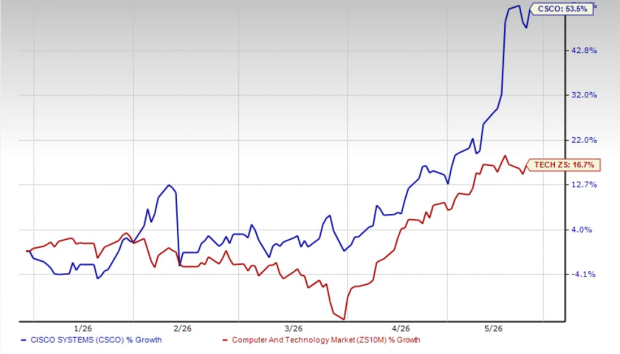

Cisco shares have gained 53.5% in the year-to-date period, outperforming the broader Zacks Computer and Technology sector’s return of 16.7%.

CSCO Stock Outperforms Sector

Image Source: Zacks Investment Research

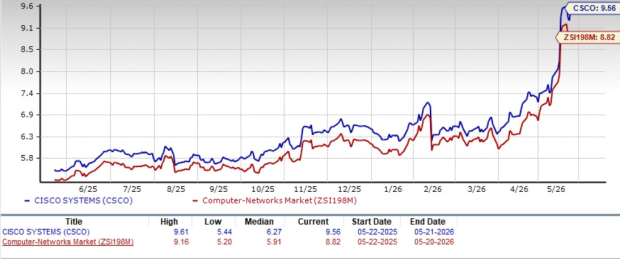

CSCO stock is trading at a premium, with a trailing 12-month price/book of 9.56X compared with the Zacks Computer Networking industry’s 8.82X. Cisco has a Value Score of F.

CSCO Stock Is Overvalued

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for fourth-quarter fiscal 2026 earnings is currently pegged at $1.09 per share, up by a penny over the past 30 days, suggesting 10.1% growth from the figure reported in the year-ago quarter.

Cisco currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Arista Networks, Inc. (ANET): Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).