“The world has entered the age of electricity,” as the International Energy Agency’s Fatih Birol recently stated, and that shows up clearly in the enormous amounts of power now used by modern data centers. Consequently, spending on technology and AI‑driven infrastructure is tracking to climb above 2% of global GDP, topping past build‑outs like interstate highways and early broadband networks.

Applied Digital is right in the middle of this “electrified” AI build‑out. The company just signed a 15‑year, multi‑billion‑dollar lease with an investment‑grade U.S. hyperscaler for its new Polaris Forge 3 campus, adding another big, take‑or‑pay deal. After that news, Needham raised its price target on Applied Digital Corporation (APLD) to $66 from $51, seeing Polaris Forge 3 as a real boost to the company’s long‑term earning power.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

This mix of locked‑in revenue, a top‑tier customer, and a higher target from a major research firm could be a real turning point for the stock. The key question now is whether this is the start of a steady rerating higher or the late stage of a hot run driven by excitement and heavy spending.

Applied Digital’s Numbers

Applied Digital is a Dallas‑based company that designs, builds, and runs high‑performance data centers, focusing on campuses built for large cloud and hyperscale customers, including its growing Polaris Forge sites.

Their stock has climbed 87.07% so far this year and delivered a huge 513.24% gain over the past 12 months.

www.barchart.com

www.barchart.com This kind of move now comes with a rich price tag. Applied Digital is valued at $13.12 billion, with the shares trading at 37.34 times trailing sales compared with a sector median of 3.83 times, and at 8.28 times book value versus the sector benchmark of 4.18 times.

APLD’s latest numbers, from its third‑quarter fiscal 2026 results released on Feb. 26, showed revenue of $126.6 million, up 139% from the same period a year earlier.

Their net loss attributable to common stockholders came in at $100.9 million, a 179% deterioration from the prior year, which shows how expensive this build‑out phase still is. This worked out to a net loss of $0.36 per basic and diluted share, down 125% year-over-year (YOY), and it was a clear reminder that growth is coming with real short‑term pressure on the bottom line.

The adjusted figures paint a more encouraging picture. They reported adjusted revenue of $108.6 million and adjusted net income of $33.2 million, or $0.09 per diluted share.

This is backed by adjusted EBITDA of $44.1 million, which shows that the underlying operations tied to its contracted infrastructure are already generating positive earnings even while reported results absorb high upfront costs.

How Polaris Forge 3 Fits Into APLD’s Bigger Growth

The 15‑year lease at Polaris Forge 3 is the latest step in a steady build‑out of its data center business. The company recently said this new hyperscaler deal at its fourth campus pushed total contracted capacity above 1 GW. It also lifted baseline contracted lease revenue to about $31 billion, and that figure could reach as much as $73 billion if customers use all renewal options across roughly 1.2 GW of IT capacity.

Funding that kind of growth has taken real work on the balance sheet. The company earlier priced $2.15 billion of senior secured notes to fund development at the Polaris Forge 2 campus. That financing locked in capital for a major build and showed lenders are willing to back APLD’s long‑term lease model.

A separate $300 million senior secured bridge facility added extra liquidity. It gave the company room to manage construction and lease ramp‑up without constantly going back to equity investors.

Demand has been building alongside the funding. APLD has been filling its campuses with large, high‑quality tenants. The company announced a new U.S.‑based, high-investment-grade hyperscaler at Delta Forge 1, a 430-MW “AI factory” campus. That agreement brought in another big, creditworthy customer and reinforced the view that hyperscalers see Applied Digital as a recurring partner rather than a test case.

Strategy at the corporate level is pointing in the same direction. The recent separation of its cloud business, which created ChronoScale as a standalone public company, carved out a more services‑heavy operation. That move left APLD more focused on being a pure data center and “AI factory” landlord.

Taken together, the Polaris Forge 3 lease is clearly designed to sit at the heart of a larger, infrastructure‑style earnings engine.

Street Expectations Still Leaning In

The company’s next earnings release is scheduled for July 29, and for the current quarter ending May 26, the average earnings estimate sits at a loss of $0.13 per share. That compares with a loss of $0.12 in the same quarter last year, implying a YOY “growth” rate on that metric of ‑8.33%.

That gap between ongoing losses and long‑term optimism shows up clearly in recent research commentary. H.C. Wainwright reiterated a “Buy” rating on Applied Digital after its fiscal Q3 results. The firm noted the profitability issues but also highlighted the strength of the company’s growth profile.

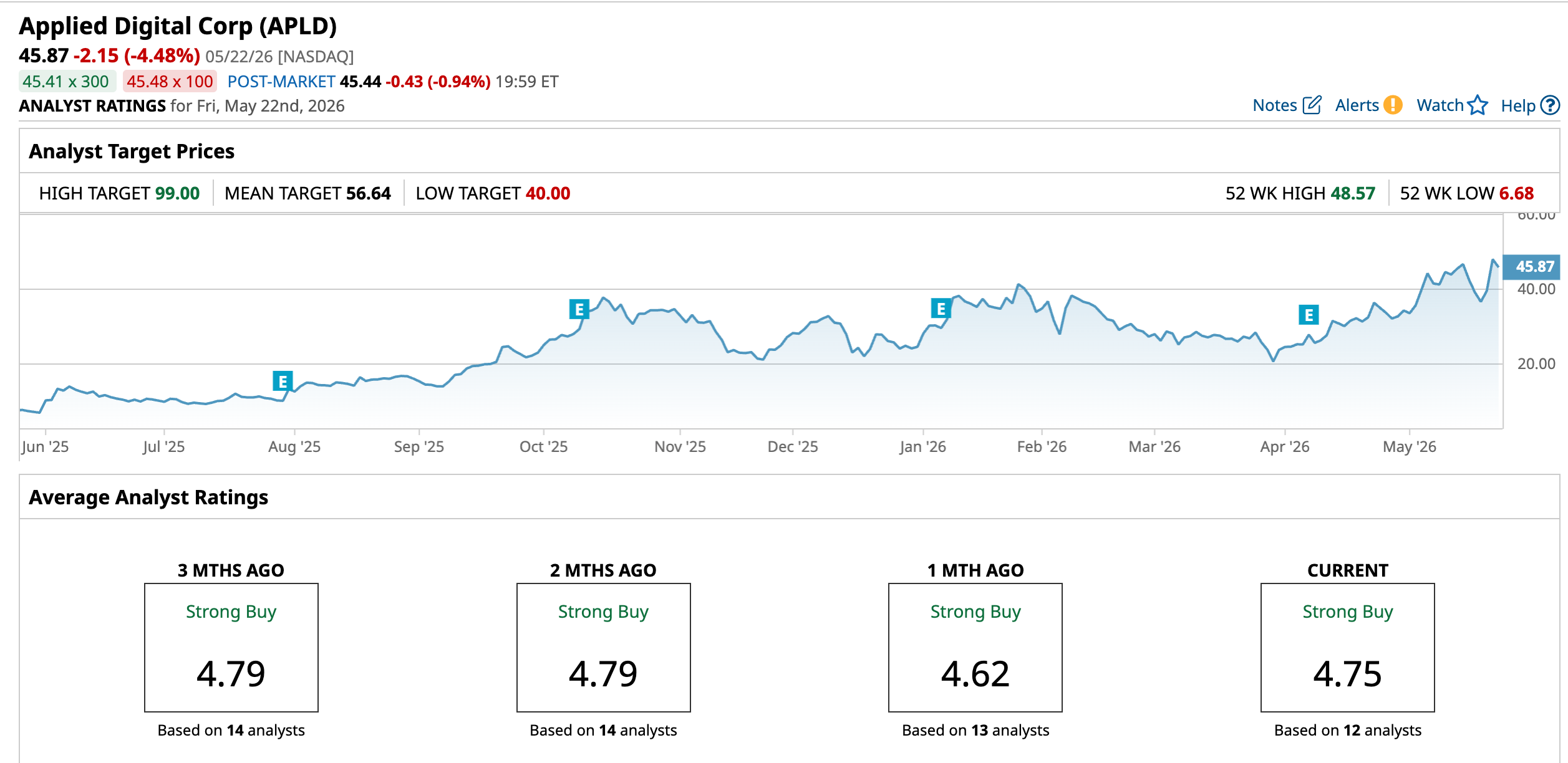

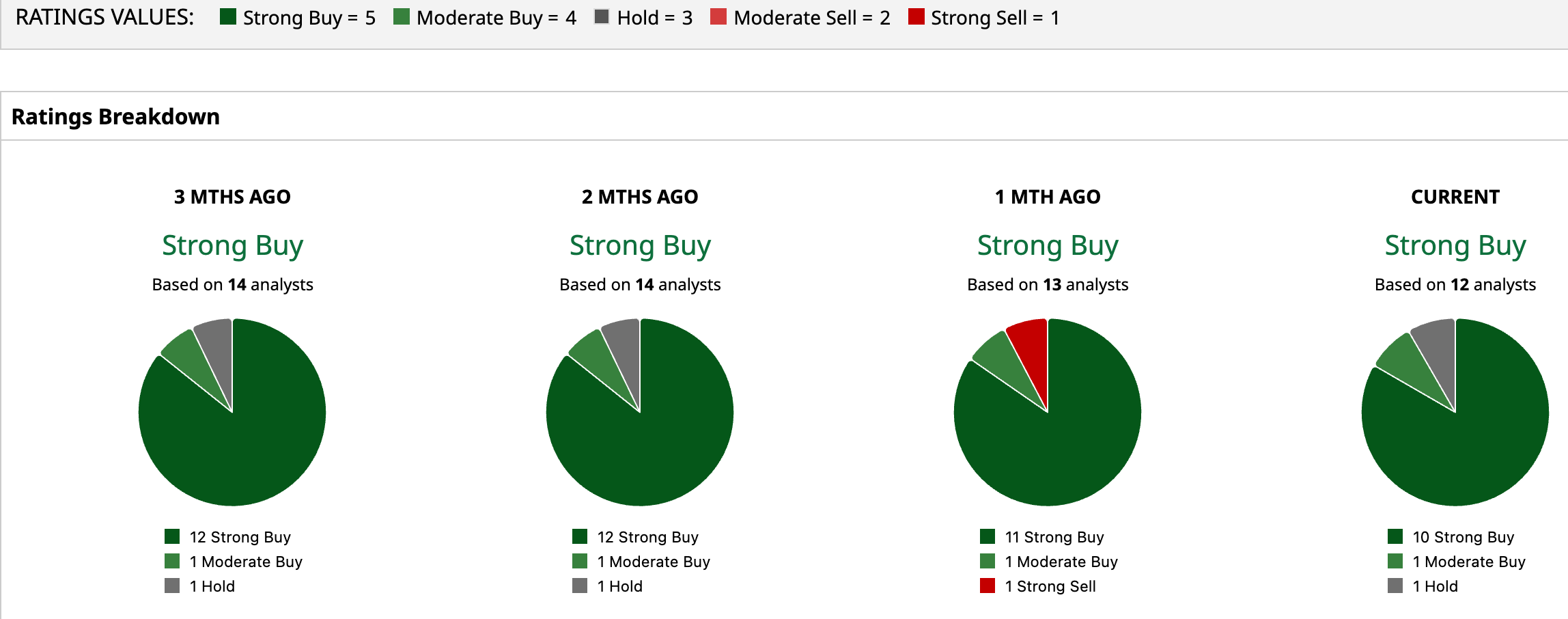

Analyst consensus tells a similar story. Out of 12 analysts surveyed, the stock holds a “Strong Buy” consensus rating. The average price target is $54.64, which works out to 19.12% upside.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

Applied Digital’s 15‑year Polaris Forge 3 lease moves the company closer to being seen as a long‑term infrastructure landlord with real staying power, not just a stock that pops on news. The most likely path from here is slower, bumpier upside rather than another explosive rally, with any pullbacks likely giving better entry points if execution and financing stay solid. Over a multi‑year stretch, the size of its contracted revenue and its ties to major hyperscalers still tilt the story toward higher levels rather than a full round trip back down.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Nvidia Had Another ‘Usual’ Quarter: How to Play NVDA Stock After Q1 Earnings Nvidia Hikes Its Dividend and Buybacks Based on Surging FCF - Is NVDA Too Cheap? Applied Digital Signed a Major Lease With a Hyperscaler for Its New Polaris Forge 3 Campus. What This Means for APLD Stock. Nvidia Just Raised Its Dividend by 2,400%. NVDA Stock Is Still a Bet on Growth, Not Income.